' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

A quick refresher on what makes up your hospitalisation coverage in Singapore

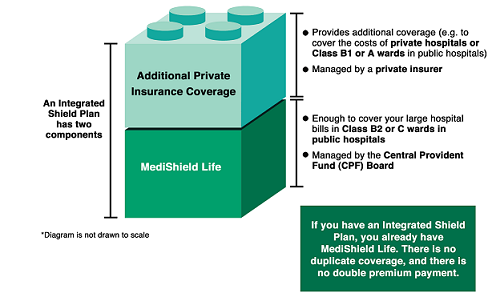

All Singaporeans and Permanent Residents (PRs) in Singapore are eligible for MediShield Life. This is a basic health insurance plan that is administered by the Central Provident Fund (CPF) Board and offers coverage for Class B2 or C wards in public hospitals.

Individuals may opt for Integrated Shield (IP) plans by private insurers if they wish to seek treatment at Class A or B1 wards in public hospitals, or private hospitals. IP riders can also be added on to cover for deductibles, and further enhance coverage.

(Source: https://www.moh.gov.sg/healthcare-schemes-subsidies/medishield-life)

Many people may by default opt for the highest-tier integrated shield (IP) plan for private hospital coverage. But is this necessary? Here are factors to consider when choosing a hospital plan.

1. Can you afford your IP premiums?

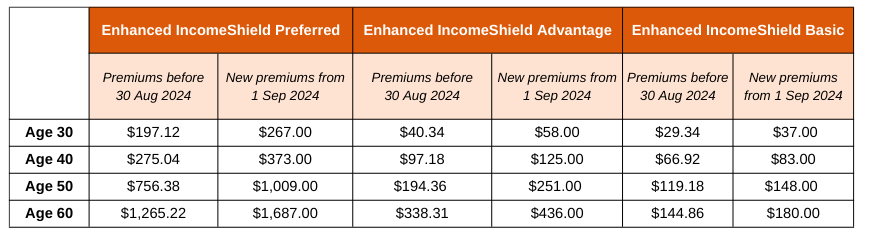

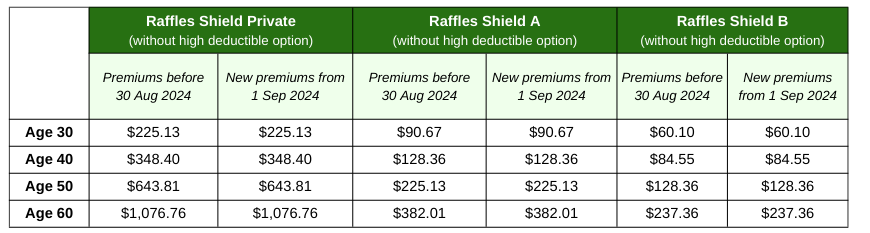

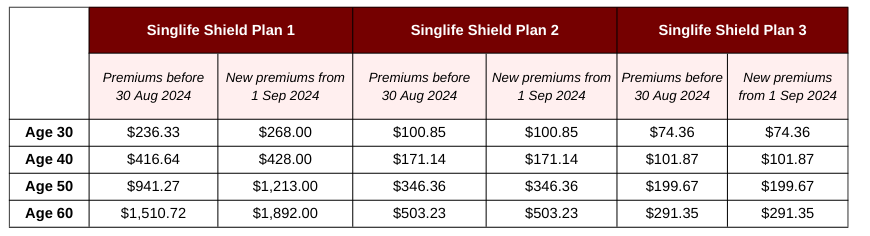

From 1 September 2024, integrated shield (IP) plan premiums have increased.

Major insurers like AIA, Income Insurance, Singlife, Great Eastern, and Prudential have stated that they will be raising the premiums for their integrated shield plans after 31 August 2024. This means that you are likely to experience higher premiums upon your next policy renewal.

For ease of comparison, we’ve compiled the difference in the total premiums (includes portion payable by Medisave) for the following insurers:

Premiums shown are retrieved on 3 October 2024 for policies issued on standard terms, and are for illustration purposes only.

With this recent increase in premiums and potential future premium hikes, ask yourself if your integrated shield plan is still affordable now, and can you continue affording it in future?

2. Which ward class will you seek medical treatment at?

Do you go straight to private hospitals when you need medical treatment? Or do you first visit a polyclinic to get a referral for treatment at public hospitals? While getting the highest tiered integrated shield plan will allow you to seek treatment at private hospitals, what if this is not what you need? If you tend to choose public hospitals for your medical treatments, then you may not actually need an IP plan with private hospital coverage.

