Understanding MediShield Life and Integrated Shield plans:

MediShield Life |

Integrated Shield Plan (IP) |

Integrated Shield Plan (IP) riders |

|

Overview |

MediShield Life is a basic health insurance plan that offers universal coverage to all Singapore Residents. This means that all Singapore citizens and Permanent Residents (PRs) will be covered for life by MediShield Life regardless of pre-existing conditions or other life circumstances. |

Offered by seven private insurers, IP plans are an optional coverage that individuals can choose to purchase to get higher as-charged coverage. |

Add-on IP riders for additional benefit. This aims to reduce your out-of-pocket expenses and increase your cancer coverage. |

Administered by |

CPF board |

Seven private insurers |

Seven private insurers |

Provides coverage for |

Class B2/C wards in public hospitals |

Private hospital or Class A/B1/B2/C wards in public hospitals |

Reduce co-insurance, and deductibles and increase your cancer coverages |

Annual policy limit |

Up to $200,000 a year |

Up to $2 million a year |

N.A. |

With the recent revisions to MediShield Life benefits and premiums, here are some common questions you may have about your Shield plans and how to lower the cost of coverage.

1. Should I downgrade my hospital shield plan to reduce my premiums payable?

If you are unsure whether to downgrade your integrated shield plan, read our article on this here: My Integrated Shield plan premium is increasing; would lowering the cost of my hospital insurance compromise my coverage?.

In summary,

(Note: Class A wards at public hospitals are a single bed, air-conditioned room with attached bathroom and televisions.)

2. IP riders take up a substantial amount of my annual hospital insurance premiums. Should I cancel my IP rider to lower my premiums payable?

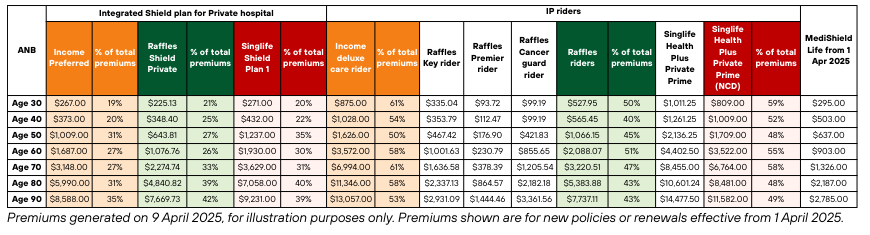

Integrated Shield plan (IP) riders offer additional benefits such as reducing your deductible payable and limiting your co-payment required for panel providers. IP riders also help to boost your coverage for cancer treatments on the cancer drug list.

While IP riders can be pricey with IP riders for private hospital shield plan contributing 43 to 61% to your total premiums payable, we feel that IP riders are a necessary part of getting comprehensive hospital coverage. This helps to reduce your out-of-pocket-expenses needed ensuring that you are well-covered should a medical emergency strike.

If you think that your premiums are getting too high and becoming unaffordable, you may wish to consider downgrading your IP plan while retaining your IP rider. Reach out to us here if you have any questions on your shield plans or would like a complimentary review.

3. Insurer ABC has a cheaper shield plan. Should I switch to Insurer ABC?

We do not recommend switching integrated shield plans between insurers as your new insurer may exclude coverage for pre-existing conditions.

Moreover, as premiums for IP plans and riders are age-banded this means that while premiums for your current insurer may be higher or lower now, future premiums are not guaranteed. Individuals may experience a lower premium now but higher premiums in future with the same insurer.

