A recap on the basic insurance needs:

- Hospitalisation: Hospital insurance should be prioritised as the foundation of your insurance needs. Opt for a private hospital plan if you can afford it and downgrade if there is the need to do so in future. This is because it will be easier to get covered now when you are healthy, and to downgrade in future if there is the need to do so.

- Death and Total Permanent Disability (TPD): This mortality coverage is recommended when you are actively drawing a salary and have dependents that are financially reliant on you.

- The Monetary Authority of Singapore (MAS)’s Basic Financial Planning Guide recommends individuals to have 9 times their annual income for coverage.

- To estimate how much coverage you need, take into consideration the age of your dependents and how many more years will they be financially reliant on you.

- Remember to also factor in your financial situation including monthly expenses, assets, liabilities (e.g. mortgage, car loans, etc.), and if you have any existing insurance coverage.

- Critical illness (CI): Receive a lump sum pay-out upon diagnosis of a covered critical illness condition. CI coverage provide income replacement during your recovery period.

- According to MAS’s Basic Financial Planning Guide, individuals are recommended to have 4 times their annual income for CI coverage. An analysis of CI coverage can be found in our article: Our 2025 Review on Critical Illness (CI) coverage: Minimise your lifetime premium on your CI plan with this guide

- Long-term care: CareShield Life will provide monthly benefits when you are unable to perform 3 out of 6 activities of daily living (ADL). Consider CareShield Life supplements to receive higher monthly pay-outs if you are disabled and unable to perform 1 or 2 ADLs as specified in your policy. You may also use your MediSave to pay for your CareShield Life supplements up to $600 per calendar year per insured person.

If you are in your 40s and fall into the life stage of married with children, this is our insurance recommendation for you.

Similar to our previous article “How much should my insurance cost when I am 30?”, we create a sample portfolio for the profile below to better illustrate how much you may expect to pay for your insurance if you are 40 and at a different life stage.

Profile: Age 40 (date of birth 1 January 1985), non-smoker Singaporean male residing in Singapore.

Assumptions made:

In this article, we will only consider insurance needs for the parent. An assumption is also made to have your share of future household expenses, and unpaid services (eg. part time helper or caregiver costs) covered by the 9 times death and TPD coverage as stated in MAS’s Basic Financial Planning guide.

Reach out to us here if you would like a detailed calculation on your protection needs, or if you would like an in-depth review for coverage for your child.

Our suggested coverage:

Coverage Suggested (Present value) |

Coverage Suggested (Adjusted for inflation*) |

|

Death, and Total Permanent Disability (TPD) to cover your share of future household expenses, and other caregiver costs. |

Equivalent to 9 times annual income = $697,464 |

$1,068,860 |

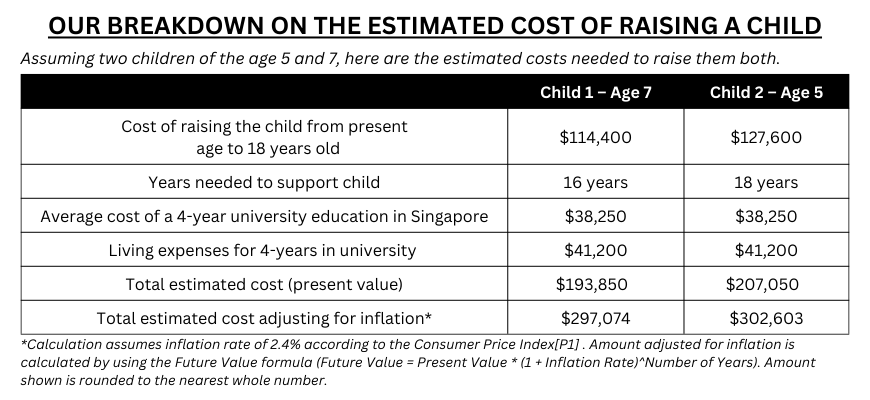

Death, and Total Permanent Disability (TPD) coverage you need to financially support your child. |

$400,900 |

$599,678 |

Total death, and Total Permanent Disability (TPD) |

$1,098,364 |

$1,668,538 |

Critical illness coverage |

Equivalent to 4 times annual income = $309,984 |

$475,049 |

Hospitalisation |

Start with a private hospital plan and add on a rider to lower the co-payment required if you can afford this. It will be easier to get covered now when you are healthy, and to downgrade in future should you need to do so. |

|

Long-Term Care |

To maximise the $600 per year MediSave additional withdrawal limit for higher monthly pay-outs, and to allow pay-outs to start when you are unable to perform 1 or 2 ADLs. This will enhance the coverage you have with CareShield Life where pay-outs commence with the inability to perform 3 out of 6 ADLs. |

|

*Calculation assumes inflation rate of 2.4% according to the Consumer Price Index . Amount adjusted for inflation is calculated by using the Future Value formula (Future Value = Present Value * (1 + Inflation Rate)^Number of Years). Amount shown is rounded to the nearest whole number.

