' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Changes to MediShield Life (MSHL)

Following the recommendations from the MediShield Life council in October 2024, the MediShield Life scheme will be enhanced with the revised benefits progressively implemented. Some of these changes will be implemented with effect from 1 April 2025. This is what we know about the changes that have been implemented and the other changes that will be implemented over the next few years.

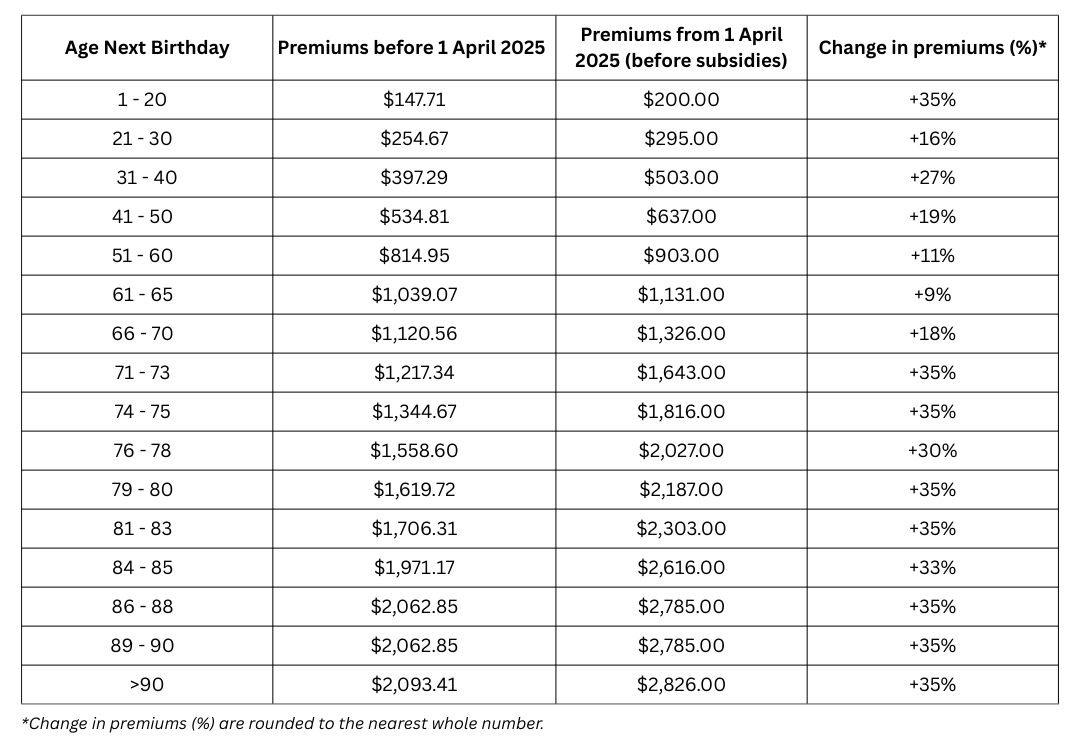

1) Premiums before subsidies will increase by as much as 35 per cent from April 2025

Our MediShield Life premiums will increase with this done in phases from April 2025 to March 2028. Premium support will also be given for 2025 and 2026 to help cushion the impact of this premium adjustment. As at time of writing, the new premiums have been implemented and will take effect for policies purchased or renewed on or after 1 April 2025.

