' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Unsure of what insurance coverage you have? Or are your parents still handling your insurance for you? If you are still relying on the insurance your parents bought for you 20 years ago, chances are that the coverage you have may no longer be applicable for your present-day needs.

1. Your critical illness insurance may be outdated

Did you know that in the past, critical illness (CI) plans used to only cover for up to a maximum of 30 CIs? This is applicable if you had purchased a critical illness insurance plan before the Life Insurance Association Singapore (LIA) Critical Illness framework was released in 2014. If you had bought your CI plan before 2003, your critical illness coverage may not even constitute of any of the current standard CI definitions as this CI definition standardisation was only first introduced by the LIA in 2003.

These changes in industry terms and coverage types are examples of how LIA periodically revises the CI definition to address ambiguities and the medical advancement or health trends. Just like how LIA makes revisions to the definitions, you should also review your insurance policies and coverage to ensure that it is still applicable for present day needs. If you are still holding on to an older insurance policy, you may wish to relook your policy terms and coverage conditions.

Reach out to us here if you are unsure of whether your coverage is adequate or if you would like a complimentary policy review. FSMOne clients will enjoy up to 45% commission rebates on their insurance purchased through us.

2. Is there a better option to get insured?

The insurance plan you purchased 10 years ago may no longer be the best option for you today.

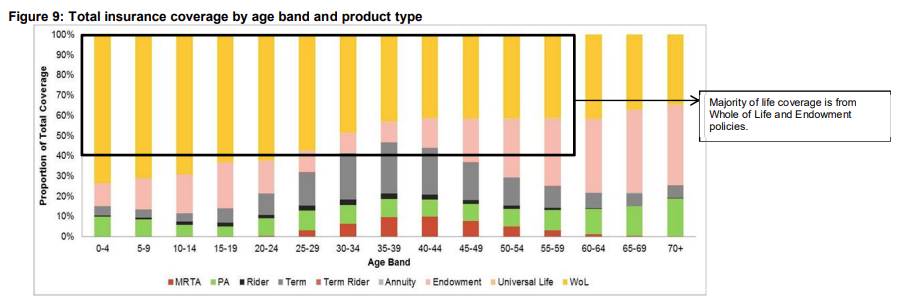

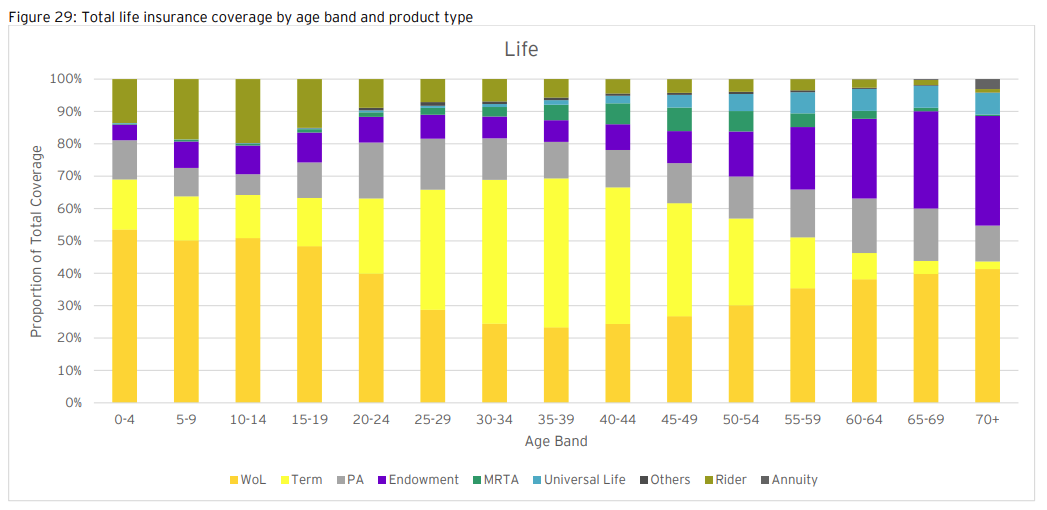

In the past, whole life and endowment plans dominated the market, making up 65% of all coverage purchased. This however is not ideal as purchasing whole life or endowments for protection needs can be expensive. Additionally, coverage amounts back then were generally lower, with whole life averaging $50,000 to $140,000 and term life averaging $25,000 to $180,000.

(Source: https://www.lia.org.sg/media/1529/lia_protection_gap_study_2012_report_28aug12.pdf)

This however has changed with times with individuals now understanding the cost-effectiveness of getting term life insurance for protection. In the recent 2022 protection gap study, Term Life insurance is now the popular choice with most working adults, taking up the majority of life insurance coverage purchased. Additionally, the average life insurance coverage per person has increased significantly to $331,228 as compared to the lower coverage amounts seen in the 2012 protection gap study.

(Source: https://www.lia.org.sg/media/3974/lia-pgs-2022-report_final_8-sep-2023.pdf)

Cost of getting covered with a term life plan vs a whole life plan

If we were to compare getting coverage with a term life vs whole life plan, you will find that the cost of getting covered differs between the two. A 1 million term life policy will only cost $480.90 a year as compared to a 1 million whole life insurance which costs $7,301.50 per year. Therefore, if you are using a whole life insurance for protection coverage you may wish to relook your policies.

Term Life Insurance |

Whole Life Insurance |

|

Coverage amount |

1 million |

1 million up to age 65,

$500,000 from age 66 to 120 |

Coverage period |

Up to age 65 |

Up to age 120 |

Annual premiums |

$480.90 |

$7,301.50 |

Premiums payable for |

34 years |

34 years |

Total Lifetime premiums |

$16,351 |

$248,251 |

Profile: Age 30, non-smoker male. Quotations generated on 1 October 2024. The above figures are for illustration purposes.

3. Do you know who to look for if you need assistance with your policy?

Is your insurance agent still in business and available to help? If you are still relying on the insurance policies you purchased 10 to 20 years ago, then it's probably time for a review. From our experience, older policies can be hard to understand due to the lack of materials available. If you have such a policy, ask yourself:

Reach out to us for a complimentary review and get up to 45% commission rebates on your policies

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

You may also be interested in...

1 in 5 Singaporeans lack life insurance coverage. Are you the 1 in 5?

Insurance is your subscription plan against life's uncertainties

Information obtained from:

https://www.todayonline.com/singapore/insurance-body-revises-definition-severe-stage-critical-illnesses

https://www.straitstimes.com/singapore/health/life-insurers-to-change-definitions-of-critical-illnesses

https://www.lia.org.sg/media/1529/lia_protection_gap_study_2012_report_28aug12.pdf

https://www.lia.org.sg/media/3974/lia-pgs-2022-report_final_8-sep-2023.pdf

Information retrieved on 1 October 2024.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product.

This article is not a contract of insurance. Insurance products are underwritten by the respective insurance partners and distributed by iFAST.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to read the precise terms, conditions and exclusions specified in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and/or any of its third-party providers has/have tried to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")