' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Why are there changes

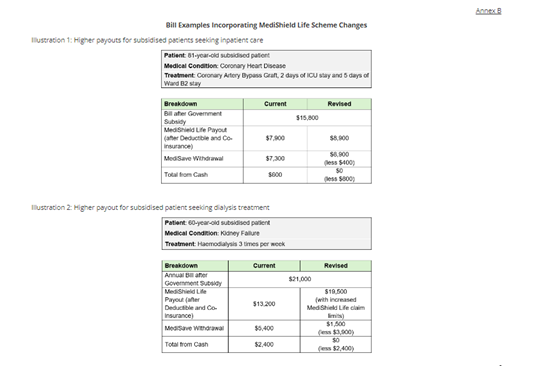

Administered by the Central Provident Fund (CPF) Board, MediShield Life is a basic health insurance that protects all Singapore Citizens and Permanent Residents (PRs) against large medical bills and selected costly outpatient treatments. Designed to cover nine in ten subsidised bills at public healthcare institutions, this coverage has now dropped to cover just under eight in ten bills due to the rising medical costs. Changes thus aims to restore MediShield Life’s benefit back to covering nine in ten subsidised bills.

What are the changes

Changes will be implemented progressively from April 2025 onwards with some changes implemented in phases. Here are the key changes to your MediShield Life (MSHL).

1. Coverage limits

The revised MediShield Life will offer better coverage and fully cover nine in ten subsidised bills. For this, MediShield Life will increase claim limits for:

2. Expanded coverage

To address medical advancements and the shift in our healthcare needs:

3. Deductible and Co-insurance

To moderate premium impact and keep larger bills affordable, new MSHL will implement:

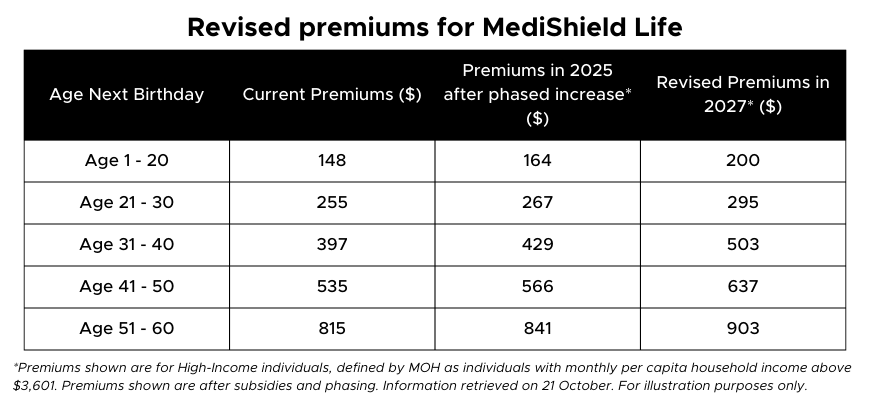

4. Premium adjustments

With the changes to MediShield Life, do I still need an Integrated Shield plan?

The new MediShield Life is intended to fully cover nine in ten subsidised bills in public healthcare institutions. If you are comfortable with seeking treatment at Class B2/C wards in public hospitals, then MediShield Life should sufficiently address your needs.

To recap, B2/C wards are naturally ventilated rooms with up to 6 beds in a ward. Rooms may not have attached bathrooms and televisions.

If you are currently only on MediShield Life and would like higher coverage:

Designed as a no-frills product, benefits for standard IP plans are determined by the Government and are identical across all IP insurers. This offers a standardised affordable option for additional coverage beyond MediShield Life.

While the standard B1 ward IP plan and the new MediShield Life plan both have an annual policy limit of $200,000, Standard IP offers higher coverage limits for both inpatient and outpatient treatments. Some of the difference in benefits can be found in the table below:

Current MediShield Life |

New MediShield Life with effect from April 2025 |

Standard Integrated Shield plan (B1 ward) |

|

Annual policy claim limit |

$150,000 |

$200,000 |

$200,000 |

Co-insurance |

Flat 10% |

Tiered structure ranging from 3% to 10% |

10% |

Inpatient and day surgery limits |

|||

Daily claim limit for first two days of normal ward stays |

$1,000 |

$1,630 |

$2,550 |

Intensive Care Unit (ICU) ward limits |

$2,200 per day |

$5,140 per day |

$6,850 per day |

Psychiatric |

$160 per day, up to 60 days per policy year |

$230 per day, up to 60 days per policy year |

$680 per day, up to 60 days per policy year |

Community hospital: Rehabilitative Care |

$350 per day |

$370 per day |

$760 per day |

Surgical procedures |

$240 to $2,600 per procedure |

$240 to $3,900 per procedure |

$590 to $21,480 per procedure |

Outpatient claim limits |

|||

Cancer drug treatment (for one primary cancer) |

$200 - $9,600 per month depending on treatment |

No change |

3x MSHL limit per month |

Cancer drug services (for one primary cancer) |

$3,600 per year |

No change |

2x MSHL limit per year |

Radiosurgery including Proton Beam Therapy - Category 4 |

$10,000 per treatment course |

$15,700 per treatment course |

$31,300 per treatment course |

Kidney dialysis |

$1,100 per month |

$1,750 per month |

$3,740 per month |

Information in table is for illustration purposes only and are non-exhaustive. Please refer to the policy wording for more information. Information retrieved on 21 October 2024.

IncomeShield Standard Plan |

Singlife Shield Standard |

Raffles Shield Standard |

|

Age 20 |

$36.00 |

$46.86 |

$39.73 |

Age 30 |

$45.00 |

$50.94 |

$48.90 |

Age 40 |

$67.00 |

$71.31 |

$63.15 |

Age 50 |

$140.00 |

$137.53 |

$127.33 |

Age 60 |

$176.00 |

$169.10 |

$166.05 |

Age 65 |

$242.00 |

$292.36 |

$280.14 |

Premiums retrieved on 21 October 2024, and are for illustration purposes only.

While Standard B1 ward plans are a step up from MediShield Life’s benefits, coverage from these plans are still not as comprehensive as Class A ward or private hospital IP plans. For example, Standard B1 IP plans do not provide as-charged coverage. Pre and post hospitalisation treatments are also not covered in Standard B1 IP plans.

For Class B1 ward entitlements with as-charged coverage and higher benefits, consider Enhanced IncomeShield Basic, Singlife Shield Plan 3, or Raffles Shield B.

(Read: A Guide to assessing your Enhanced IncomeShield plan)

For private hospital treatments, or to further enhance your coverage:

If you would like to get as charged coverage, opt for a Class A or Private hospital IP plan. Not only will this give you as charged coverage for inpatient and outpatient treatments, but you will also receive additional benefits such as coverage for pre and post hospitalisation treatments.

With integrated shield plans, you will get:

Have a question? Click the button below to speak to us:

If you are unsure on which hospitalisation plan you need, or would like a second opinion for your policies.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://www.moh.gov.sg/news-highlights/details/government-accepts-medishield-life-council-s-recommendations-to-enhance-medishield-life-scheme---government-support-more-than-offsets-premium-increases

https://www.straitstimes.com/singapore/health/medishield-life-to-offer-higher-claim-limits-better-coverage-premiums-to-rise-from-april-2025

https://www.moh.gov.sg/healthcare-schemes-subsidies/medishield-life/medishield-life-faqs#sisp

Information retrieved on 21 October 2024.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")