' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

What is critical illness insurance?

Critical illness (CI) insurance offers financial protection if you are diagnosed with a critical illness. Such plans include coverage for the 37 standard critical illnesses as defined by the Life Insurance Association Singapore (LIA) and may also cover for up to 158 conditions (covering specified early or intermediate stages critical illnesses). Upon diagnosis of a covered condition, a lump sum payout is provided to the insured to cushion the financial impact.

Critical illness coverage can be obtained from standalone CI plans, or by attaching early critical illness (ECI) riders to your term or whole life plans. In this article, we share the different options for critical illness coverage and our recommendation on what we feel is the optimal approach to getting critical illness coverage.

1. Standalone Critical Illness (CI) plans

There are two types of coverage offered from standalone critical illness plans:

- Critical illness plan that provides a single pay-out offers a one-time pay-out for specified critical illnesses. For most plans, this means a 100% pay-out of the sum assured for early, intermediate, and advanced stage critical illness up to the specified policy limits. These plans only cover for a single critical illness, and coverage will cease once the sum assured reduces to zero.

- Critical illness plan with multiple pay-outs provides multiple pay-outs for different critical illnesses, ensuring that you remain covered even after the first critical illness strikes. These plans provide continued coverage after the first claim, allowing for subsequent claims for different specified critical illness. Depending on the insurer’s terms, you may potentially receive a total pay out of up to 10 times your sum assured.

Critical illness plan that provides a single pay-out |

Critical illness plan with multiple pay-outs |

|

Pros |

||

Cons |

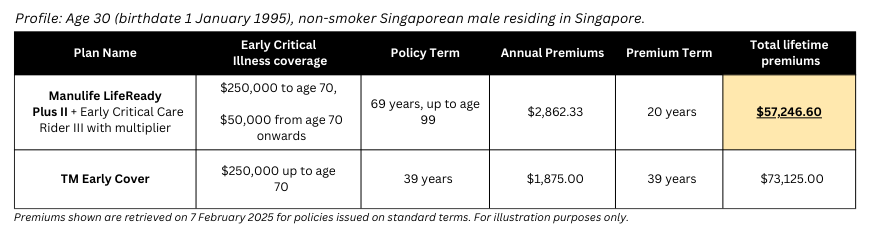

Premium illustration for standalone critical illness plans

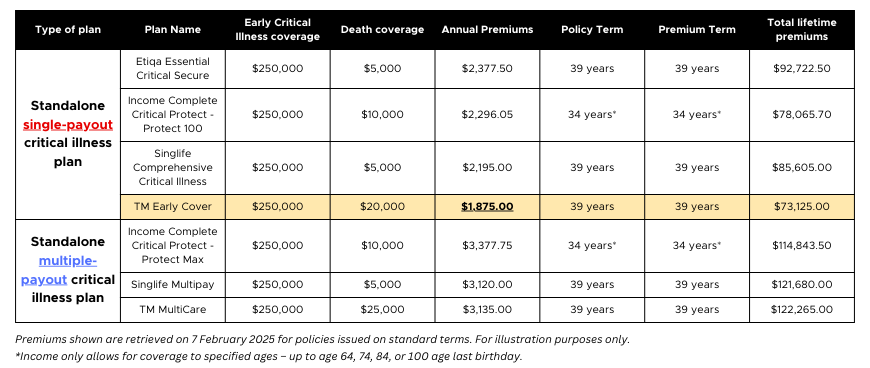

Profile: Age 30 (birthdate 1 January 1995), non-smoker Singaporean male residing in Singapore

⭐ For low upfront premiums: TM Early Cover (standalone single pay-out critical illness plan)

As shown in the table above, premiums for a standalone single payout critical illness plan are generally lower with TM Early Cover offering the most competitive initial premium at $1,875 a year. This is approximately 40 per cent cheaper than the multiple pay-out critical illness plans.

