' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

A brief recap on MediShield Life and the Integrated Shield (IP) plans offered by Singlife,

(Read: Is private hospital insurance really necessary?)

In this article, we study the benefit and premium differences between Singlife Shield Plan 1 and Plan 2 to determine if it is worth paying for the higher-tier Plan 1, or if you should downgrade to a Class A ward plan.

Singlife Shield Plan 1 |

Singlife Shield Plan 2 |

Singlife Shield Plan 3 |

MediShield Life (MSHL) |

|

Ward entitlement |

Standard ward of a private hospital |

Standard ward A of public hospital |

4-bed standard ward B1 of a public hospital |

Class B2/C wards in public hospitals |

Annual policy limit |

Up to $2,000,000 |

Up to $1,000,000 |

Up to $500,000 |

$150,000 |

What the different hospital ward classes mean:

#1 Difference in benefits between Singlife Shield Plan 1 and Plan 2

Wondering which Singlife Shield plan is right for you? Here are the notable differences between the plans to help you determine if the higher-tier plan is worth the difference in premiums.

Differences in Singlife Shield Plan 1 and Plan 2 |

Similarities in Singlife Shield Plan 1 and Plan 2 |

List of differences and similarities are for illustration purposes only. Please refer to your policy wording for more information. Information retrieved on 4 November 2024.

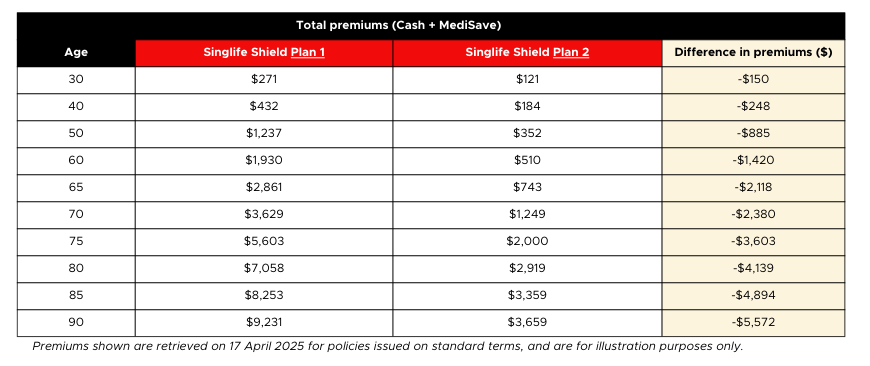

Premiums between Shield Plan 1 and Plan 2 will also vary with this difference going up to as much as over 3 times.

#2 Do the riders matter?

The addition of an IP rider is intended to (1) Reduce annual deductible needed (2) Lower or cap the co-insurance payable, and (3) Increase cancer treatment limits.

Here are the notable differences in the various riders:

[💡 Lite plans have a ward downgrade benefit where 50% of your Singlife Shield annual deductible is covered if the insured chooses to stay at a ward class lower than his chosen plan]

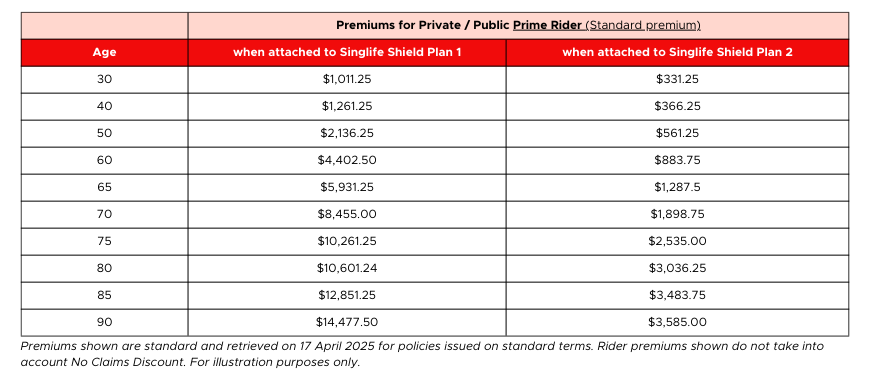

In addition to the premium differences between IP plans, premiums for Health Plus Prime rider will also vary according to the IP plan that it is attached to. For example, when attached to Singlife Shield Plan 1, the prime rider has premiums of 2 to 4 times higher than when attached to Singlife Shield Plan 2.

