What are endowments?

Endowments, also known as a saving plan, are a type of life insurance. Offering minimal coverage, endowments are seen as a disciplined way to save and are typically used to help achieve financial goals rather than for just insurance coverage.

How does an endowment work?

In endowments, individuals are required to pay a fixed amount for a specified period of time. This may be a one-off payment or a regular payment for 5 to 25 years. Endowment plans are thus able to help us to build up our savings over a specified time frame.

As a saving plan, endowments will accumulate cash values. How this works is that the insurer will use a portion of your premiums for insurance coverage and invest the rest of your premiums paid. Based on the performance of their investments, this then forms the basis of your non-guaranteed returns. Plans that participate in the insurer's investments (also known as participating fund) are called a participating plan.

(See The Truth About Endowments")

What will I get from an endowment?

With cash values accumulating over the span of your policy term, plans will either provide a lump sum pay-out at maturity of policy (i.e. at the end of the policy term) or a regular pay-out throughout the policy period.

Endowments also come with surrender values. This means that you have the option to surrender your policy in exchange for a sum of money should you urgently require cash.

(See Understanding the difference between ILPs and Endowments")

Endowments are typically used for two main purposes: to receive a regular pay-out or to save up for a financial goal. In this article, we look at nine different policies and highlight the benefits of using an endowment plan.

For regular pay-outs: NTUC Income Gro Cash Flex and Gro Sure Saver, Manulife Spring, Ready Life Income II, Signature Income

One benefit of using endowments are the regular pay-outs that you may be able to receive from the plan.

How this works is that endowment plans that offer pay-outs usually come with an accumulation period which ranges between 2 to 10 policy years. Regular pay-outs will then be given on a regular basis for a specified duration (e.g. 10 years or up to the age of 120) after this accumulation period. Individuals may also choose to accumulate their pay-outs with the insurer for additional interest so as to receive a larger sum at policy maturity.

If you would like to an endowment plan that provides regular pay-outs, you may wish to consider these plans:

Name of plan |

Gro Cash Flex |

Gro Sure Saver |

Manulife Spring II |

Ready Life Income II |

Signature Income |

Insurer |

NTUC Income |

NTUC Income |

Manulife |

Manulife |

Manulife |

Premium Payment Term |

5, 10, 15, 20, 25, 30 years |

15 to 25 years |

12 years |

5 or 10 years |

Single Premium |

Policy Term |

10, 15, 20, 25, 30 years or up till age 120ALB |

15 to 25 years (policy must mature no later than age 69 ALB of insured) |

12 years |

Up to age 120 |

Up to age 120 |

Pay-outs start from |

From end of 2nd policy year |

From end of 2nd policy year |

From end of 3rd or 6th year onwards |

From end of policy year 5 or 10 |

From 37th or 49th policy month |

Frequency of pay-outs |

Yearly |

Yearly |

Yearly |

Yearly |

Monthly |

Guaranteed acceptance |

Yes |

N.A. |

Yes |

Yes |

Yes |

Capital guaranteed at maturity? |

Yes (if cash pay-outs are accumulated with insurer) |

No |

Yes |

N.A. |

80% guaranteed surrender value from day 1 |

Option to accumulate cash pay-outs with insurer for interest? |

Yes |

Yes |

Yes |

Yes |

Yes |

Payment method |

Cash (SGD) |

Cash (SGD) |

Cash (SGD) |

Cash (SGD) |

Cash (SGD or USD) |

Coverage |

Death and Terminal Illness (TI) |

Death, Terminal Illness (TI), and Total Permanent Disability (TPD, before age 70) |

Death, Terminal Illness (TI), Total Permanent Disability (TPD) |

Death and Terminal Illness (TI) |

Death and Terminal Illness (TI) |

Tell me more about saving plans

For short-term financial goals (e.g. 10 years and under): NTUC Income Gro Saver Flex, Gro Power Saver, and Gro Cash Flex

Another main purpose of using endowment plans are to help individuals to save towards a financial goal. If you are looking to use an endowment plan to help achieve your short-term financial goals, here are the plans that may be suitable for you:

NTUC Income's Gro Saver flex, Gro Power Saver, and Gro Cash Flex allows individuals to choose a policy term of just 10 years. This means that after 10 years your policy will mature and you will then be able to receive the maturity benefit from your endowment plan. If you are looking to save towards a short-term financial goal, these three plans may be suitable for you.