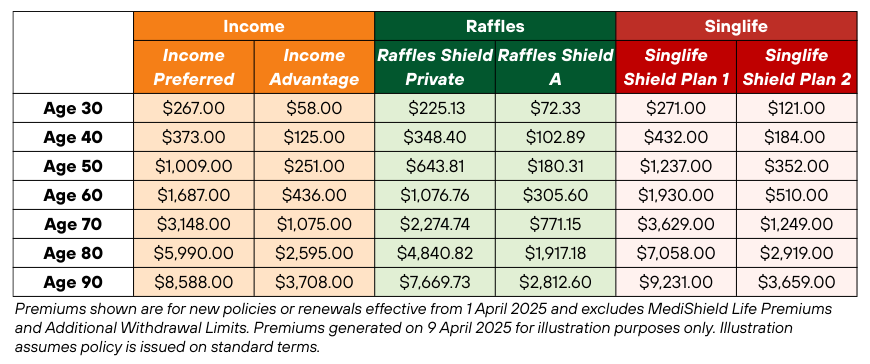

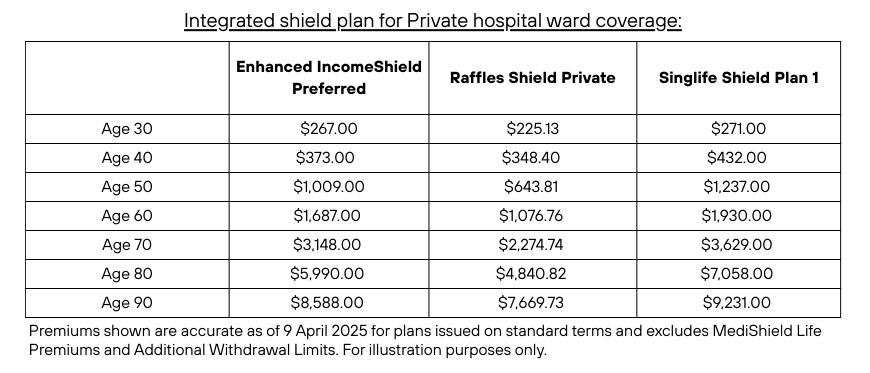

Note: Raffles Shield plans offers the lowest premiums for now as this is the only insurer where premiums remained unchanged by the April 2025 and September 2024 premium revisions.

Apart from premiums, do also consider the overall coverage offered by your shield plan provider. Some factors to consider are:

Enhanced IncomeShield |

Raffles Shield |

Singlife Shield |

Up to 23x MediShield Life limit per month when you choose Enhanced IncomeShield Preferred or Advantage and add a Deluxe Care or Classic Care rider. |

Capped at 23x MediShield Life limit per month if you choose Raffles Shield Private with Premier Rider and Cancer Guard Rider. |

Up to 20x MediShield Life limit per month when you choose Singlife Shield Plan 1, 2, or 3 and attach a Private Prime, Private Lite, Public Prime or Public Lite rider. |

Enhanced IncomeShield |

Raffles Shield |

Singlife Shield |

Panel: Over 600 specialists Extended panel: Over 200 specialists |

Panel: Over 150 specialists Extended panel: Includes specialist on another insurer’s panel of specialists. Requires pre-authorisation to be eligible for use as an extended panel. |

Preferred medical provider: Over 600 specialists |

Enhanced IncomeShield |

Raffles Shield |

Singlife Shield |

Up to $1.5 million annual policy limit. |

Up to $1.5 million annual policy limit for panel providers, and up to $600,000 for non-panel providers. |

Up to $2 million annual policy limit for preferred medical providers, and up to $1 million for other medical providers. |

4. Are there any other ways to help lower or reduce the cost of my hospital insurance?

Did you know that FSMOne offers up to 45% commission rebates on eligible shield plan and riders^? This is applicable to new purchases of shield plans.

You may also be interested in:

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Information obtained from:

https://www.income.com.sg/kcassets/7f849300-50f6-4239-aef7-3a8b8fec8232/Premium%20Table%20Deluxe%20Rider%20EIS.pdf

https://www.income.com.sg/kcassets/48ba2802-266a-4bec-b7cb-b61bff0e0f7c/Final%20Enhanced%20IncomeShield%20policy%20conditions%201%20Nov%202024.pdf

https://www.income.com.sg/specialist-panel

https://www.raffleshealthinsurance.com/wp-content/uploads/2021/03/Raffles-Cancer-Guard-Rider-Standalone-App-form-and-Product-Summary-1-April-2024-Final.pdf

https://www.raffleshealthinsurance.com/wp-content/uploads/2021/03/Raffles-Shield-Booklet-with-GIRO-Version-3.8.5-April-2025.pdf

https://www.raffleshealthinsurance.com/products/raffles-shield/raffles-shield-specialists/find-a-specialist/

https://singlife.com/content/dam/public/sg/documents/singlife-shield-and-health-plus-premiums.pdf

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-shield/singlife-shield-policy-contract-2025.pdf

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-shield/singlife-health-plus-policy-contract-2025.pdf

https://singlife.com/en/medical-insurance/medicalspecialists

Information retrieved on 9 April 2025.

Disclaimer(s):

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice. More information on iFAST Digital Term can be found here: https://secure.fundsupermart.com/fsmone/insurance/ifast-digital-term.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.