As of 1 October 2020, all Singaporeans and Permanent Residents (PRs), who were born in 1980 or later, will be automatically enrolled into CareShield Life when they reach age 30. However, if you fall into the group of Singaporeans and PRs with an ElderShield, or were born in 1979 or earlier, you may have several questions regarding CareShield Life and whether it is worth switching over from ElderShield. If you are unsure as to which is the better option for you, then this article is for you.

What is ElderShield?

ElderShield 300 was introduced in 2002 as a basic long-term care insurance for all Singaporeans and Permanent Residents (PRs). This was subsequently reviewed in 2007 with ElderShield 400 launched to provide higher monthly disability pay-outs for a longer period.

(See "Critical illness coverage on a budget for age 40 and above")

What is CareShield Life?

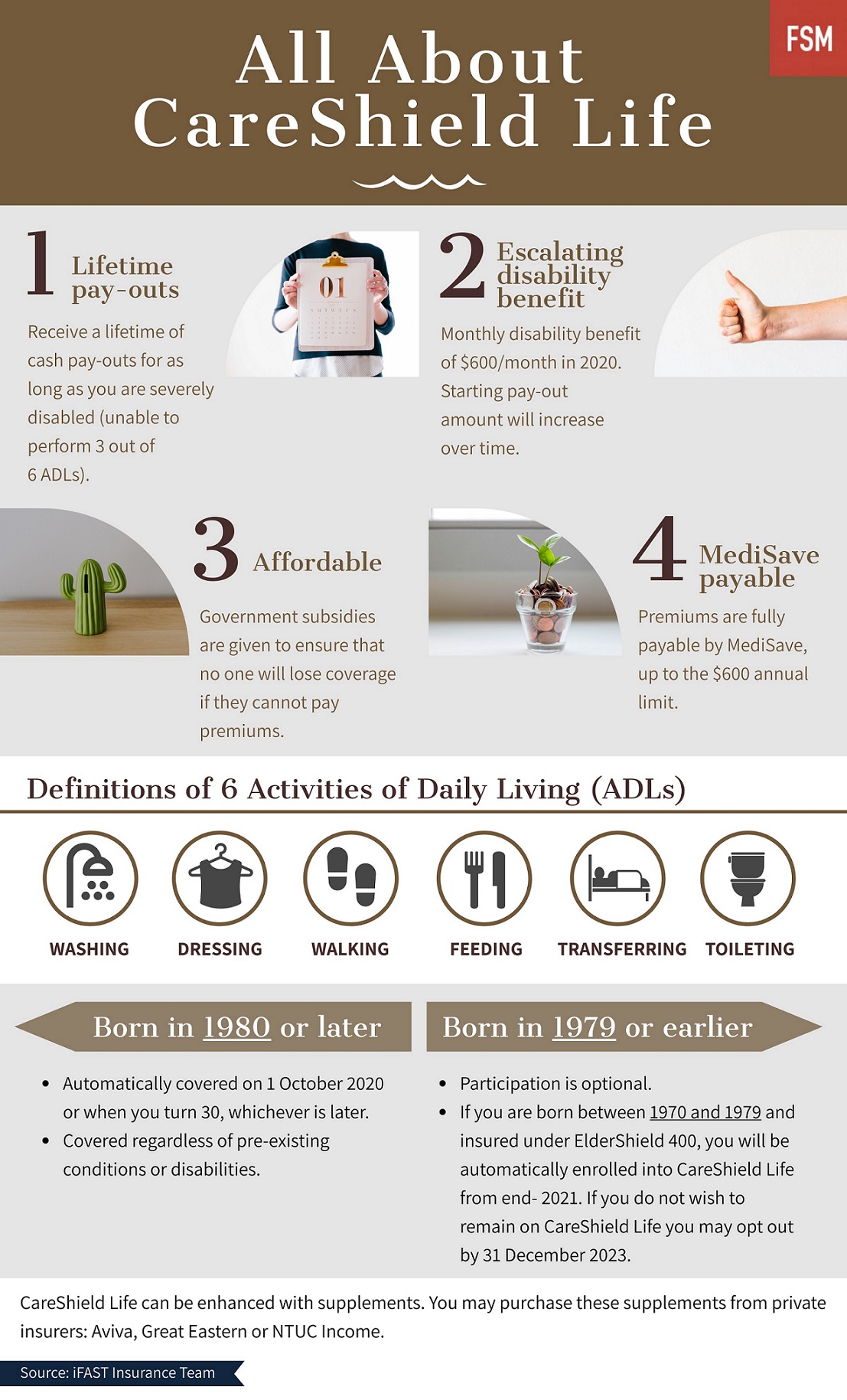

A compulsory national insurance scheme, CareShield Life is an enhancement to existing ElderShield plans. This is a type of long-term care insurance and seeks to provide basic financial support for all Singaporeans in the event of a severely disability.

Enrolment into CareShield Life is compulsory for all Singaporeans and Permanent Residents (PRs) who were born in 1980 or later. Singaporeans and PRs born in 1979 or earlier will have the option to switch to CareShield Life in 2021.

(See "Our honest opinions about CareShield Life and its supplements")

Comparing ElderShield and CareShield Life

There are three main differences between ElderShield and CareShield Life, namely the monthly disability benefit, duration of pay-outs and eligibility for coverage.