2. Critical illness riders

Critical illness riders are optional benefits that can be added to term life or whole life plans to provide coverage for critical illnesses. Such riders offer comparable coverage to standalone single pay-out critical illness plans but has the added advantage of being a dual-purpose plan by providing both death or Total Permanent Disability (TPD) coverage and critical illness protection. Additionally, the total lifetime premiums paid for critical illness riders may also be lower than those paid for standalone critical illness plans.

There are two types of critical illness (CI) riders: accelerated and additional.

Early Critical Illness riders given on an accelerated basis |

Early Critical Illness riders given on an additional basis |

💡Tip: Critical illness riders that pay on an additional basis offers more coverage. However, such plans may end up being more expensive.

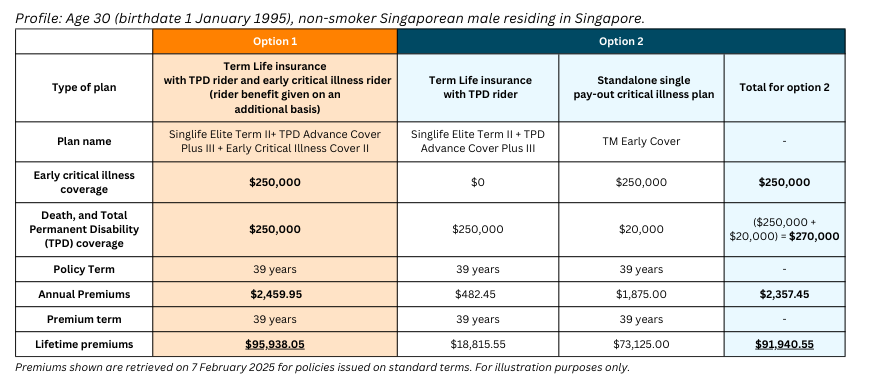

As shown in the table below, term life insurance with an early critical illness (ECI) rider given on an additional basis will provide $250,000 ECI coverage, and $250,000 death and TPD coverage. Annual premiums for this option work out to $2,459.95 a year, with the total lifetime premiums payable amounting to $95,938.05.

However, if we were to use two separate plans for coverage instead – (1) a term life plan and (2) a standalone single pay-out critical illness plan, the individual would receive a total of $250,000 ECI coverage, and $270,000 death and TPD coverage. Not only will the individual have a higher death coverage, but the annual premiums will also be lower at $2,357.45 a year, or a total lifetime premium of $91,940.55.

Premium illustration for term or whole life plan with early critical illness riders

