New 37 standard critical illness (CI) as defined by Life Insurance Association (LIA)

With the new CI definitions effective no later than 26 August 2020, we highlight the critical illnesses affected by these changes. To find out more about the changes, you may wish to refer to our article "Should You Purchase Critical Illness Insurance Before 2020?"

37 Standard critical illnesses as defined by LIA |

|||

Major cancer |

Open chest heart valve surgery |

Fulminant hepatitis |

Major head trauma |

Heart attack of specified severity |

Irreversible loss of speech |

Motor neurone disease |

Paralysis (irreversible loss of use of limbs) |

Stroke with permanent neurological deficit |

Major burns |

Primary pulmonary hypertension |

Terminal illness |

Coronary artery by-pass surgery |

Major organ or bone marrow transplantation |

HIV due to blood transfusion and occupationally acquired HIV |

Progressive scleroderma |

End stage kidney failure |

Multiple sclerosis |

Benign brain tumour |

Persistent vegetative state (apallic syndrome) |

Irrevsible aplastic anaemia |

Muscular dystrophy |

Severe encephalitis |

Systemic lupus erythematosus with lupus nephritis |

End stage lung disease |

Idiopathic parkinson's disease |

Severe bacterial meningitis |

Other serious coronary artery disease |

End stage liver failure |

Open chest surgery to aorta |

Angioplasty and other invasive treatment for coronary artery |

Poliomyelitis |

Coma |

Alzheimer's disease or severe dementia |

Blindness (irreversible loss of sight) |

Loss of independent existence |

Deafness (irreversible loss of hearing) |

|||

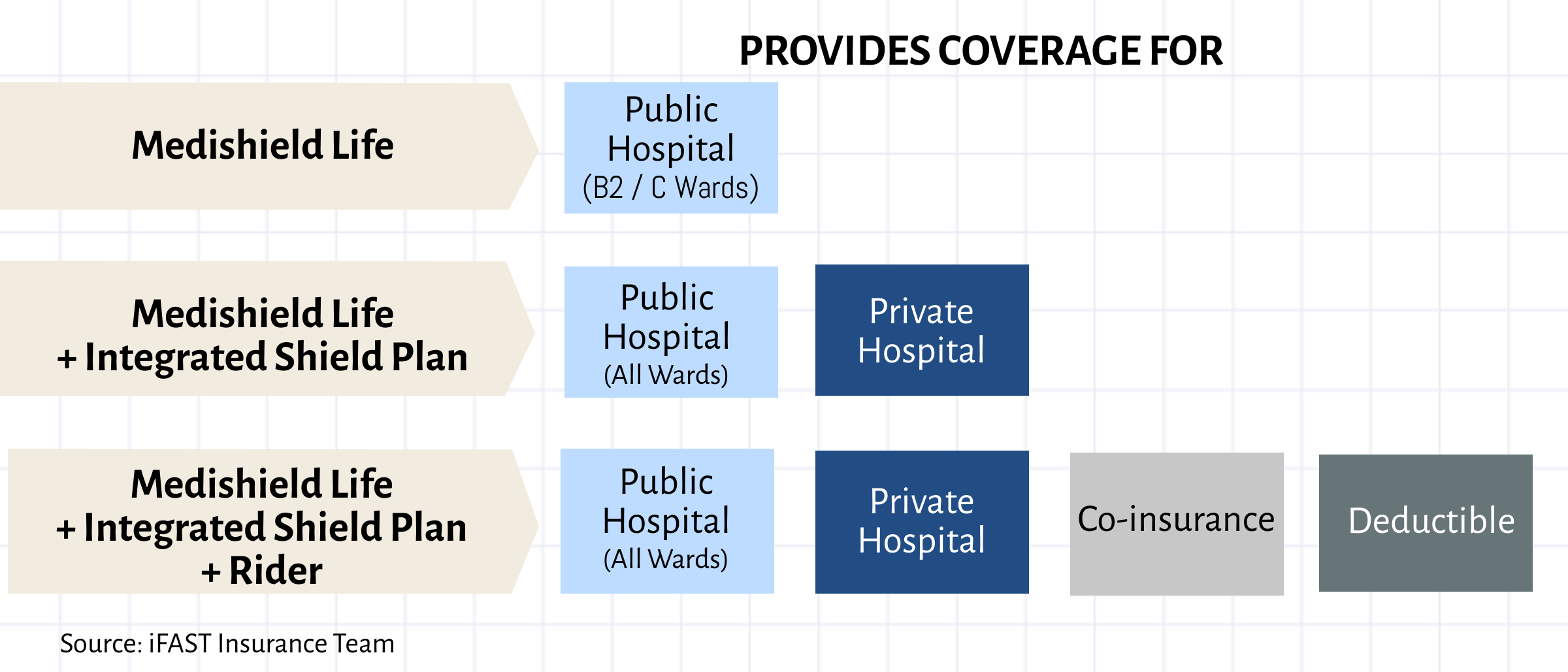

#1 Integrated shield plans provides health coverage

Covering for inpatient, day surgeries, pre and post treatments and specified outpatient treatments, MediShield Life offers all Singaporeans and Permanent Residents (PRs) health coverage for Class B2/C wards in public hospitals. To cover for treatments in private hospitals and/or Class A wards in public hospitals, an integrated shield plan and shield rider can be purchased.

