What is Whole Life Insurance?

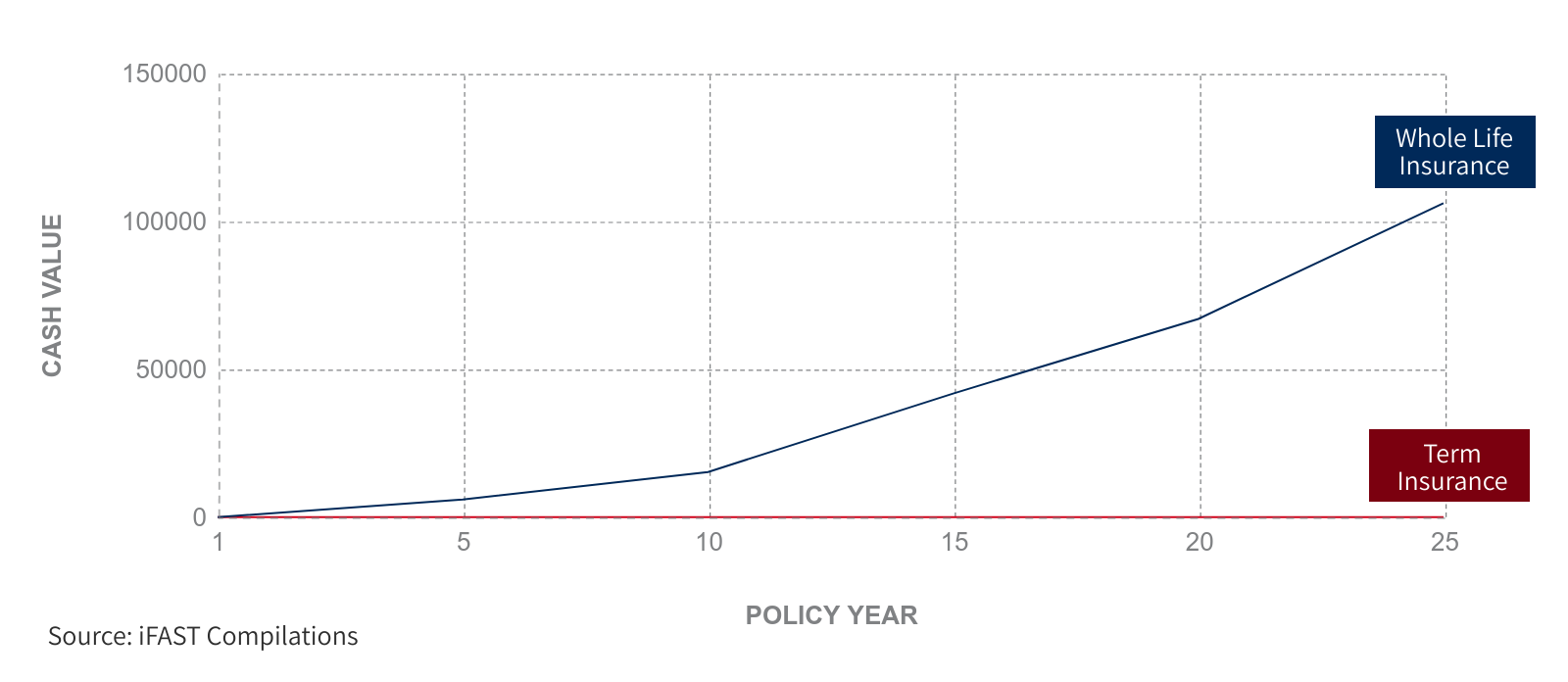

Whole life insurance offers coverage for life and is commonly used for protection and legacy planning. This is unlike term insurance that only provides coverage for a specified period.

With knowledge that you will remain insured for the rest of your life and have your legacy passed on to future generations, whole life insurance allows for a peace of mind. Plans are usually offered on a participating basis and will accumulate cash value thus allowing you to cash out should the need arise.

(See "Comparing Whole Life Insurance 2019")

