A life insurance that is meant to be used for your protection gap during your working years, term insurance offers an affordable option for life insurance.

However, while term insurance is indeed an affordable option for life insurance, thinking that term plans are always cheaper or better could prove to be a costly mistake. In this article, we highlight four mistakes that you may be making with your term insurance.

(See "Stay Safe This Dengue Season With These 3 Tips")

Mistake #1 Thinking that term insurance is always cheaper

While term plans are commonly believed to be the more affordable option, there are some exceptions to this case.

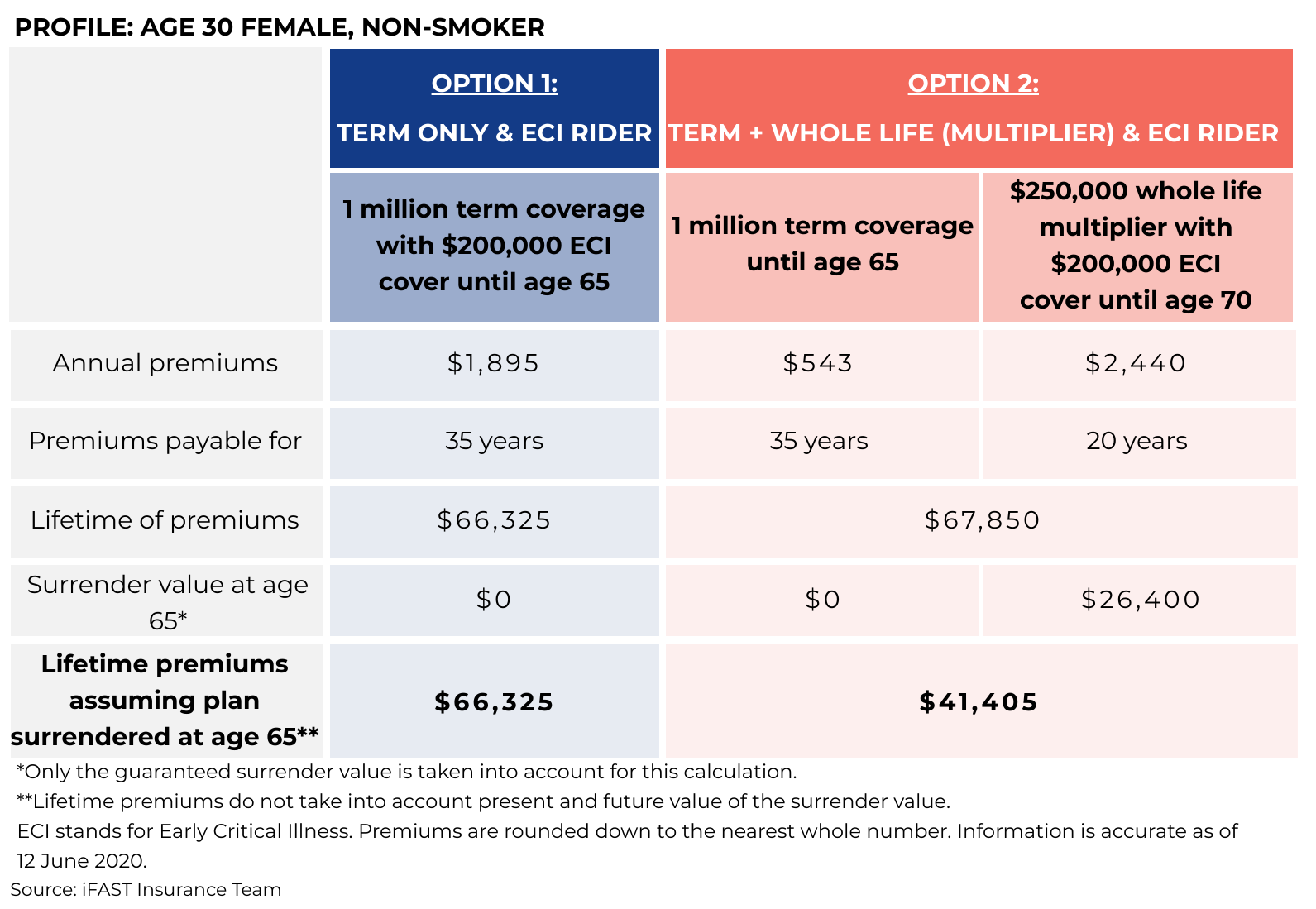

Take for example the two options as shown in the table above. As whole life insurance accumulates cash value, you would be able to receive a guaranteed surrender value of $26,400 should you choose to surrender your whole life plan at age 65. Assuming that we only require coverage until age 65 and intend to surrender our plan then, this would bring our lifetime premiums for option 2 to a total of $41,405 as compared to $66,325 from option 1.

