Investment, insurance or forced savings - what are endowments to you? A controversial product, many may lack proper understanding on endowments thus resulting in endowments being seen in a negative light. Low returns and a long lock-in period, these are just some of the cons of an endowment. But are endowments necessarily bad?

What are endowments?

A disciplined way to save, endowments are also known as a savings plan. Offered on a regular premium or single premium basis, endowments are a participating plan and will accumulate cash values. These cash values comprise of both guaranteed and non-guaranteed components and will be paid to the policy holder at maturity.

(See "3 Reasons An International Health Plan Is For You")

Cons of an endowment plan

1. Your capital is not always guaranteed at maturity

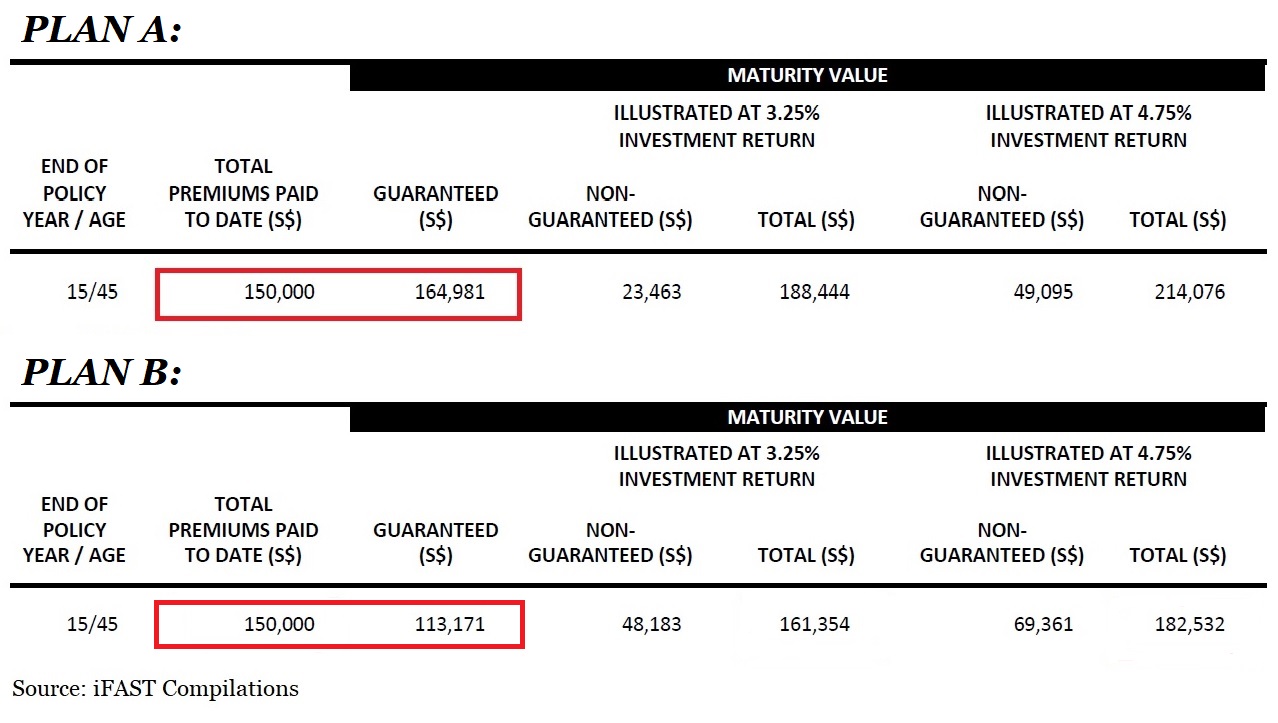

While there may be the misconception that an endowment plan is capital guaranteed at maturity, this is not necessarily so. Take for example the two endowment plans as shown below, while Plan A is capital guaranteed at maturity, Plan B is not.

