What is home insurance?

Home content insurance protects the belongings inside your home against loss or damage. This includes but are not limited to your furniture, appliances, electronics, valuables, renovation and building and structure. This differs from the compulsory HDB fire insurance and MCST fire insurance policies that only covers for the building and not the individual owner’s home contents, renovations or improvements made.

1. Insured perils vs All Risk

There are two types of home content insurance. Namely, insured perils home insurance and all risk home insurance.

a. Coverage

- Insured perils – Insured perils home insurance only covers for specified events. Such events usually includes but are not limited to: Fire, lightning, explosion, impact by road vehicles, bursting or overflowing of water tanks or pipes, theft by violent or forcible entry, specified natural disasters such as floods, riots and strikes. Damages or loss that are not a result of these insured events will not be claimable from the home insurance policies.

- All risk – For all risk home insurance, all accidental loss or damages are generally covered unless explicitly excluded. This offers a wider scope of coverage as compared to insured perils home insurance.

An illustration of events covered under insured perils vs all risk home insurance

Scenario |

Insured perils home insurance |

All risk home insurance |

A water pipe bursts in your home and causes damages to the items in your home |

✔️Covered |

✔️Covered |

A water pipe bursts outside of your home and water from this burst pipe flows into your house and damages the items in your home |

❌Not covered |

✔️Covered |

The scenario above is for illustration purposes only. For specific coverage details, please refer to your policy wording.

b. Cost

While all risk home insurance offers broad coverage for your home content, buildings and renovation, such coverage usually cost more.

Illustrated premiums for all risk home insurance

Great Eastern GREAT Home Protect |

Sompo Home Max |

|

Home content |

Up to $50,000 |

Up to $50,000 |

Building cover |

Up to $100,000 |

Up to $100,000 |

Renovation cover |

Up to $50,000 |

|

Annual Premium (including GST) - before discounts |

$277.96 |

$204.38 |

Premiums are generated on 10 March 2025 and are for illustration purposes only. Although there may be some differences in the benefits across the plans, we have made every effort to align them as closely as possible for this comparison.

Insured perils vs All risk home insurance plans available on FSMOne:

Insured perils home insurance |

All risk home insurance |

2. Average clause vs First loss

Home content insurance can be further categorised into two types of plans:

- Average clause home insurance – For home insurance with an average clause, your claim amount will be prorated by the insurer should you under-insure the value of your home. Underinsurance occurs when your coverage does not match the full cost of rebuilding, renovating, or replacing your property and belongings. In this scenario, you will be unable to fully claim for your losses as the insurer will prorate the amount payable in the event of a loss or damage.

- First loss home insurance – Unlike average clause policies, you will not be penalised for underinsurance with a first loss home insurance policy. This is because a first loss policy ensures that claims are paid to the full sum insured as specified in your benefit table. No average clause or underinsurance penalties will be applied. Consider first loss home insurance policies to avoid receiving a pro-rated pay-out in the event of a claim.

An illustration for home insurance with an average clause vs first loss

Insurance coverage |

Value of your home content |

In the event of claim for a loss or damage of $50,000, the amount you will be able to claim are… |

|

For home insurance with an average clause |

For a first loss home insurance |

||

$50,000 |

$100,000 |

As your insurance coverage is less than the value of your home content, your house is underinsured by $50,000. Therefore, the insurer will pay a prorated amount of 50% of the loss or damage value ($50,000 / $100,000 = 50%). The insurer will pay $25,000 (50% of $50,000) for your claims for the above scenario. |

The insurer will pay up to the limits of your policy. For the above scenario, the insurer will pay $50,000 for your loss. |

$50,000 |

$50,000 |

As you are adequately insured, the insurer will pay $50,000 for the above scenario. |

The insurer will pay up to the limits of your policy. For the above scenario, the insurer will pay $50,000 for your loss. |

$100,000 |

$50,000 |

As you are adequately insured, the insurer will pay $50,000 for the above scenario. |

The insurer will pay up to the limits of your policy. For the above scenario, the insurer will pay $50,000 for your loss. |

The comparisons and opinions provided here are for illustration purposes only. Actual values and calculations may vary depending on specific conditions or factors.