The insured may also choose to not surrender his/her plan for option 2 with the difference in lifetime premiums only slightly higher for option 2 as compared to option 1. Keeping his/her whole life insurance coverage would then allow him/her to continue enjoying a $50,000 life coverage, inclusive of $40,000 early critical illness coverage, for the rest of his/her life without having to pay any additional premiums.

Do note that the above options do not take into account present and future values of the surrender value. Instead, this comparison has been simplified to show the total capital required for lifetime premiums for the two options.

(See "3 Reasons To Not Get Basic Critical Illness Insurance")

Mistake #2 Believing that term insurance will always offer better coverage

There is a common misconception that term insurance will always offer better coverage levels. However, while term insurance is an affordable option for life insurance, term plans may not always offer better coverage levels.

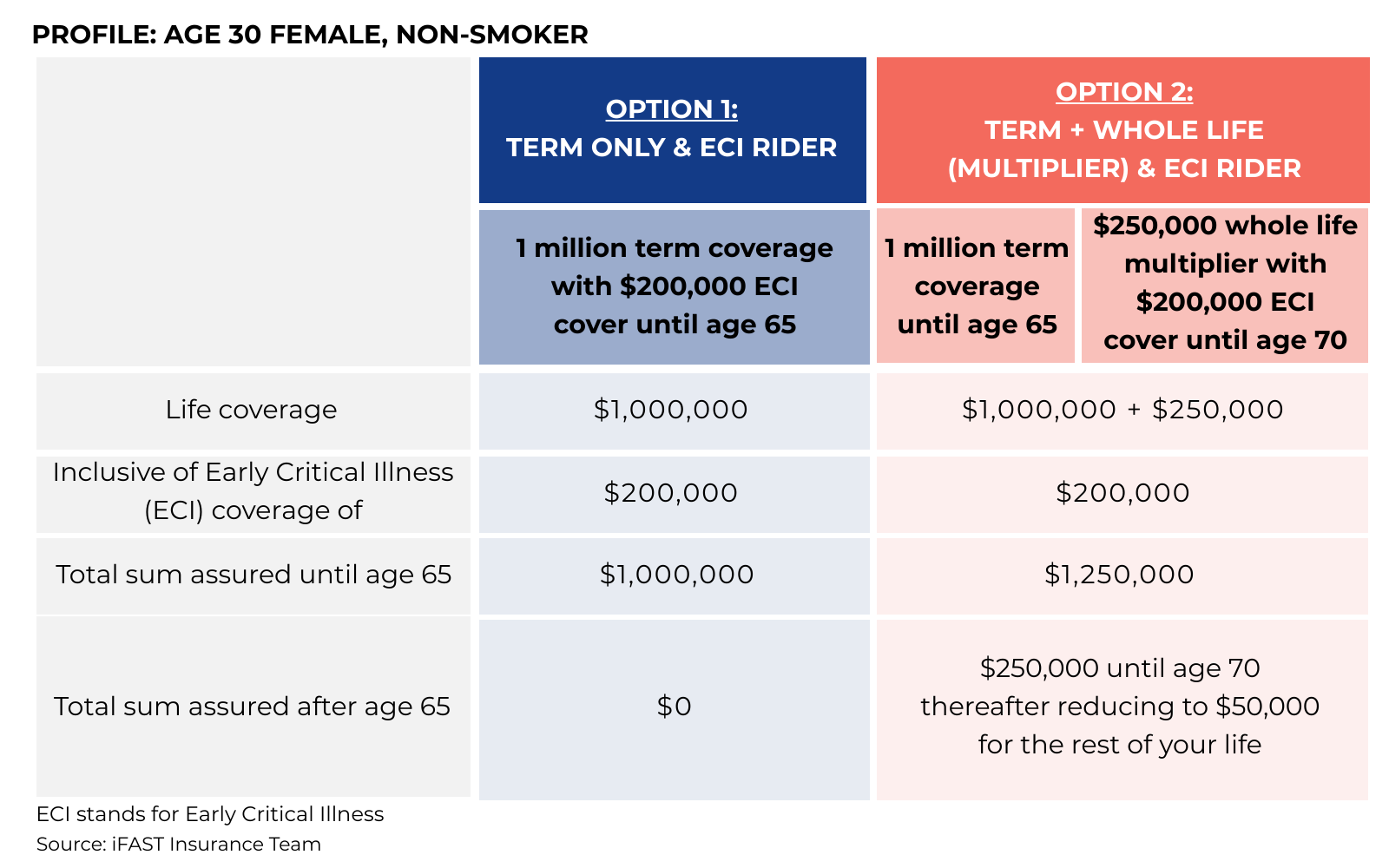

Continuing on the comparison of option 1 and 2, we can see that option 2 will provide slightly more coverage with a higher sum assured of $1,250,000 until age 65 as compared to option 1.