However, this is not to say that a capital guaranteed endowment is better than a non-capital guaranteed endowment. With factors such as a higher non-guaranteed component or yearly income affecting the guaranteed value at maturity, understanding the intention of endowments will ensure that the plan you choose is suitable for you.

(See "When Is Whole Life Insurance The Better Option?")

2. Projected returns are non-guaranteed

The benefit illustration of an endowment plan will show a projected investment return of 3.25% or 4.75%. However, do note that this is not guaranteed as the actual amount received will be subjected to the performance of the insurer's investment.

3. Long commitment period

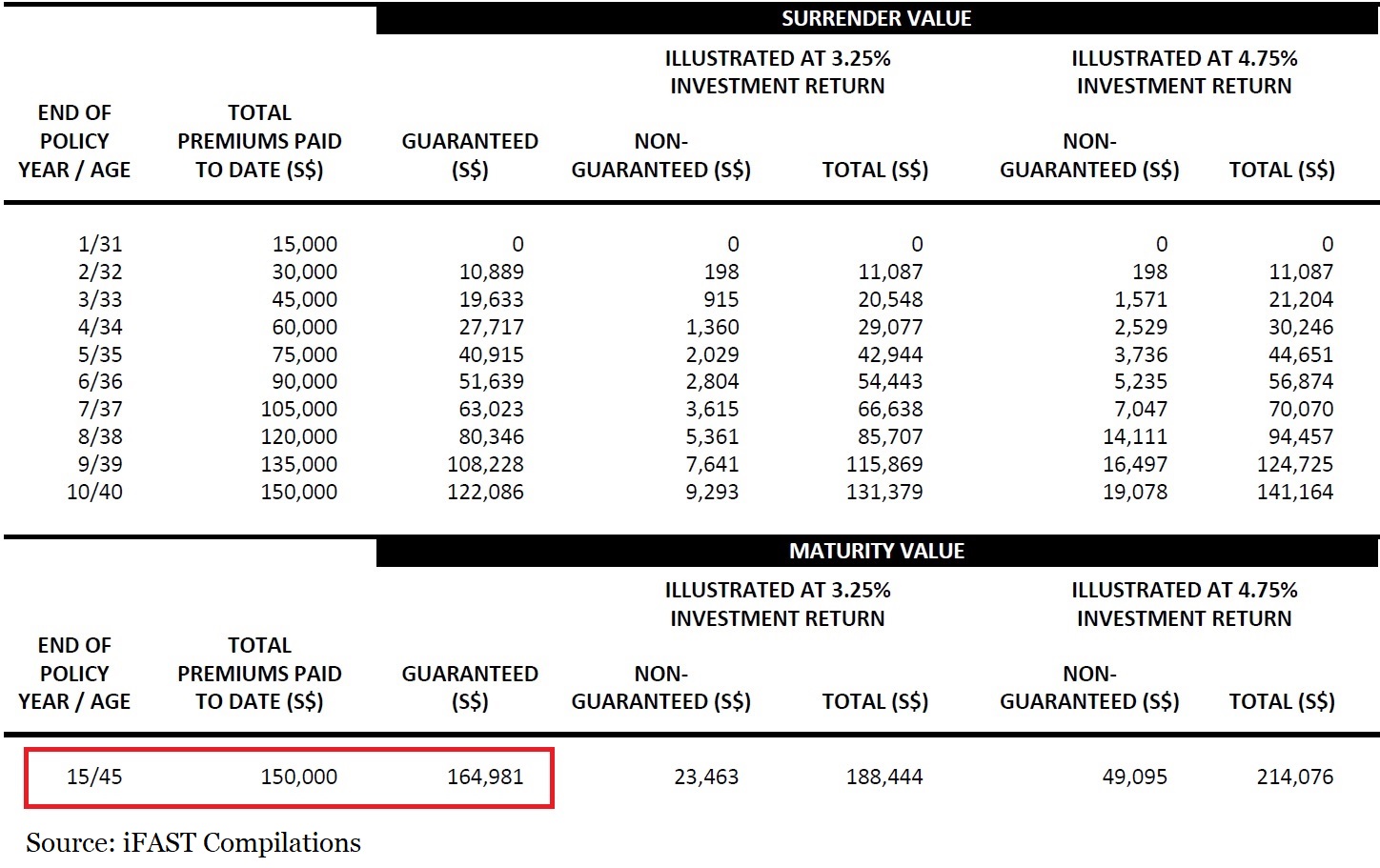

Endowments have low liquidity with the lock-in period typically between 10 to 25 years. While you can terminate your plan before maturity, doing so can be costly and is not advisable. As shown in the image above, the guaranteed value is only equal to the total premiums paid at maturity. Should you terminate your plan before maturity, you would then lose a portion of the premiums that you have paid to date. Therefore, to reap the full returns of the endowment, you are required to commit to the policy term and hold the endowment plan until maturity.

(See "Should You Purchase Critical Illness Insurance Before 2020?")

But are endowments necessarily bad?

However, while naysayers may say otherwise, we feel that endowments are not necessarily bad. This is because endowments are suitable should you find yourself in these situations:

1. If you have trouble sticking to a saving plan

With early terminations penalised, individuals are unlikely to make any withdrawals unless absolutely necessary. This deterrence “forces” individuals to save thus helping those who have trouble saving. Moreover, while endowments are less liquid, this could actually work in your favour as it ensures that you achieve what you set out to do for your finances.

(See "Your Cheatsheet To The 2020 Holidays")

Simple, high coverage, affordable. Insurance done right for your family.

2. If you are planning for your child's education

You may also consider using endowments to plan for your child’s education. With a portion guaranteed at maturity, you can choose to coincide when your endowment matures with when you will need the money for your child’s education.