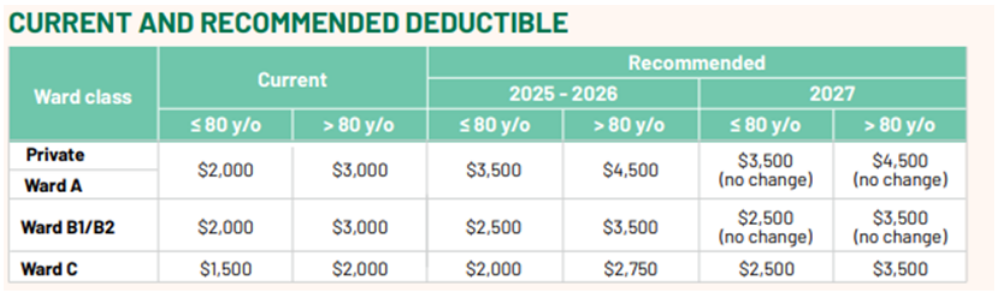

2) Inpatient deductible will increase by up to $1,500

One of the main changes announced in October 2024 was the increase of inpatient deductible for MediShield Life. The current inpatient deductible ranges from $1,500 to $3,000 and has remained unchanged since MediShield Life was introduced in 2015. This deductible was initially implemented to sieve out smaller medical bills, keep premium increases in control and allow MediShield Life to focus on the larger bills. However, the rising medical bills has deemed this deductible insufficient at achieving its intended cause.

The MediShield Life council has recommended the inpatient deductible to increase by up to $1,500 with this increase to be done in phases over the next three years. While the first increase in inpatient deductible was initially set for April 2025, as at time of writing we have not been able to find any confirmation that the new inpatient deductible has taken effect.

(Source: MediShield Life report 2024)

