What are diabetes and glaucoma?

Diabetes is a chronic condition which occurs when your blood glucose, also known as blood sugar, levels are too high. There are 3 types of diabetes: type 1, type 2 and gestational diabetes with type 2 diabetes being the most common type of diabetes.1

Glaucoma is an eye condition that damages the optic nerve and may eventually lead to blindness.2 This condition typically develops gradually over time with the risk of glaucoma increasing with age.3

(See "Stay Safe This Dengue Season With These 3 Tips")

Treatment options for diabetes

While diabetes cannot be treated on your own, a combination of medication, exercise and diet can help to keep your diabetes in control. For type 2 diabetes, diet and exercise may even be enough for some to keep the disease under control.4

If you are feeling unwell or suspect yourself to have diabetes, please seek medical help from a professional.

(See "Is Your Term Insurance A Costly Mistake?")

Coverage options for diabetes

While most cases of diabetes can be controlled, severe cases of diabetes can lead to very high or low blood sugar levels and may require you to be hospitalised for treatment. Therefore, if you are worried about the cost of treatment in hospitals, having adequate hospital insurance would cover for inpatient and pre and post-hospitalisation treatment costs.

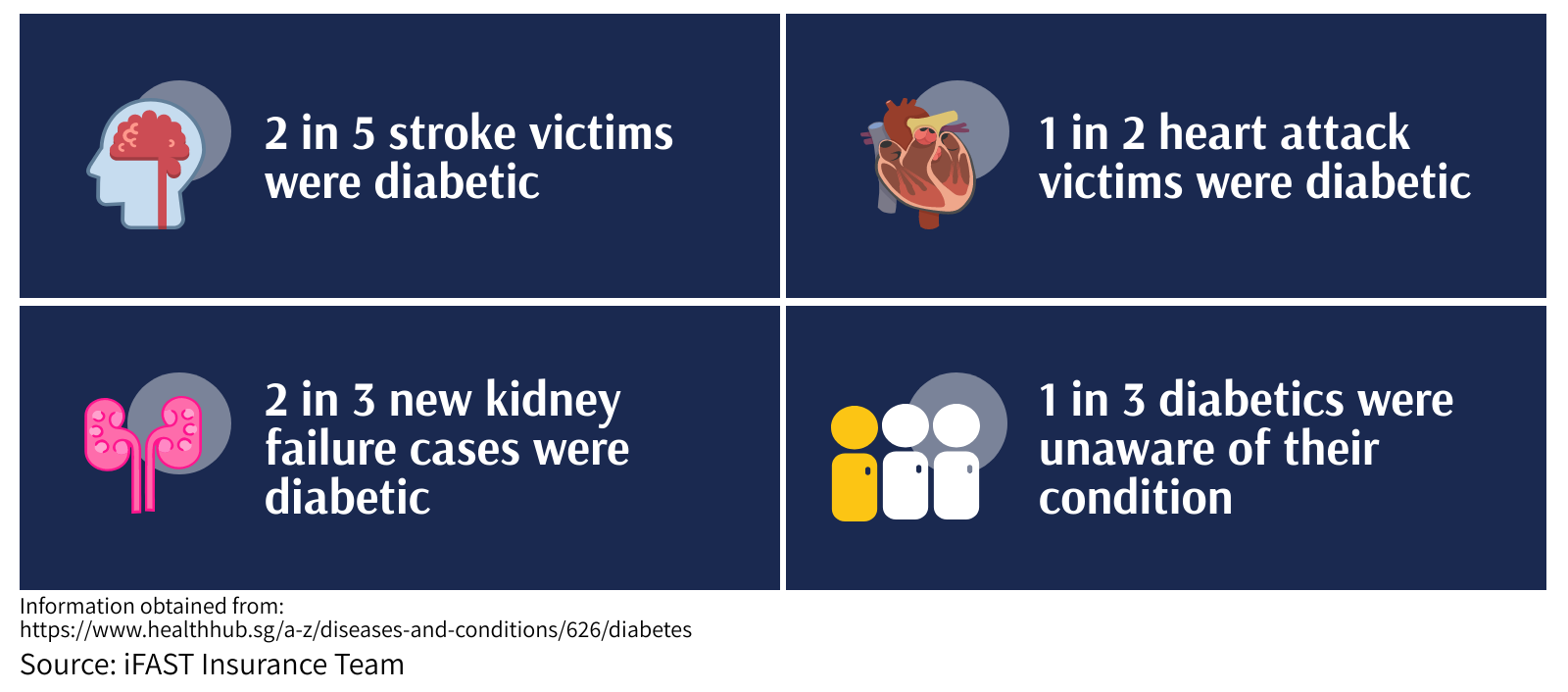

Additionally, severe diabetes could also result in long term complications such as stroke, cardiovascular diseases and damage to the eyes, kidneys and nerves.5

While critical illness (CI) insurance do not specify coverage for diabetes, CI plans may cover some of the complications that result from diabetes. Should these complications lead to any of the specified standard Life Insurance Association Singapore (LIA) definitions for critical illness, you would then be able to receive coverage from your critical illness insurance. Some possible complications include:

Heart attack of specified severity |

Open chest heart valve surgery |

Open chest surgery to aorta |

Angioplasty and other invasive treatment for coronary artery |

Stroke with permanent neurological deficit |

End stage kidney failure |

Alzheimer's disease or severe dementia |

Other serious coronary artery disease |

Deafness (irreversible loss of hearing) |

Blindness (irreversible loss of sight) |

Coma |

*This table only shows the relevant critical illnesses as defined by LIA. Early critical illness plans may have a more extensive list of coverage with coverage levels differing between insurers.