Additionally, some endowments have the option for an add-on premium waiver rider allowing future premiums to be waived in the event of the parents' demise. This ensures that the endowment plan will not terminate and will continue until maturity should anything untoward happen to the parents. With endowments, you can protect your child’s future, knowing that he/she will not be denied of an education as a result of financial constraints.

(See "The True Cost Of Raising A Child In Singapore")

3. If your risk appetite is low

Endowments are not investments and therefore they are not subjected to market volatility. Protected by the Policy Owner’s Protection Scheme (PPF Scheme), endowment plans are guaranteed in the event of the failure of the insurer.1 This acts as a safety net for your policy and offers 100 per cent protection for your guaranteed benefits thus providing a peace of mind.

Additionally, while the surrender value of endowments before maturity may not be as attractive, having a surrender value reassures knowing that you have access to your money in the event of an emergency.

(See "3 Tips For The Best Retirement Strategy")

While endowments may be an insurance product, endowments provide minimal protection coverage. Therefore, we do not recommend using endowments for protection planning. Instead, consider using endowments to help achieve your savings or financial goals.

Endowments are suitable for:

Endowments are not suitable for:

Available Endowments on FSMOne Insurance: |

Etiqa Insurance - eFUTURE pay presto, eSAVE assure presto Manulife - ReadyPayout Plus, Ready Builder, ManuWealth Secure NTUC Income - Gro Goal Saver, Gro Steady Saver, Gro Retire Ease, Gro Junior Saver, Gro Secure Saver, Gro Saver Tokio Marine - TM Nest Egg (GIO), TM Nest Egg (Cashback 8/10), TM Wealth Enhancement, TM KidStart |

If endowments are not for you, you may consider alternatives such as short term duration bonds, regular saving plans (RSP) or Singapore Saving Bonds.

Over 6,900 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment from Etiqa Insurance, Manulife, NTUC Income and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

1Source: https://www.sdic.org.sg/calc/pop_calc

Interested to learn more? Check out these articles:

Cheap Car Insurance Singapore 2020

I Already Have CPF Life, Do I Still Need Annuities?

3 Things Your 20 Years Old Policy May Not Tell You

Best Cancer Insurance Singapore

4 Mistakes All Couples Must Avoid Making With Their Finances