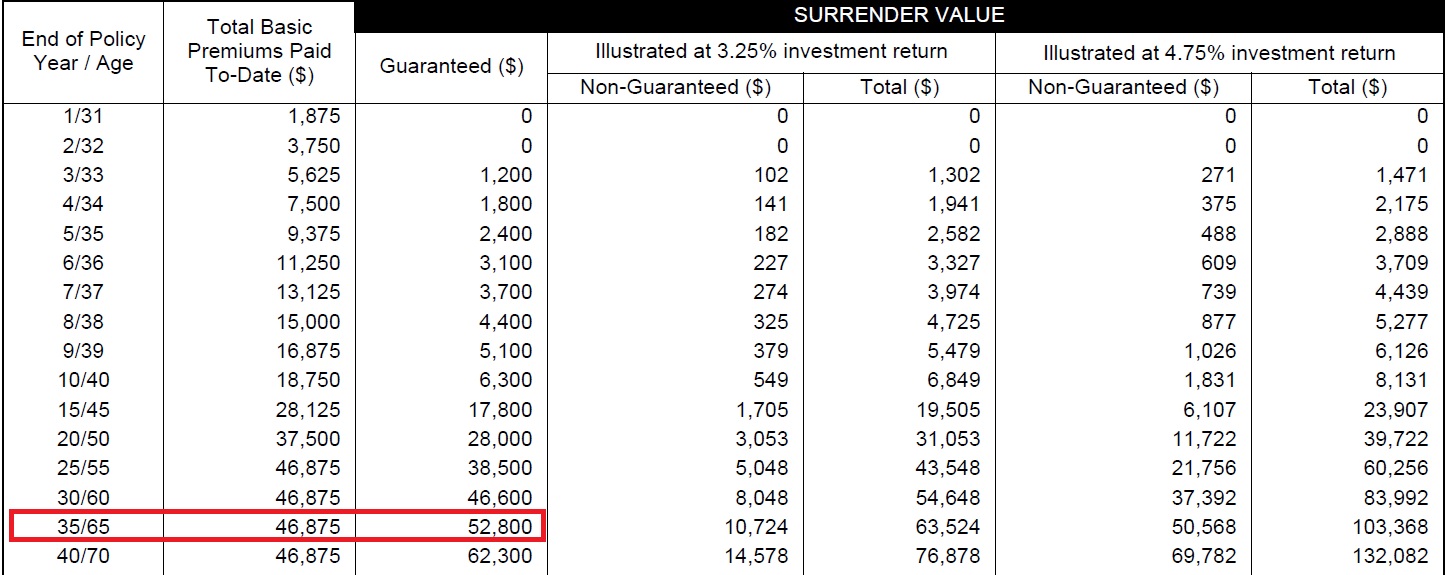

#1 When you surrender your whole life insurance at age 65

While term insurance is commonly used to fill a temporary protection gap, these plans are non-participating and have no cash value. This means that at the end of the policy term, your term insurance coverage will conclude with no option to cash out.

However, whole life insurance plans will accumulate cash value. As shown in the image below, your policy's accumulated cash value would be equal to the total basic premiums paid-to date at age 65. Using a whole life insurance and cashing out only after age 65 would then allow you to enjoy "free coverage".

Do note that whole life insurance is generally more expensive than term insurance. Therefore, consider this option only if you are comfortable with the annual premiums required.

(See "Your Cheatsheet To The 2020 Holidays")

Simple, high coverage, affordable. Insurance done right for your family.

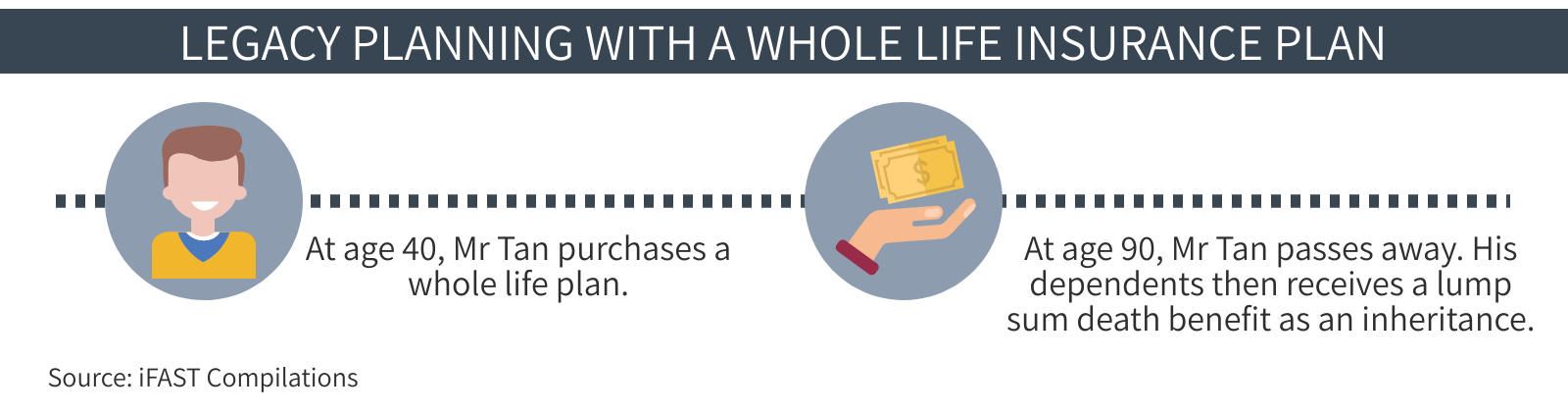

#2 For legacy planning

Apart from providing protection, whole life insurance can also be used for legacy planning. With coverage for life or up to the age of 99, this ensures that your dependents will receive a lump sum after you pass on.