According to the Ministry of Health, about half of patients with IP and rider protection end up using subsidised public healthcare for hospitalisation or day surgery. If this group of individuals had been paying for private hospital IP plans, they may have then been paying for coverage that they do not need. If you are guilty of also doing so, then it is time to reconsider your IP coverage.

Ward entitlement for the various IP plans:

Income |

Raffles |

Singlife |

|

Private hospital |

Enhanced IncomeShield Preferred |

Raffles Shield Private |

Singlife Shield Plan 1 |

Class A wards in public hospitals |

Enhanced IncomeShield Advantage |

Raffles Shield A |

Singlife Shield Plan 2 |

Class B1 wards in public hospitals |

Enhanced IncomeShield Basic |

Raffles Shield B |

Singlife Shield Plan 3 |

Alternatively, if you feel that your premiums are getting unaffordable, reassess your budget and determine if the additional cost is worth the benefits provided.

If you want private care, shorter waiting times for appointments and procedures, or have a specific doctor that you visit for treatments:

Get an IP plan with private hospital coverage. This ensures that you are adequately insured for your hospitalisation needs, and prevent you from having to pay high out-of-pocket expenses in the event of hospitalisation.

For treatment at private hospitals, here are the integrated shield plans we have available on FSMOne:

Private hospital integrated shield plans available on FSMOne

Enhanced IncomeShield Preferred |

Raffles Shield Private |

Singlife Shield Plan 1 |

|

Ward entitlement |

Private hospital |

||

Annual policy limit |

$1,500,000 |

$1,500,000 for in-panel, and $600,000 for non-panel |

$2,000,000 for A&E or preferred medical providers, and $1,000,000 for others |

Annual premiums (from 1 September 2024) |

|||

Age 30 |

$267.00 |

$225.13 |

$268.00 |

Age 40 |

$373.00 |

$348.40 |

$428.00 |

Age 50 |

$1,009.00 |

$643.81 |

$1,213.00 |

Age 60 |

$1,687.00 |

$1,076.76 |

$1,892.00 |

Premiums shown are retrieved on 3 October 2024 for policies issued on standard terms, and are for illustration purposes only.

Reconsider your choice of getting the “highest” ward class coverage if…

your approach is to go for subsidised care at public hospitals. Downgrading to the next tier of coverage (i.e. plans with Class A ward or Class B1 wards in public hospitals) may adequately address your needs at a more affordable cost for you.

Class A ward integrated shield plans available on FSMOne

Enhanced IncomeShield Advantage |

Raffles Shield A |

Singlife Shield Plan 2 |

|

Ward entitlement |

Class A wards in public hospitals |

||

Annual policy limit |

$500,000 |

$600,000 |

$1,000,000 |

Annual premiums (from 1 September 2024) |

|||

Age 30 |

$58.00 |

$90.67 |

$100.85 |

Age 40 |

$125.00 |

$128.36 |

$171.14 |

Age 50 |

$251.00 |

$225.13 |

$346.36 |

Age 60 |

$436.00 |

$382.01 |

$503.23 |

Premiums shown are retrieved on 3 October 2024 for policies issued on standard terms, and are for illustration purposes only.

Have a question? Click the button below if you would like a complimentary review from our team

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

You may also be interested in...

PSA: Is the insurance policy your parents bought for you serving you well?

1 in 5 Singaporeans lack life insurance coverage. Are you the 1 in 5?

Insurance is your subscription plan against life's uncertainties

Information obtained from:

https://www.moh.gov.sg/healthcare-schemes-subsidies/medishield-life

https://www.businesstimes.com.sg/wealth/five-seven-insurers-jack-private-hospital-premiums-under-integrated-shield-plans-some-double-digits

https://www.income.com.sg/kcassets/2a30f5fc-c64d-4c30-8818-ca0ffaf93e98/Premium%20Table%20for%20Enhanced%20IncomeShield%20and%20IncomeShield%20Standard%20Plan.pdf

https://www.income.com.sg/kcassets/57771d4e-8109-4258-b37c-106664279ad6/Premium%20Table%20EIS.pdf

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-health-plus/Singlife-Shield-HealthPlus-PremiumRates.pdf

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-health-plus/premium-rates.pdf

https://www.raffleshealthinsurance.com/wp-content/uploads/2021/03/Raffles-Shield-Product-Summary-1-April-2024-Finalv1-1.pdf

https://www.moh.gov.sg/news-highlights/details/medishield-life-adequacy-and-ip-consumer-education#:~:text=To%20illustrate%2C%20about%20half%20of,the%20major%20review%20this%20year

Information retrieved on 3 October 2024.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")