Are you aware of the limitations on your company’s health insurance or do you think that the coverage offered will suffice in the event of a sudden illness? With a common misconception of a corporate coverage being adequate, here are 3 factors to consider when determining if your company’s health insurance is sufficient.

(See "An Introduction To International Health Plans")

#1 Portability

An important point for consideration is the portability of your health insurance. Will you be able to bring the plan along should you leave the company or relocate to another country? If your plan is not portable, you are likely to be subjected to underwriting should you choose to purchase new coverage. However, with it being harder to qualify for insurance when you get older, this puts you at risk of being uninsurable or having higher premiums and/or exclusions should you have any pre-existing health conditions.

(See "What Happens If I Don’t Have Long-term Care Insurance?")

#2 Lack of control

With corporate coverage, your health insurance is likely to be under a group policy. As it is meant to be a one size fit all solution for employees, you are unlikely to have any control over your coverage levels.

While basic coverage may be sufficient for an individual with no financial liabilities and/or dependents, things are likely to change when you start a family. With dependents financially reliant on you, you may wish to increase and/or adjust your coverage accordingly. To retain control over your health insurance, consider International Health insurance.

(See "Comparing Whole Life Insurance 2019")

Simple, high coverage, affordable. Insurance done right for your family.

#3 Subjected to limits and co-payment

Lastly, the amount that you can claim from your company’s health insurance is likely to have a capped limit. Co-payment may also be applicable which may result in you having to share a certain percentage of the incurred costs. You may also be unable to choose to visit your preferred doctor or clinic as additional excess may be applicable should you visit a non-panel clinic.

(See "All About Term Insurance 2019")

Why International Health plans?

Offering the option for worldwide medical coverage, International Health insurance is portable and customisable thus giving you full control over your policy.

With International Health insurance, your plan can be brought along to any country that you may move to next thus resolving the problem of portability. This not only eliminates the inconvenience of having to re-apply and undergo medical underwriting again but also ensures that you will remain insured regardless of any health deteriorations.

Additionally, international health plans can be customised according to your desired coverage levels and annual coverage limits. This ensures that you will be adequately covered in the event of an emergency.

(See "3 Reasons An International Health Plan Is For You")

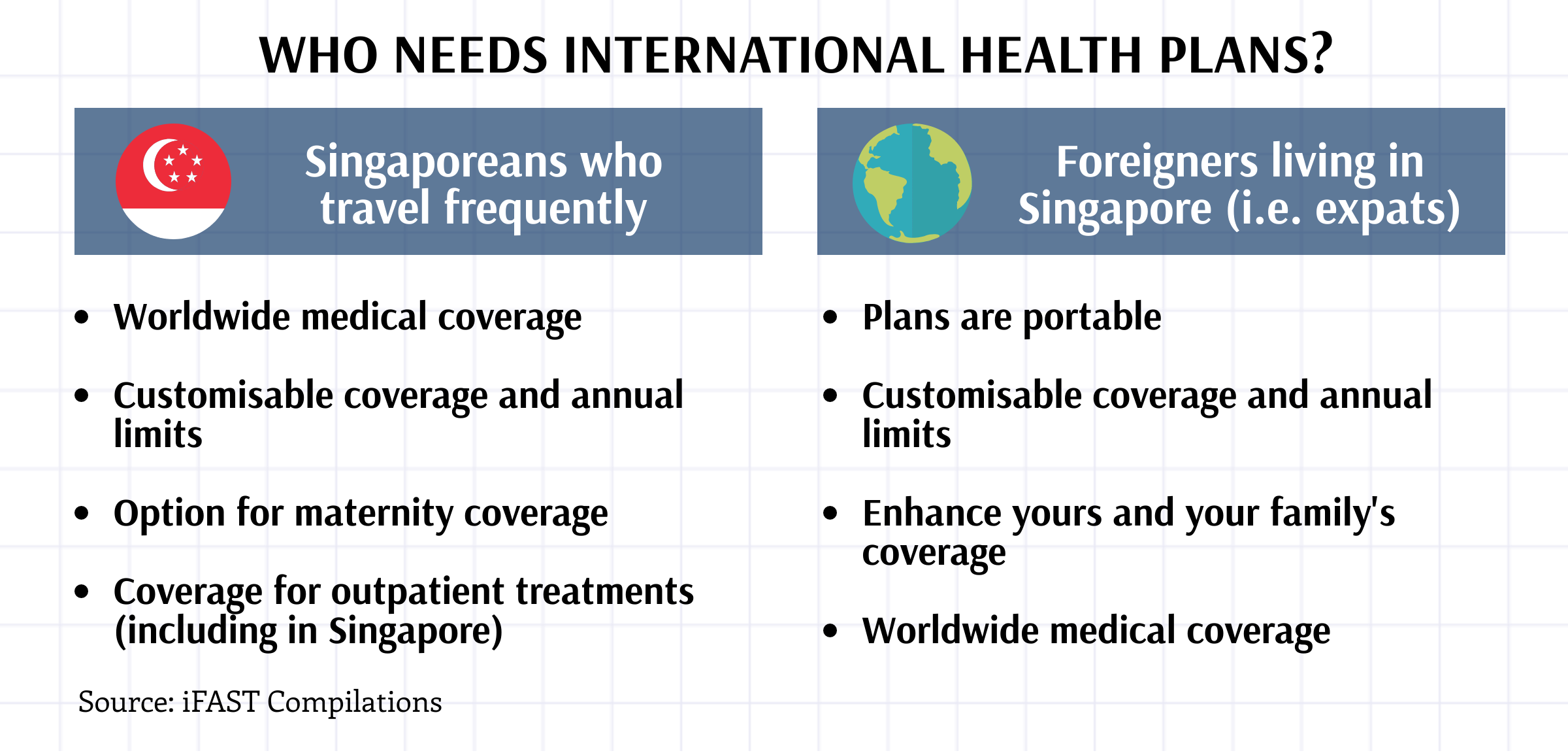

International Health insurance is suitable for:

International Health insurance is not suitable for:

*Exclusive Promotion: Enjoy 26% off your FWD International Health (IH) plan with promo code "IFAST". Purchase can be made on FWD's website.

Over 6,900 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Note: Information is accurate as of 26 May 2020 with changes subjected to the insurer's discretion.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment from Etiqa Insurance, Manulife, NTUC Income and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Best Travel Insurance For Families 2019

I Already Have CPF Life, Do I Still Need Annuities?