' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Unsure about the differences in coverage between the various maid insurance plans? Find your ideal maid insurance plan on FSMOne. Compare options, understand MOM's requirements, and ensure you and your helper are protected against unexpected medical expenses, accidents, and other unforeseen events.

Ministry of Manpower’s (MOM) requirements on hiring foreign domestic help in Singapore

Are you hiring a foreign domestic helper for the first time? Here are three mandatory requirements to know when hiring a domestic helper in Singapore:

A security bond is not required for Malaysian helpers.

[🔎 MOM will enhance the medical insurance coverage for your helper in a stage 2 phase from 1 July 2025. This enhancement will include a direct reimbursement of medical bills from insurer to hospitals. More details for this can be found here.]

Choosing the right maid insurance plan is important. While many maid insurance plans offer similar coverage, we highlight three key factors for you to consider before making your purchase.

1. Is co-payment needed for hospitalisation and surgical expenses?

MOM has increased the required medical insurance coverage for domestic helpers with effect from 1 July 2023. This new annual claim limit is $60,000 and offers the employers a greater protection against large medical bills. However, while the annual claim limit is now higher, do note that most of the plans may include a 25% co-payment on claims exceeding $15,000.

An example of co-payment needed for hospitalisation and surgical expenses based on different bill amounts:

Hospitalisation bill |

Co-payment needed from the employer |

Amount claimable from insurer |

|

Scenario 1 |

$10,000 |

Not applicable for first $15,000 |

$10,000 |

Scenario 2 (without waiver of co-payment) |

$20,000 |

Co-payment applicable for claim amount above $15,000 ($20,000 - $15,000 = $5,000) $5,000 x 25% = $1,250 |

$15,000 + ($5,000 x 75%) = $18,750 |

Scenario 3 (with waiver of co-payment) |

$20,000 |

Not applicable up to the benefit limit of plan |

$20,000 |

This table is for illustration purposes only. Claim conditions may differ between insurer and plans.

Choose a comprehensive plan or opt for an optional add-on rider should you wish to reduce or remove your co-payment payable.

Plan(s) with no co-payment required for hospitalisation and surgical expenses |

Waiver of co-payment available as an optional add-on rider |

2. Outpatient medical expenses

Coverage for outpatient medical expenses can be split into two categories:

a. Outpatient medical expenses due to an accident or injury – This benefit will only be claimable in the event that your helper requires outpatient medical treatment as a result of an accident.

FWD Maid Insurance |

MSIG Maid Plus |

Income Domestic Helper |

|

Outpatient medical expenses due to an accident / injury |

Essential: Up to $1,000

Enhanced: Up to $2,000 Exclusive: Up to $3,000 |

Standard: Up to $1,000

Classic: Up to $2,000 Premier: Up to $3,000 |

Basic: Up to $1,500

Standard: Up to $2,000 Enhanced: Up to $3,000 |

Points to note |

Includes coverage for dengue fever or Zika.

Excludes coverage for TCM treatments. |

Sub-limit applies for dental, TCM, and dengue fever |

Includes TCM or chiropractor expenses within 12 months from date of accident. This benefit is capped at $100 per accident. |

This table is for illustration purposes only. Claim conditions may differ between insurer and plans.

b. Outpatient medical expenses due to an illness – While most insurance plans only cover for outpatient medical expenses due to an accident or injury, FWD’s Enhanced or Exclusive plan includes coverage for consultation, prescription, and diagnostic test costs if your helper needs to be treated for an illness. However, do note that treatment must be sought at a FWD’s network of clinics, and a co-payment of $10 will be required.

FWD Maid Insurance |

MSIG Maid Plus |

Income Domestic Helper |

|

Outpatient medical expenses due to an illness |

$30 per outpatient visit, up to $500 or $1,000 (subject to your chosen plan). Co-payment of $10 is required per visit. |

Not applicable |

Not applicable |

Points to note |

This benefit is available for Enhanced and Exclusive plans only. Treatment must be sought at FWD’s network of clinics. |

- |

- |

3. Waiver of counter indemnity for insurance guarantee bond to MOM

A waiver of counter indemnity may be available in specific plans or available as an optional add-on for maid insurance policies. This waiver protects employers from losing the $5,000 security bond required in the event that MOM calls on the security bond.

Note that the waiver of counter indemnity may not waive the entire $5,000 payable. In most instances, you will still need to pay the first $250 excess with the remaining $4,750 covered by your insurance plan (if applicable).

Plan(s) with waiver of MOM’s security bond included |

Waiver of MOM’s security bond available as an optional add-on rider |

Other commonly asked questions:

Q: How do I choose the start date for the period of insurance for my maid insurance policy?

A: The start date of your policy is dependent on the type of maid you are hiring:

Q: Why are maid insurance plans offered for 14 or 26 months when MOM only issues work permits for 12 or 24 months?

A: This is a requirement by MOM as the two extra months of insurance provides coverage for your maid in Singapore during the repatriation period following the expiration of their work permit.

Q: How will the security bond be transmitted to MOM?

A: The insurer will transmit the Security Bond details to MOM. Upon successful transmission, you may proceed to MOM’s website to renew or issue your maid’s work permit.