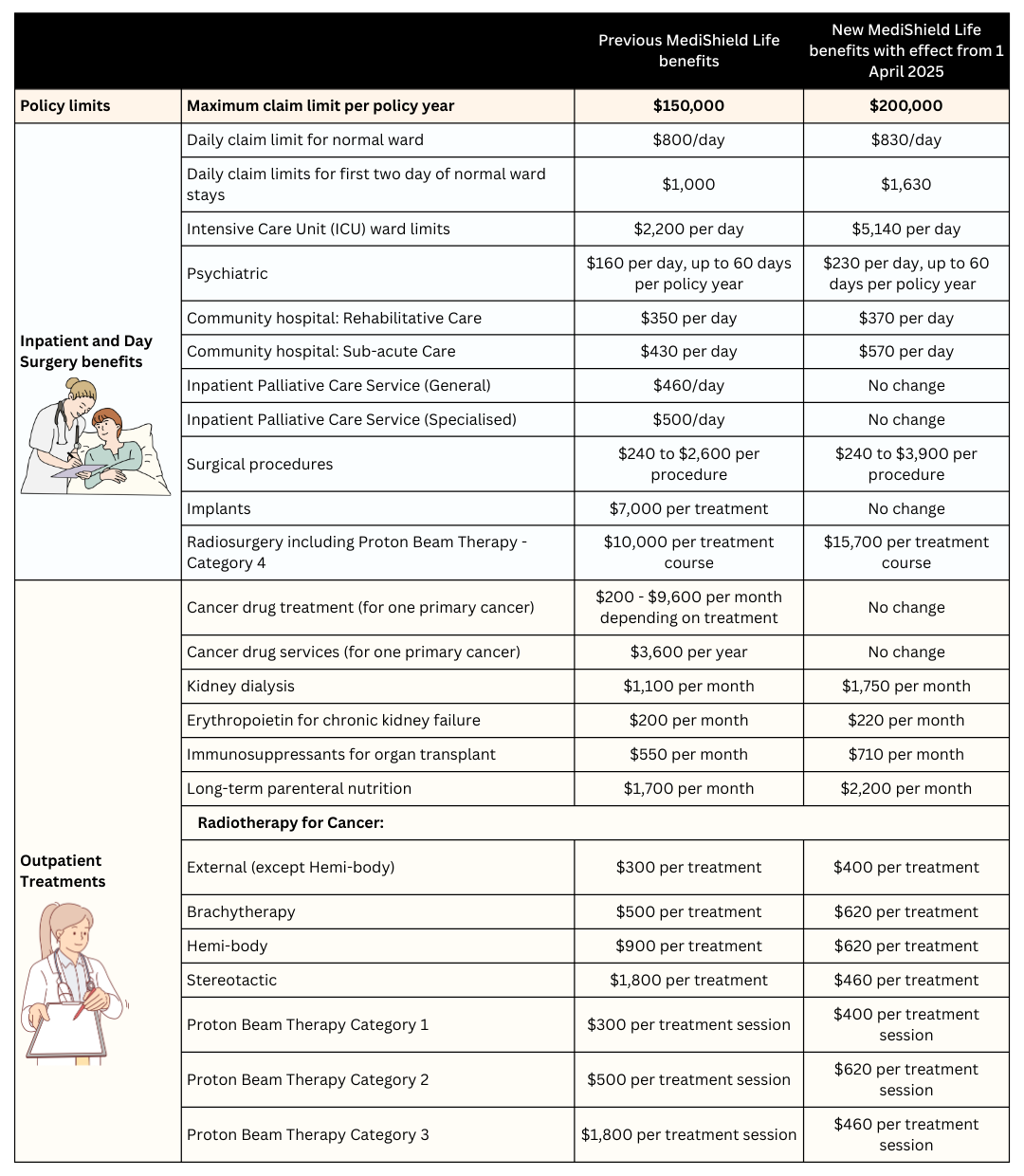

3) Increase in maximum claim limits and other benefits

Apart from premium increases and the increase in deductibles, the revised MediShield Life will also offer higher benefit limits. The annual policy claim limit has been increased from $150,000 to $200,000 among other things.

We summarised a list of benefit changes between the new and old MediShield Life in the table below:

(Source: MediShield Life report 2024)

With the updates to MediShield Life, there has also been changes to Integrated Shield plans. Here are the changes:

Premium revision: Premiums are revised for foreigner rates to all Enhanced IncomeShield plans, IncomeShield Plan P, IncomeShield Plan A and IncomeShield Standard Plan effectivefrom April 2025. There are no changes to the premiums of riders.

Changes to benefit: No changes.

Premium revision: Singlife Shield and Singlife Health Plus premiums will be raised from 1 April 2025. Premiums for Singlife will now increase gradually with age instead of by broad age bands.

Changes to benefit: There are four main changes to the benefit for Singlife Shield plans:

Old benefit |

New benefit with effect from 1 April 2025 |

|

Inpatient and Outpatient Cell, Tissue and Gene Therapy |

$150,000 per policy year. |

$150,000 per treatment per lifetime. Each CTGTP treatment is only claimable once under the policy. |

Cap for co-insurance treatment at non-preferred medical providers |

Capped at $12,750 per policy year. |

No cap for co-insurance treatment at non-preferred medical providers. No changes for treatments at preferred medical providers.r. |

Children benefit |

Children get free cover if conditions are met. |

Free cover removed and converted to family discount for children benefit upon policy renewal. |

No Claims Discount (NCD) for Singlife Health Plus |

15% if the total claim payout amount during the assessment period is less than or equal to S$1,000. |

20% if the total claim payout amount during the assessment period is equal to S$0. |

Premium revision: No revisions made to premiums.

Changes to benefit: No changes.

If you have existing shield plans with Income, Raffles or Singlife, you may also be interested in:

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Information obtained from:

https://www.cpf.gov.sg/member/healthcare-financing/medishield-life/what-medishield-life-covers-you-for

https://isomer-user-content.by.gov.sg/3/c33f49bb-869d-4ff0-88ef-755e9602402d/medishieldlife-report-2024.pdf

https://www.moh.gov.sg/managing-expenses/schemes-and-subsidies/medishield-life/medishield-life-premium-and-subsidy-tables

https://www.moh.gov.sg/newsroom/government-accepts-medishield-life-council-s-recommendations-to-enhance-medishield-life-scheme---government-support-more-than-offsets-premium-increases

https://singlife.com/content/dam/public/sg/documents/promotion/H44%20Singlife%20Shield%20TCs%20Sept%202024.pdf

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-shield/singlife-shield-policy-contract-2025.pdf

https://singlife.com/content/dam/public/sg/documents/promotion/H46%20Singlife%20Health%20Plus%20TCs%20Sept%202024.pdf

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-shield/singlife-health-plus-policy-contract-2025.pdf

Information retrieved on 3 April 2025.

Disclaimer(s):

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice. More information on iFAST Digital Term can be found here: https://secure.fundsupermart.com/fsmone/insurance/ifast-digital-term.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")