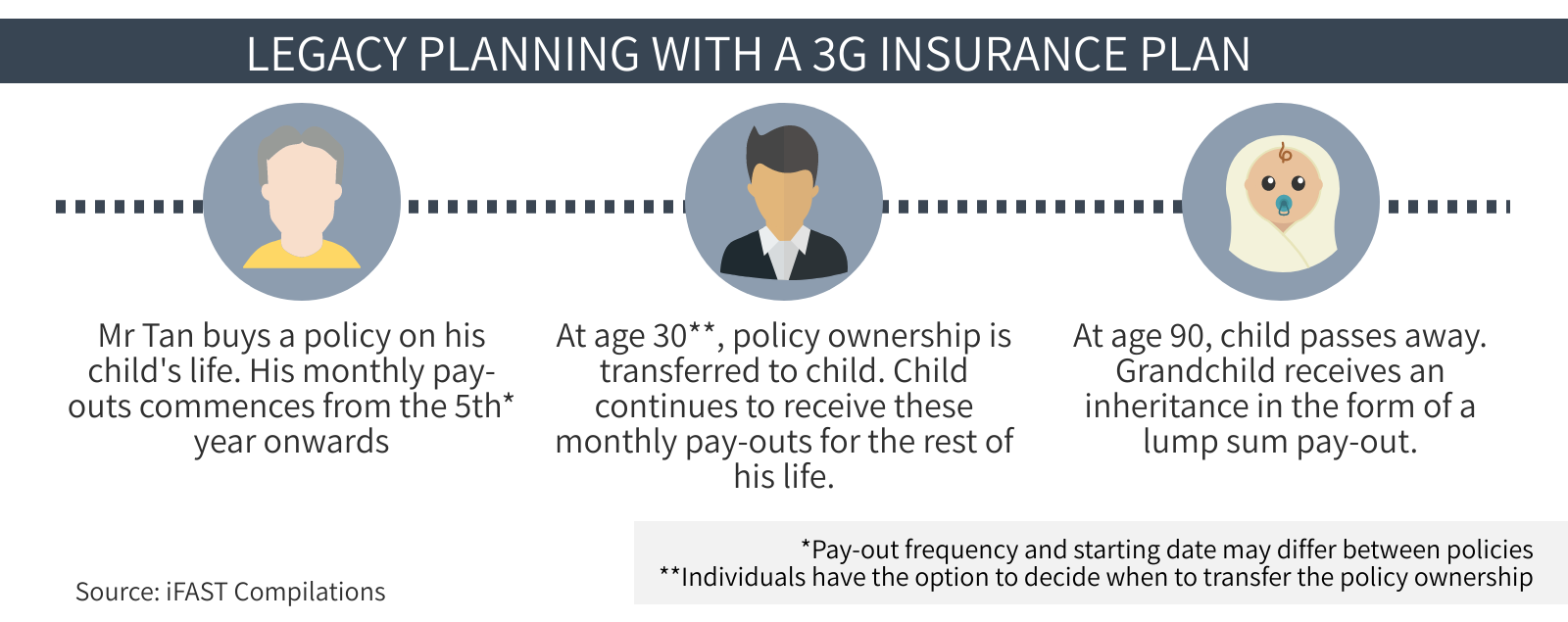

Alternatively, consider 3 generation (3G) plans for wealth preservation and to transfer of wealth to future generations. Giving the first two generations a regular stream of income and the third generation a lump sum pay-out as inheritance, 3G plans ensures wealth continuity for 3 generations.

(See "Transfer Your Wealth To Future Generations With A 3G Plan")

#3 Using your whole life insurance for additional retirement income

As mentioned in "3 Tips For The Best Retirement Strategy", the best retirement income strategy comprises of optimising CPF Life pay-outs and devising ways to receive a lifetime of pay-outs. While policy conditions differ between plans, some whole life insurance plans offer the option for regular pay-outs. This may be guaranteed and/or non-guaranteed pay-outs and can be used as part of your retirement planning.

(See "With My Corporate Cover, Do I Still Need Health Insurance?")

Whole life insurance is suitable for:

Whole life insurance is not suitable for:

Available Whole Life Insurance |

Etiqa Insurance - ePREMIER Diamond, ePREMIER Legacy III, ePREMIER Legacy IV Manulife - LifeReady Plus, Ready LifeIncome, Signature Income NTUC Income - Star Assure, Wealth Solitaire Tokio Marine - TM Legacy Lifeflex |

Over 6,900 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment from Etiqa Insurance, Manulife, NTUC Income and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Should You Purchase Critical Illness Insurance Before 2020?

The 5 Factors Affecting Your Car Insurance Premiums