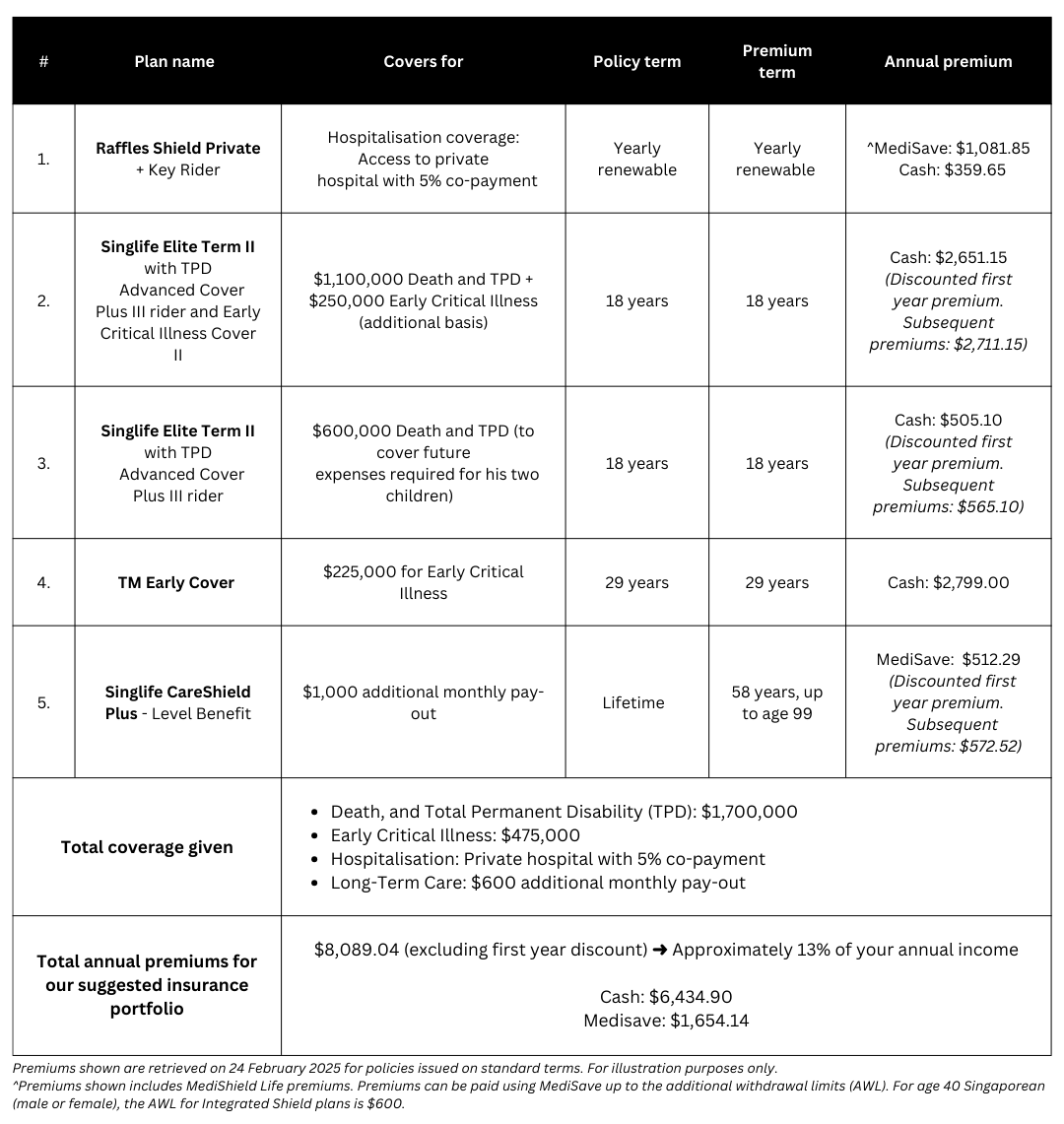

Premium illustration for our recommended coverage (For Male, Non-Smoker, age 40)

We created a recommended insurance portfolio based on the coverage required by the profile above. We recommend that this portfolio include death, TPD, and critical illness coverage for a minimum of 18 years, ensuring protection until his youngest child completes university. Hospital and long-term care coverage should be maintained for the insured's lifetime.