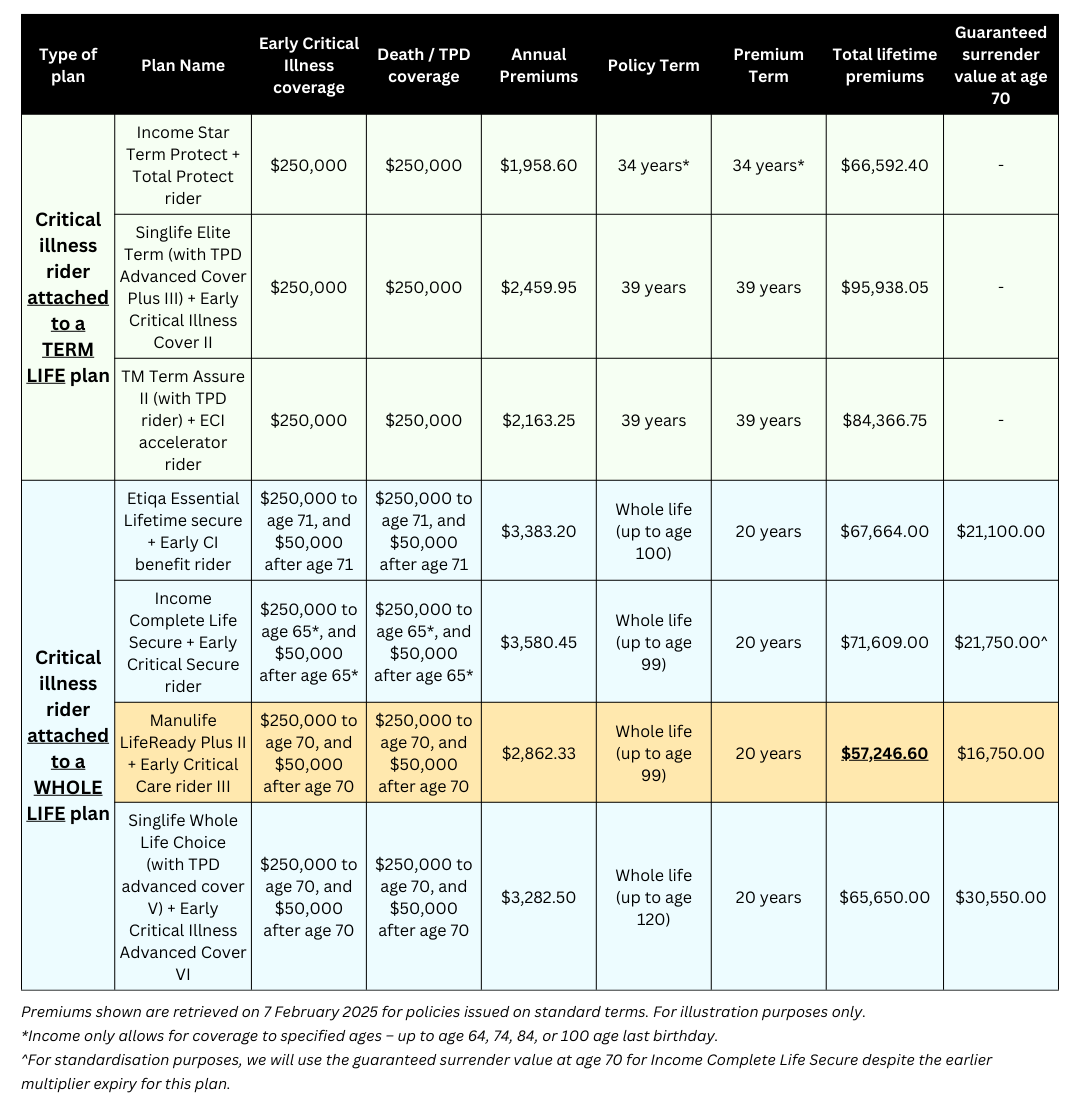

Profile: Age 30 (birthdate 1 January 1995), non-smoker Singaporean male residing in Singapore

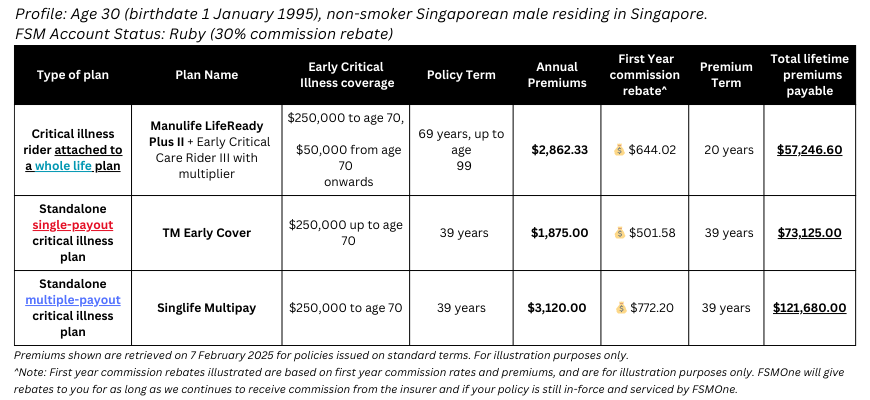

⭐ For low total lifetime premiums: Manulife LifeReady Plus II + Early Critical Care Rider III with multiplier (Critical illness rider attached to a whole life plan)

While whole life plans with an attached early critical illness (ECI) rider have higher initial premium, the total lifetime premium for such plans are lower than that of a term life plan with ECI rider. This can be seen in the table below where Manulife LifeReady Plus II with ECI has a total lifetime premium of $57,246.60, as compared to $73,125.00 for TM Early Cover (a standalone single pay-out critical illness plan). This represents a difference of $15,878.40 in total lifetime premium, or approximately 22 per cent in savings by opting for Manulife LifeReady Plus II with ECI rider instead of TM Early Cover.