Are the benefits worth the premiums payable? This is what we think:

If you are comfortable with the current premiums -

We recommend that you continue with your current plan until the premiums become unaffordable as it is generally easier to downgrade or remove a rider than to upgrade your coverage in future. At that point, review your needs to assess whether there have been any significant changes to your hospital plan requirements.

If you would like to relook your hospital coverage and lower your premiums payable,

1. To seek treatment at Class A wards: Downgrade to Singlife Shield Plan 2 but keep your Prime rider

One way to reduce your payable premium is to downgrade your IP plan but keep your rider. By doing so you will experience:

Your co-insurance is reduced from 10% to 5% with the addition of a Prime or Lite rider. The maximum co-insurance needed per policy year is also capped at a lower amount. Without a rider, Singlife Shield Plan 1, 2, and 3 caps the 10% co-insurance at $25,500 per policy year for treatment at A&E or preferred medical providers. With the addition of a Prime rider, the co-insurance needed is capped at $3,000 per policy year for A&E or preferred medical providers.

Additionally, Prime rider removes the annual deductible which significantly lowers out of pocket expenses required.

Medical bill from a preferred provider |

Deductible needed for Ward A |

Co-insurance payment needed |

Total out of pocket expense needed |

|

Singlife Shield Plan 1 |

$100,000 |

$3,500 |

($100,000 - $3,500) x 10% = $9,650 |

$3,500 + $9,650 = $13,150 |

Singlife Shield Plan 1 + Private Prime |

$100,000 |

Not applicable |

$100,000 x 5% = $5,000 (but capped at $3,000 with Private Prime rider) |

$3,000 |

Singlife Shield Plan 2 + Public Prime |

$100,000 |

Not applicable |

$100,000 x 5% = $5,000 (but capped at $3,000 with Public Prime rider) |

$3,000 |

Illustration assumes individual sought treatment at a preferred provider. Information generated on 4 November 2024, for illustration purposes only.

With MediShield Life (MSHL), your cancer coverage is limited to just $200 - $9,600 per month for drugs on the Cancer Drug List (CDL) and Cancer drug services claims are limited to $3600 per annum. No coverage is given for non-CDL treatments. To receive higher cancer coverage, opt for a Prime rider that will provide both CDL and non-CDL coverage.

With the addition of a prime rider, you can receive up to 20 times the MSHL benefit limit per month for treatments on the CDL. You will also receive up to $15,000 per month for non-CDL treatments.

MediShield Life (MSHL) |

Singlife Shield Plan 1 |

Singlife Shield Plan 2 |

With a Private or Public Prime rider |

|

Outpatient Cancer Drug Treatment each month on the Cancer Drug List (CDL) for one primary cancer |

$200 - $9,600 per month depending on cancer drug treatment |

5x MSHL Limit for one primary cancer |

5x MSHL Limit for one primary cancer |

Additional 15x MSHL limit for one primary cancer. This gives you 20x MSHL monthly claim limit for treatments on CDL for one primary cancer. |

Outpatient cancer drug services per policy year |

$3,600 per year for Cancer drug services. |

5x MSHL limit for one primary cancer. |

5x MSHL limit for one primary cancer. |

N.A. |

Outpatient cancer drugs benefit each month for one primary cancer (Non-CDL) |

No coverage provided. |

No coverage provided. |

No coverage provided. |

$15,000 per month, subject to co-insurance. |

Co-insurance payment needed for CDL treatment |

10% co-insurance |

10% co-insurance (capped at $25,500 per policy year) |

10% co-insurance (capped at $25,500 per policy year) |

5% co-insurance (capped at $3,000 per policy year for A&E and preferred panel; and $12,760 per policy year for other providers) |

Co-insurance payment needed for non-CDL treatment |

N.A. |

N.A. |

N.A. |

5% co-insurance (no cap on amount payable) |

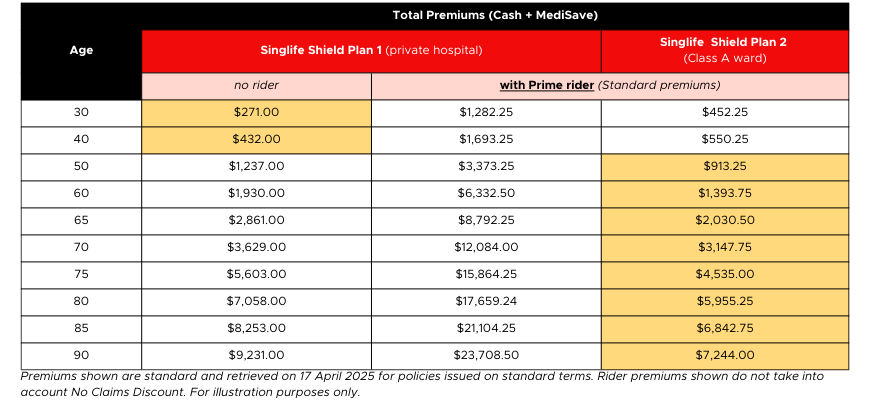

Moreover, switching to Singlife Shield Plan 2 and adding a Public Prime rider can still be cheaper than a Plan 1 alone. This difference in premiums can be seen in the table below.