Name of plan |

Gro Saver Flex |

Gro Power Saver |

Gro Cash Flex |

Insurer |

NTUC Income |

NTUC Income |

NTUC Income |

Premium Payment Term |

Single premium or for 5, 10, 15, or 20 years |

3 years |

5, 10, 15, 20, 25, 30 years |

Policy Term |

10, 15, 20, 25, 30 years or up till age 120 |

10 years |

10, 15, 20, 25, 30 years or up till age 120 ALB |

Pay-outs start from |

N.A. |

N.A. |

From end of 2nd policy year |

Frequency of pay-outs |

N.A. |

N.A. |

Yearly |

Guaranteed acceptance |

Yes |

Yes |

Yes |

Capital guaranteed at maturity? |

Yes |

No |

Yes (if cash pay-outs are accumulated with insurer) |

Option to accumulate cash pay-outs with insurer for interest? |

N.A. |

N.A. |

Yes |

Payment method |

Cash (SGD) or SRS (SRS for Single Premium only) |

Cash (SGD) |

Cash (SGD) |

Coverage |

Death and Terminal Illness (TI) |

Death and Terminal Illness (TI) |

Death and Terminal Illness (TI) |

For plans that are capital guaranteed at maturity: NTUC Income Gro Cash Flex, Gro Saver Flex and Manulife Spring II, GrowSecure

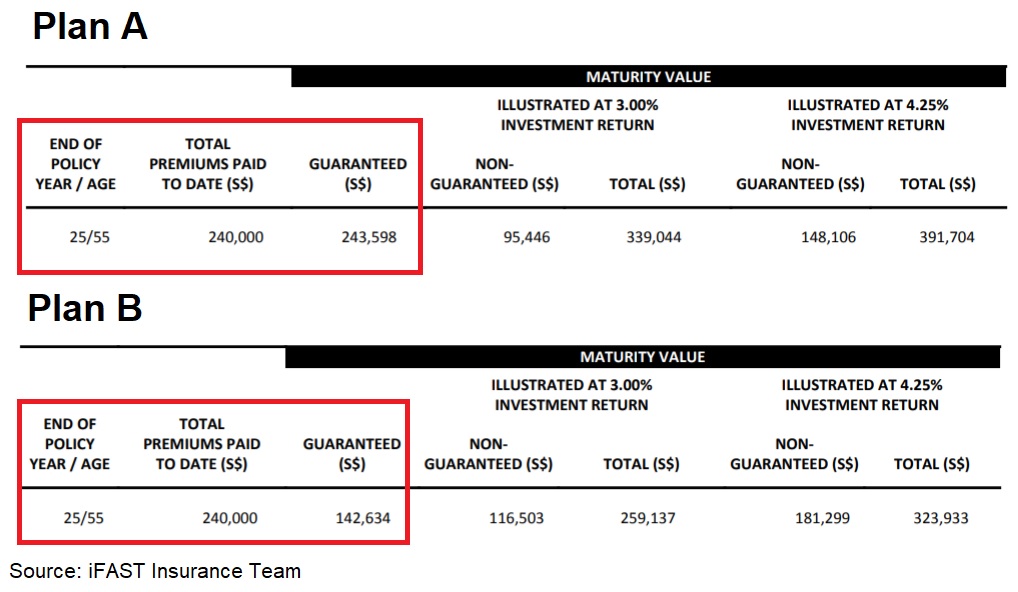

In endowment plans, the cash value of a plan is usually split into two components: guaranteed and non-guaranteed. This means that your final receivable amount will be made up of both a guaranteed and non-guaranteed component. It is important to note that while the amount stated in the guaranteed component is confirmed, the amount stated in the non-guaranteed component is based on illustrated returns. This means that the actual amount you receive from the non-guaranteed component may differ from the illustrated amount.

Therefore, another factor to consider when purchasing an endowment is to understand if your plan is capital guaranteed at maturity. A capital guaranteed at maturity plan refers to a plan where you are able to get back all your premiums paid (i.e. “total premiums paid to date”) under the guaranteed component at the maturity of policy. Note that the “total premiums paid to date” excludes any premiums paid for optional riders. Any policy alterations or claims made during the policy term may also affect your maturity value.