If you prefer to pay less total lifetime premiums and are comfortable with paying a slightly higher initial premium, then this option of adding an ECI rider to a whole life plan may be suitable for you.

⭐ Alternatively, if you only intend to have coverage until age 70: Singlife Whole Life Choice + TPD Advance Cover V + Early Critical Illness Advance Cover VI with multiplier (Critical illness rider attached to a whole life plan)

If you only require critical illness coverage up to age 70, and intend to surrender your policy after, you may consider the Singlife Whole Life Choice option. While the initial premiums and total lifetime premiums are higher than Manulife LifeReady Plus II and TM Early Cover, Singlife Whole Life Choice has a higher guaranteed surrender value at age 70. This allows you to get back $30,550 if you no longer need coverage and surrender your plan then.

This guaranteed surrender value effectively reduces the actual cost of your insurance with Singlife Whole Life choice amounting to $35,100 if we take into consideration the guaranteed surrender value at age 70. This is significantly lower than the single pay-out CI plan (TM Early cover) with a total premium of $73,125, or the other whole life with ECI rider option (Manulife Life Ready)’s actual cost of insurance of $40,496.60.

.png)

This means that Singlife Whole Life Choice may be a better option if you are comfortable with the higher initial premiums needed and intend to surrender the plan and cease coverage at age 70.

💡 Tip: Consider surrendering your whole life plan with ECI rider once your plan’s multiplier expires (and coverage reduces) if you no longer require the coverage. This allows you to receive a lump sum surrender value that you can use for your hospital insurance plans (i.e. integrated shield premiums).

Other considerations:

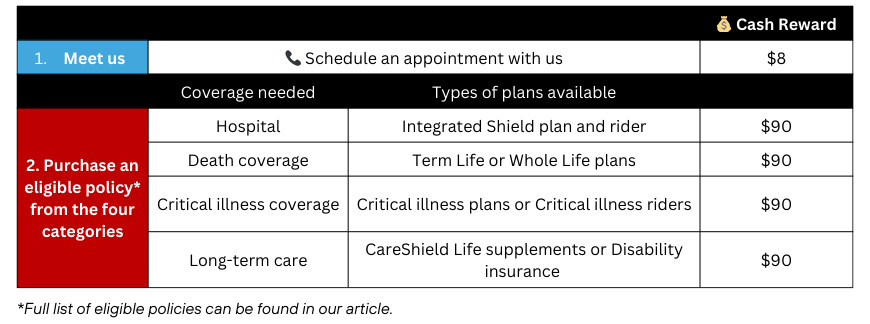

Get Rewarded with up to $368 Cash Account credits* when you trust FSMOne with your insurance

Have a question on your insurance but don’t know who to ask? Reach out to us here to schedule an appointment (be among the first 10 to schedule and attend an appointment to receive $8 cash account credits*) and let us assist with your protection needs!

Here’s how you can unlock the $368 reward:

- Be among the first 10 to schedule and attend an appointment with our FSMOne Insurance Specialist ($8)

- Check if you are adequately covered during the appointment, and get covered (if applicable) for any of the four protection categories (4 x $90)

You may also receive up to 45% commission rebates on your policies when you choose FSMOne for your insurance needs!

Read also: Our Rebate Program – Save more when you insure with us

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://www.lia.org.sg/media/4253/for-lia-mu-5824-part-2-of-4-_lia-ci-framework-2024_definitions-for-37-cis.pdf

Information retrieved on 12 February 2025.

Disclaimer(s):

All materials and contents found in this advertisement are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This advertisement is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

All materials and contents found in this advertisement do not have any regard for the specific financial objectives, financial situation and particular needs of any specific person. You are advised to read the key product documents, including (but not limited to) the product summary, precise terms, conditions and exclusions specified in the relevant policy contract and consider carefully before deciding whether the product is suitable for you. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")