First loss vs average clause home insurance plans available on FSMOne:

First loss home insurance |

Home insurance with an average clause |

💡 What we recommend:

Our recommendation |

Purchase here |

|

For affordable premiums |

We recommend: QBE Home Prestige

Note: An excess of $100 for each and every claim applies. This means that you will have to pay the first $100 and claim the remainder of every claim related to this home insurance. ⭐Suitable for: HDB Flats |

|

For optional building coverage |

We recommend: Allianz Home Protect or FWD Home Insurance

Allianz Home Protect FWD Home Insurance ⭐Suitable for: Condominium or Executive Condominium |

Allianz Home Protect:

FWD Home Insurance

|

For most comprehensive coverage |

We recommend: Great Eastern’s GREAT Home Protect

Note: Premiums tend to be higher due to the broad coverage offered. ⭐Suitable for: Landed properties where a higher building and renovation coverage is needed. |

Click: Home Insurance > GREAT Home Protect

|

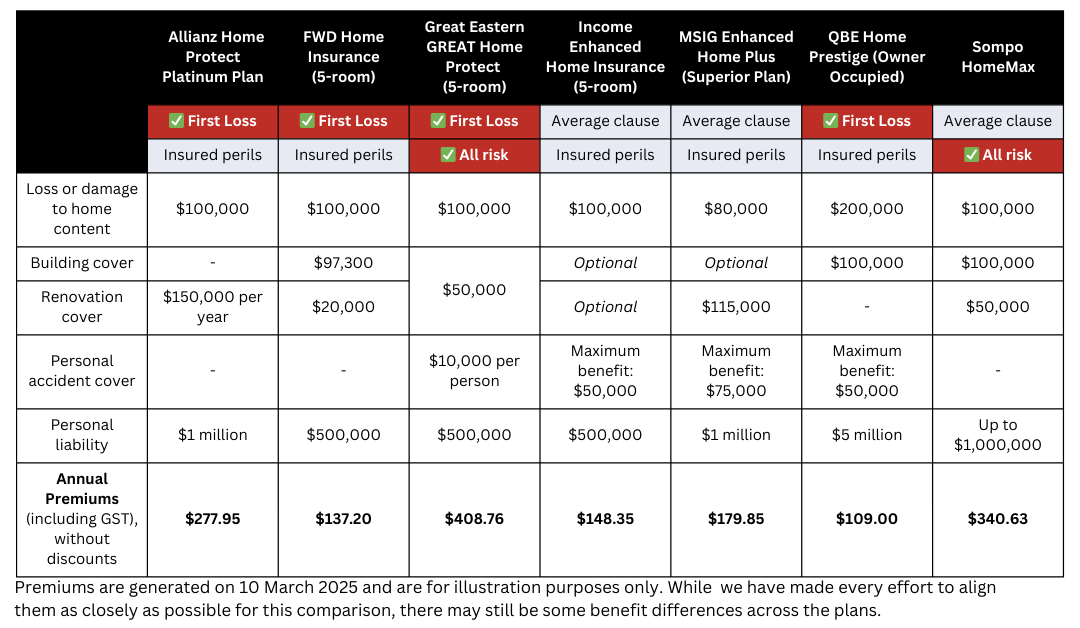

Illustrated premiums for home content insurance for a 5-room HDB flat

Compare and discover Home insurance plans available on FSMOne

Easily compare and view all available home insurance plans we have available. Simply click here to head to our Lifestyle insurance page and click on the “Home Insurance” tab.

✅ Get an overview of all available insurance options in one place (E.g. Travel, Car, Personal Accident, Home, Maid, Pet insurance)

✅ Explore the best offers with current promotions highlighted on the page.

✅ Fuss-free online purchase available

Or click here to contact us if you have any questions on your insurance plan.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://gia.org.sg/property-insurance-faq/397-all-home-insurance-coverage-is-the-same.html

https://azconnect.allianz.sg/channel/direct?pr=HOME_PROTECT_PRODUCT&er=~~0000056~91181076

https://www.fwd.com.sg/home-insurance/?utm_source=AFFINITY&utm_medium=NONAPI&utm_campaign=IFAST&promo=IFAST

https://www.greateasternlife.com/sg/en/personal-insurance/our-products/home-insurance/great-home-protect.html?

https://e-insure2.msig.sg/cp/product/broker/HOME/P34EnhancedHomePlusV1?producerRef=IFAAF

https://www.income.com.sg/buy/enhanced-home-insurance?prep=YWdlbnRDb2RlPTYzMDYwMCZ1bmRlZmluZWQ=

https://www.sompo.com.sg/products/home

https://sg-customer.qbe.com/home/partner/01001100

Information retrieved on 10 March 2025.

Disclaimer(s):

All materials and contents found in this advertisement are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This advertisement is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

All materials and contents found in this advertisement do not have any regard for the specific financial objectives, financial situation and particular needs of any specific person. You are advised to read the key product documents, including (but not limited to) the product summary, precise terms, conditions and exclusions specified in the relevant policy contract and consider carefully before deciding whether the product is suitable for you. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

The comparisons and opinions provided are based on publicly available data/information and are intended to provide a general overview of the insurance products discussed. These comparisons do not cover all available products and may not fully illustrate every aspect of the products discussed.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

This advertisement has not been reviewed by the Monetary Authority of Singapore.