In the image below, we can see that Plan A has a guaranteed amount that is higher than the total premiums paid to date. This means that Plan A is plan that is capital guaranteed at maturity. On the other hand, Plan B has a lower guaranteed amount at maturity than the total premiums paid to date. This means that Plan B is not capital guaranteed at maturity.

For an endowment plan that is capital guaranteed, consider these plans:

Name of plan |

Gro Cash Flex |

Gro Saver Flex |

Manulife Spring II |

Grow Secure |

Insurer |

NTUC Income |

NTUC Income |

Manulife |

Manulife |

Premium Payment Term |

5, 10, 15, 20, 25, 30 years |

Single premium or for 5, 10, 15, or 20 years |

12 years |

5, 8, or 10 years |

Policy Term |

10, 15, 20, 25, 30 years or up till age 120 ALB |

10, 15, 20, 25, 30 years or up till age 120 ALB |

12 years |

16 or 18 years |

Pay-outs start from |

From end of 2nd policy year |

N.A. |

From end of 3rd or 6th year onwards |

N.A. |

Frequency of pay-outs |

Yearly |

N.A. |

Yearly |

N.A. |

Guaranteed acceptance |

Yes |

Yes |

Yes |

|

Capital guaranteed at maturity? |

Yes (if cash pay-outs are accumulated with insurer) |

Yes |

Yes |

Yes |

Option to accumulate cash pay-outs with insurer for interest? |

Yes |

N.A. |

Yes |

N.A. |

Payment method |

Cash (SGD) |

Cash (SGD) or SRS (SRS for Single Premium only) |

Cash (SGD) |

Cash (SGD) |

Coverage |

Death and Terminal Illness (TI) |

Death and Terminal Illness (TI) |

Death, Terminal Illness (TI), Total Permanent Disability (TPD) |

Death, Terminal Illness, Accidental death (before age 80) |

For alternative payment options: NTUC Income Gro Saver Flex, Manulife Ready Builder II (Single premium plans only), and Manulife Signature Income

If you would like to use your Supplementary Retirement Scheme (SRS) for payment, consider NTUC Income’s Gro Saver Flex and Manulife Ready Builder II. Apart from offering the usual cash payment in SGD, these two plans also offer the option to use your SRS for payment. However, do note that SRS payments are only applicable for single premium plans (i.e. this must be a one-off premium made at the start of the policy term).

Alternatively, Manulife's Signature Income accepts payment with USD should you wish to pay for your endowment with a currency other than SGD.

Name of plan |

Gro Saver Flex |

Ready Builder II |

Signature Income |

Insurer |

NTUC Income |

Manulife |

Manulife |

Premium Payment Term |

Single premium or for 5, 10, 15, or 20 years |

Single premium or 5, 10, 15, 20 years |

Single Premium |

Policy Term |

10, 15, 20, 25, 30 years or up till age 120 |

Up to age 120 |

Up to age 120 |

Pay-outs start from |

N.A. |

N.A. |

From 37th or 49th policy month |

Frequency of pay-outs |

N.A. |

N.A. |

Monthly |

Guaranteed acceptance |

Yes |

Yes |

Yes |

Capital guaranteed at maturity? |

Yes |

80% guaranteed surrender value from day 1 for Single Premiums policies |

80% guaranteed surrender value from day 1 |

Option to accumulate cash pay-outs with insurer for interest? |

N.A. |

N.A. |

Yes |

Payment method |

Cash (SGD) or SRS (SRS for Single Premium only) |

Cash (SGD) or SRS (SRS for Single Premium only) |

Cash (SGD or USD) |

Coverage |

Death and Terminal Illness (TI) |

Death and Terminal Illness (TI) |

Death and Terminal Illness (TI) |

If you are interested in getting an endowment plan, or would like a second opinion to find out which endowment can best suit your financial goals, contact us for a complimentary session here!

Let FSMOne help you get on track with your financial planning

Information accurate as of 21 February 2022. Changes to policies are subjected to the insurer's discretion.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

All about insurance for newly wedded couples

Are annuities good for retirement planning?

Should I switch from Eldershield to CareShield Life?

This is why you should Buy Term Invest the Rest (BTIR)

Debunking Cancer Insurance Myths – Here Are 4 Things You Must Know