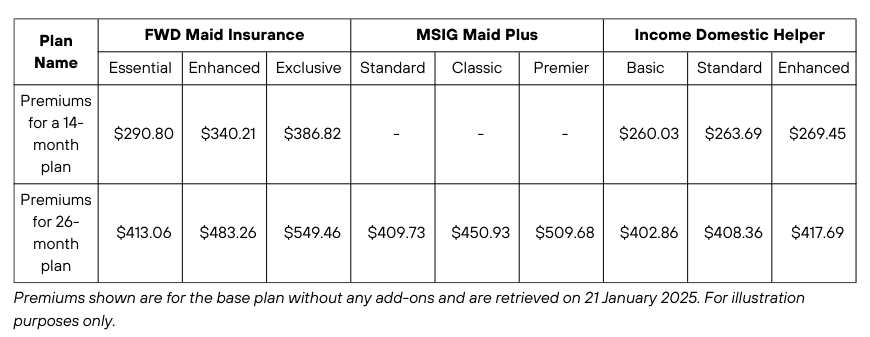

Q: How much will it cost to purchase maid insurance?

A: Here is how much you may expect to pay for your maid insurance plan:

Profile: Age 30 (Date of birth: 01/01/1995) for an Indonesian foreign domestic helper.

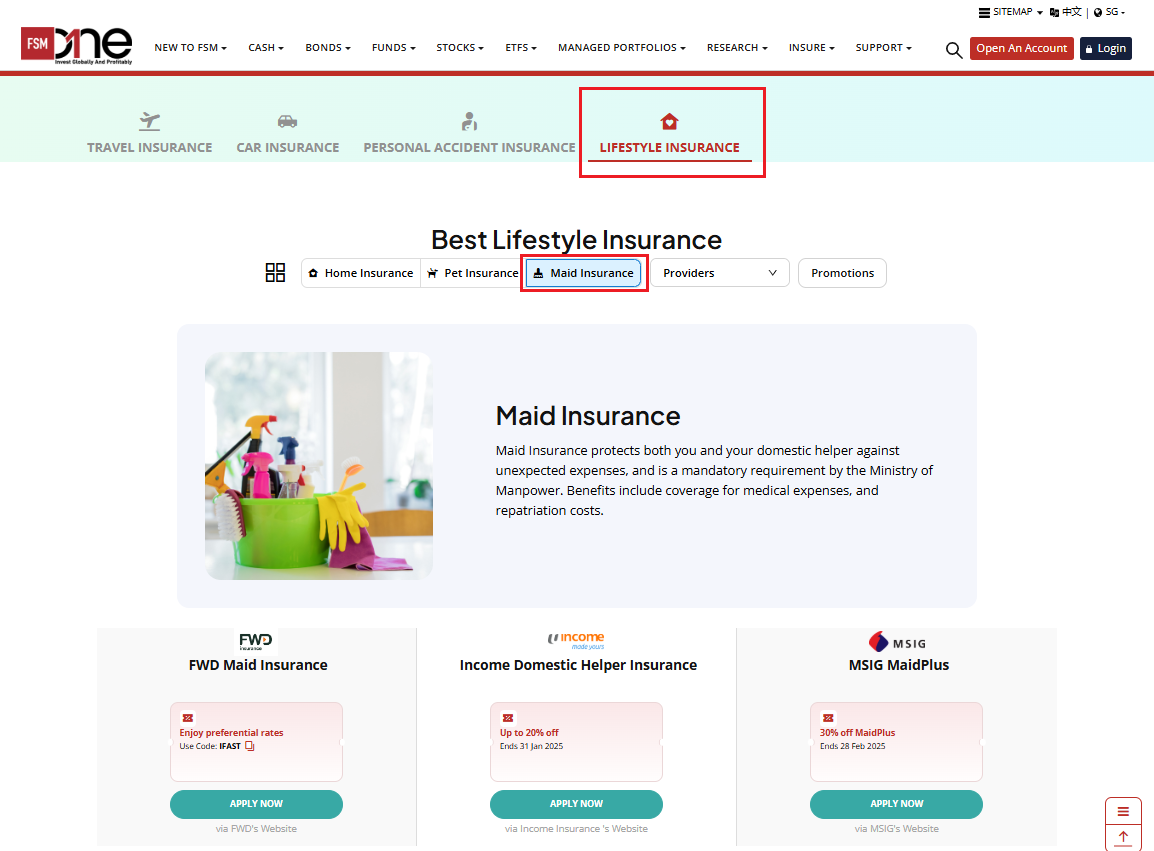

Compare and discover maid insurance deals on FSMOne

Get a snapshot of all maid insurance plans available on FSMOne with our newly launched comparison page, and find a plan that can best suit your budget and needs.

Click here to head to our Lifestyle insurance page and click on the “Maid Insurance” tab to compare across all maid insurance plans available on FSMOne.

✔ Snapshot of available insurance at a single glance (E.g. Travel, Car, Personal Accident, Home, Maid, Pet insurance)

✔ Find current promotions, and discover the best deal for you

✔ Direct online purchase

Or click here to contact us if you have any questions on your insurance plans.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://www.mom.gov.sg/passes-and-permits/work-permit-for-foreign-domestic-worker/eligibility-and-requirements/security-bond

https://www.mom.gov.sg/passes-and-permits/work-permit-for-foreign-domestic-worker/eligibility-and-requirements/insurance-requirements

https://www.mom.gov.sg/-/media/mom/documents/work-passes-and-permits/enhanced-mi-for-helper-infographic.pdf

https://www.fwd.com.sg/maid-insurance/

https://www.msig.com.sg/personal-insurance/maidplus

https://www.income.com.sg/domestic-helper-insurance

Information retrieved on 21 January 2025.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")