2. If you still want private hospital coverage and do not mind paying the annual deductible: Switch your Private Prime rider to a Private Lite rider

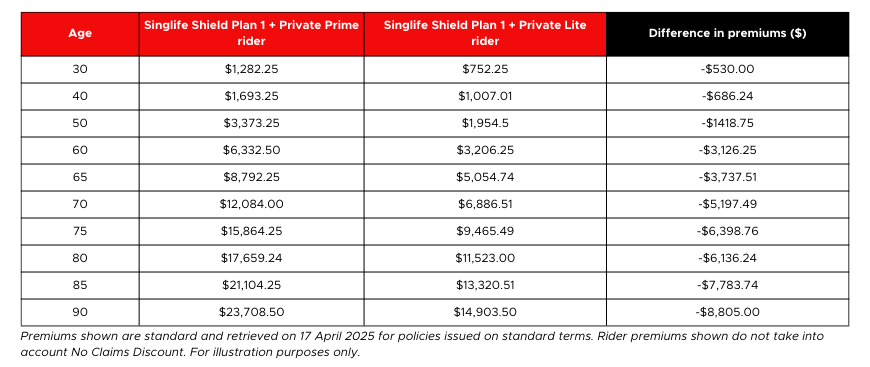

Alternatively, to reduce your premiums payable while maintaining private hospital coverage, consider switching your IP rider from Private Prime to Private Lite. Here are the factors to consider for this option.

While the Private Prime rider reduces your annual deductible for A&E or preferred providers to $0, you will have to pay this annual deductible with a Private Lite rider. However, for an insured under the age of 80, the current annual deductible amount for Singlife is just $3,500 for treatment at a private hospital. This annual deductible needed goes up to $5,250 for an individual age 81 and above.

[💡 The current difference in premiums is $3,264 between Singlife Shield Plan 1 + Prime Rider and Singlife Shield Plan 1 + Private Lite rider for an age 80 individual.]

Moreover, if you require treatment and would like to reduce the annual deductible payable, you may also downgrade your ward stay. This will reduce your annual deductible payable by 50%.

Switching to Private Lite rider will reduce your premiums by between 29 and 44 per cent as shown in the table below.

While you will have to pay the deductible with a Private Lite rider, this rider still reduces your co-insurance needed to 5%. Co-insurance is also capped at $3,000 thus making your total out of pocket expenses needed still much lower than if you were to only have an IP plan.

Medical bill from a preferred provider |

Deductible needed for Ward A |

Co-insurance payment needed |

Total out of pocket expense needed |

|

Singlife Shield Plan 1 |

$100,000 |

$3,500 |

($100,000 - $3,500) x 10% = $9,650 |

$3,500 + $9,650 = $13,150 |

Singlife Shield Plan 1 + Private Prime |

$100,000 |

Not applicable |

$100,000 x 5% = $5,000 (but capped at $3,000 with Private Prime rider) |

$3,000 |

Singlife Shield Plan 1 + Private Lite |

$100,000 |

$3,500 |

($100,000 - $3,500) x 5% = $4,825 (but capped at $3,000 with Private Lite rider) |

$3,500 + $3,000 = $6,500 |

Have a question? Speak to us about your shield plans here:

Click the button below if you would like to review or downgrade your Singlife Shield plan, or seek a second opinion on your hospitalisation coverage.

If you have existing shield plans with Income, Raffles or Singlife, you may also be interested in:

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://www.moh.gov.sg/managing-expenses/schemes-and-subsidies/medishield-life/medishield-life-benefits#Cancer-Drug-List

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-health-plus/premium-rates.pdf

https://singlife.com/content/dam/public/sg/documents/promotion/H44%20Singlife%20Shield%20TCs%20Sept%202024.pdf

https://singlife.com/content/dam/public/sg/documents/promotion/H46%20Singlife%20Health%20Plus%20TCs%20Sept%202024.pdf

Information retrieved on 4 November 2024.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")