If you have pre-existing medical conditions but would still like to receive coverage, contact us for an in-depth review.

(See "3 Reasons To Not Get Basic Critical Illness Insurance")

Simple, high coverage, affordable. Protect yourself from the uncertainties of life

Treatment options for glaucoma

The most common type of glaucoma, primary open-angle glaucoma, is hereditary with family history increasing your risk of glaucoma by four to nine times.6 Having diabetes, high blood pressure and heart disease could also put you at a higher risk of glaucoma. There are four typical treatment options for Glaucoma: using prescription eye drops, oral medications, laser surgery or microsurgery.7

If you are feeling unwell or suspect yourself to have glaucoma, please seek medical help from a professional.

(See "When Is Whole Life Insurance The Better Option?")

How you can get coverage for glaucoma

Likewise, as Glaucoma is not one of the specified critical illnesses as defined by LIA, a critical illness (CI) insurance would not cover for glaucoma per se. However, glaucoma could lead to blindness with it being the leading cause of irreversible blindness in the world. Therefore, as vision loss due to glaucoma is irreversible, this will fulfill the LIA definition of blindness. Coverage from your critical illness insurance is payable in the event that glaucoma leads to the irreversible loss of sight.

With treatment options for glaucoma including laser surgery or microsurgery to lower the pressure in the eye, having integrated shield plan and riders for comprehensive hospital coverage will also be beneficial. This would allow you to receive coverage for any inpatient and pre and post-hospitalisation treatments that you may require.

Additionally, you may also consider long-term care insurance, also known as disability insurance, which pays upon the inability to perform the first Activity of Daily Living (ADLs).

(See "What Happens If I Don’t Have Long-term Care Insurance?")

Over 8,100 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Chubb, Etiqa Insurance, FWD Insurance, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Is Your MINDEF Group Insurance Really The Cheapest?

Cheap Car Insurance Singapore 2020

Critical Illness Insurance In A Nutshell

----

1Source: https://www.mayoclinic.org/diseases-conditions/glaucoma/

2Source: https://www.singhealth.com.sg/patient-care/patient-education/glaucoma

3Source: https://www.healthhub.sg/a-z/diseases-and-conditions/380/glaucoma)_nuh

4Source: https://www.webmd.com/diabetes/guide/understanding-diabetes-detection-treatment

6Source: https://www.glaucoma.org/