As shown in the table above, we used 3 different plans to cover the profile’s death, TPD, and critical illness needs. By doing so, we are able to lower the annual premiums payable and provide more flexibility for his coverage.

For example,

- Plan #2, a $1.1 million death and TPD coverage with an additional $250,000 early critical illness coverage from Singlife Elite Term II is intended to be used for the profile’s own mortality needs. This is separate from what the profile needs for his children thus allowing him the flexibility to review or cancel the plan if required.

- His plan #3 $600,000 death and TPD coverage from Singlife Elite Term II with TPD Advanced Cover Plus III rider can be used for his children’s future expenses. This separates out the coverage needed for his children from his own mortality coverage needs.

Our recommended insurance portfolio will cost the profile $8,089.04 a year. This is approximately 13% of his annual income (after CPF contributions are deducted) and is well within the 15% limit as set out by MAS’s basic financial planning guide.

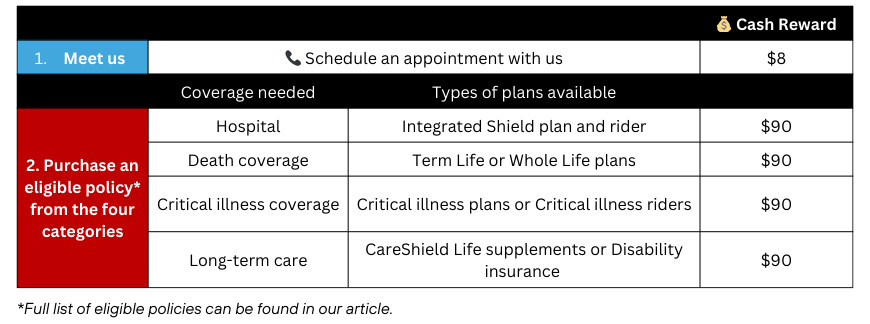

💰 Unlock up to $368 cash account credits* when you take the first step towards understanding your protection needs

Unsure of how much your insurance should cost? Let us assist with your protection needs! Reach out to us here to schedule an appointment and unlock up to $368 cash account credits*!

Here’s how you can unlock the $368 reward:

1. The first 10 persons to schedule and attend an appointment with our FSMOne Insurance Specialist will receive $8.

2. Check if you are adequately covered during the appointment, and get covered (if applicable) for any of the four protection categories to receive up to $360.

You may also receive up to 45% commission rebates on your policies when you choose FSMOne for your insurance needs!

👉 Read also: Our Rebate Program – Save more when you insure with us

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://www.careshieldlife.gov.sg/supplements.html

https://stats.mom.gov.sg/Pages/Labour-Force-In-Singapore-2024.aspx

https://www.msf.gov.sg/docs/default-source/research-data/family-trends-report-(final).pdf?sfvrsn=8d984171_2#:~:text=The%20resident%20Total%20Fertility%20Rate,in%202013%20(Chart%2011).&text=The%20median%20age%20of%20first,to%2031.6%20years%20in%202023.

https://dollarsandsense.sg/much-cost-raise-child-singapore-till-age-18/

https://smartwealth.sg/cost-of-university-fees-singapore/

https://www.singstat.gov.sg/-/media/files/news/cpidec24.ashx

https://www.cpf.gov.sg/service/article/what-are-additional-withdrawal-limits-awls-for-integrated-shield-plan-ip-premiums

https://www.mas.gov.sg/-/media/mas-media-library/news/media-releases/2023/basic-financial-planning-guide-2023.pdf

Information retrieved on 24 February 2025.

Disclaimer:

All materials and contents found in this advertisement are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This advertisement is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

All materials and contents found in this advertisement do not have any regard for the specific financial objectives, financial situation and particular needs of any specific person. You are advised to read the key product documents, including (but not limited to) the product summary, precise terms, conditions and exclusions specified in the relevant policy contract and consider carefully before deciding whether the product is suitable for you. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by Monetary Authority of Singapore.