If you are concerned about the medical expenses incurred from a critical illness, you may be relieved to know that integrated shield plans offers coverage should you require inpatient treatment. Additionally, most integrated shield plans would cover for specified outpatient treatments with the non-exhaustive list shown in the table below.

Non-exhaustive list of outpatient treatments covered by integrated shield plans: |

||

Kidney dialysis |

Radiotherapy |

Chemotherapy |

Immunotherapy |

Stereotactic radiotherapy |

Immunosuppressants for organ transplant |

Erythropoietin |

||

Therefore while we acknowledge that critical illness and integrated shield plans are not to be used interchangeably, we feel that priority should be given to getting comprehensive coverage for your hospital plans. If you are still concerned about coverage for critical illnesses, you may then wish to consider early critical illness or cancer insurance.

(See "3 Things You Must Know About Integrated Shield Plans")

Simple, high coverage, affordable. Insurance done right for your family.

#2 Basic critical illness insurance only covers for 37 advanced stage CIs

Medical advancements have resulted in critical illnesses being detected at an earlier stage. However, as basic critical illness plans only provides coverage for the 37 advanced stage CI as defined by LIA, an individual would not be able to make any claims in the event of early or intermediate stage critical illness diagnosis. Therefore if you are worried about being diagnosed with critical illnesses, a basic critical illness insurance would be insufficient coverage.

As explained in our article "Do You Really Need Early Critical Illness Insurance?", early critical illness (ECI) insurance offers a more comprehensive coverage for critical illnesses. With coverage for up to 119 medical conditions for early to advanced stage critical illnesses, ECI plans have no restrictions on how your pay-outs are to be used. As such, ECI plans are typically used for income replacement during your recovery period.

(See "Critical Illness Insurance In A Nutshell?")

#3 Cancer as the affordable option for coverage against the number 1 critical illness

The number one critical illness, approximately 35 people are diagnosed with cancer every day.1 If you wish to receive some coverage but do not have the budget for an early critical illness insurance, consider cancer insurance.

Early critical illness insurance |

Cancer insurance |

|

Coverage |

$200,000 |

$200,000 |

Policy term |

To age 85 |

To age 85 |

Annual premiums |

$2,248 |

$248 |

*Note: Premiums are calculated before discounts and calculated for a 30 year old non-smoker male with changes subjected to the insurer's discretion. Policies may have a fixed death benefit with this benefit differing between policies.

With some cancer insurance offering full pay-out for all stages of cancer, this provides assurance knowing that you are covered from the start. Additionally, cancer insurance is also suitable for individuals with pre-existing medical conditions as cancer insurance does not require any underwriting. With just 1 medical question to be answered, this allows you to purchase cancer insurance as long as you have no history of cancer.

Exclusive promotion: Enjoy 35% off your FWD Cancer Insurance with promo code "IFAST".You may purchase FWD's Cancer Insurance here.

(See "Best Cancer Insurance Singapore")

In summary,

Basic critical illness (CI) insurance |

Integrated shield plan |

Early critical illness (ECI) insurance |

Cancer insurance |

|

Coverage |

Typically covers for the 37 standard critical illnesses as defined by LIA |

Inpatient, day surgeries, pre and post treatments and specified outpatient treatments |

Up to 119 medical conditions including early and intermediate stages of critical illnesses |

All stages of cancer |

Underwriting required? |

Yes |

Yes |

Yes |

No, just answer 1 health question |

Payment for claims |

Lump sum pay-out |

Reimbursement basis |

Lump sum pay-out |

Lump sum pay-out |

*NEW* March birthday promotion. Enquire here to find out more.

Over 6,900 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Information is accurate as of 23 March 2020 with changes subjected to the insurer's discretion.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment from Etiqa Insurance, Manulife, NTUC Income and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Best Personal Accident Insurance Singapore 2020

Is Your MINDEF Group Insurance Really The Cheapest?

When Is Whole Life Insurance The Better Option?

Does My Travel Insurance Cover The Wuhan Coronavirus (COVID-19)?