After age 65, the term insurance plan will cease coverage and the total sum assured for option 1 will reduce to $0. However, as option 2 also includes a whole life insurance plan, the total sum assured for option 2 will not be reduced to $0. Instead, option 2 will continue to enjoy a total sum assured of $250,000 until age 70, thereafter reducing to $50,000 for the rest of your life.

Option 2 will also continue to include $40,000 early critical illness (ECI) coverage after age 70 for the rest of your life. Therefore while term plans are affordable, they may not always be the better coverage option.

(See "When Is Whole Life Insurance The Better Option?")

Simple, high coverage, affordable. Insurance done right for your family.

Mistake #3: Using term insurance for coverage in retirement

Term insurance provides coverage for a specified period and is typically used to address a temporary protection gap. Without the need to protect your dependents or a loss of income in retirement, income protection is of less importance with the focus for protection needs shifting back to yourself. This would make coverage from term insurance less relevant when you retire.

(See "Is Your MINDEF Group Insurance Really The Cheapest?")

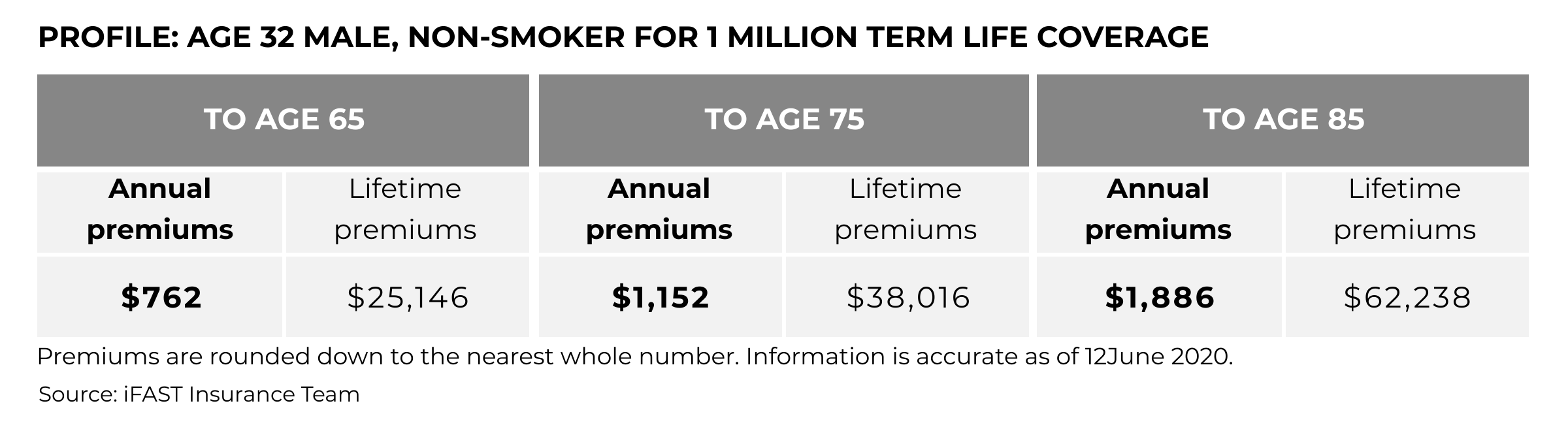

Mistake #4: Choosing term insurance for coverage until age 85

Additionally, using term insurance for coverage until age 85 would also lead to significantly higher annual premiums as compared to coverage until age 65.

Moreover, with no limited pay option for term insurance plans, you would have to continue paying annual premiums for every year of coverage that you enjoy. This may lead to a cash flow problem where you would be retired and without income but yet still have to pay the annual premiums for your term insurance.

(See "Want An Early Retirement? Achieve Your Retirement Goals With Annuities")

Term insurance may be suitable for:

Term insurance may not be suitable for:

Over 6,900 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Chubb, Etiqa Insurance, FWD Insurance, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

The 3 Things All Business Owners Should Know About Insurance

Is My Company's Insurance Benefit Really Reliable?