ElderShield (乐龄健保) |

CareShield Life (终身护保) |

|

Entry age |

Age 40 |

Age 30 |

Administered by |

Private insurers: Aviva, Great Eastern or NTUC Income. |

Singapore government |

Monthly disability benefit |

300 or $400, dependent on plan chosen |

Starting pay-out of $600 in 2020 |

Escalating monthly disability benefit |

No |

Yes. Monthly disability benefit will increase at a projected rate of 2% p.a. until the age of 67.1

However, should an individual make a claim before age 67, his/her monthly disability benefit will be fixed at the year of claim. |

Duration of pay-outs |

For up to 60 or 72 months, dependent on plan chosen |

For life |

Premiums |

Fixed. Premiums are determined at the age of entry and does not increase with age. |

Premiums will increase over time. |

Premium payment term |

Age 40 to 65 |

Age 30 to 67 |

Premiums at entry age* |

ElderShield 300

Male: $151.67 Female: $194.26 ElderShield 400 Male: $174.96 Female: $217.76 |

CareShield Life

Male: $175 Female: $218 |

Option to opt out? |

Yes |

No |

Eligibility for coverage |

Excludes individuals with pre-existing disabilities |

Includes individuals with pre-existing disabilities |

*Premiums are shown for standard entry age. Information accurate as of 25 November 2020.

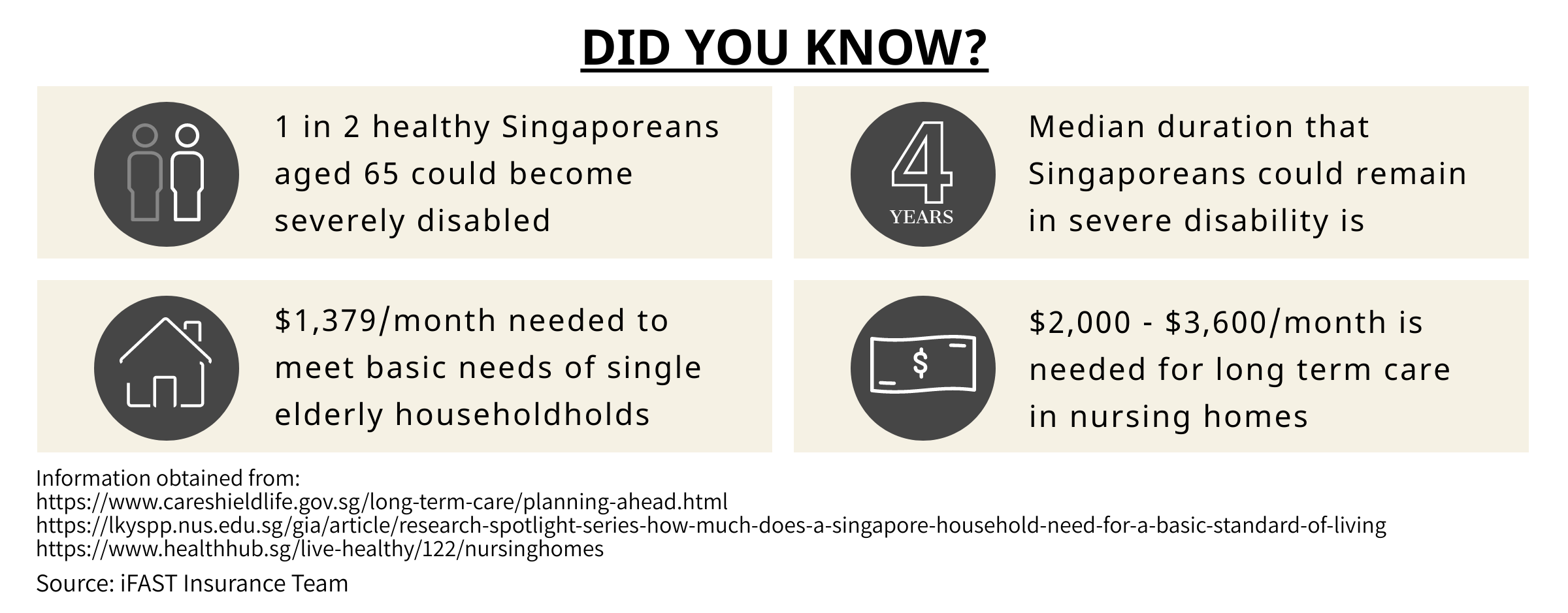

CareShield Life offers a higher starting monthly disability benefit with this set to be $600 in 2020. This is higher than the $300 or $400 monthly benefit given by ElderShield. Additionally, the starting monthly disability benefit from CareShield Life is projected to increase at a rate of 2% p.a. until the age of 67. This allows you to receive a higher starting pay-out benefit should you become severely disabled at a later age.

^Monthly disability benefit is calculated on a projected 2% p.a. increase and is rounded down to the nearest decimal place.

CareShield Life also offers enhanced coverage with the monthly disability benefit given for life. This is an improvement from ElderShield where the disability benefit is only given for up to 60 or 72 months.

Lastly, CareShield Life covers all Singapore citizens and Permanent Residents (PRs), including those with pre-existing severe disabilities. Individuals who would have been uninsurable under ElderShield due to pre-existing severe disabilities will now be able to receive coverage under CareShield Life.2

(See "Is Your Term Insurance A Costly Mistake?")

Should you switch your existing ElderShield plan to CareShield Life?

If you are unsure as to whether CareShield Life is the better option for you, here are a few scenarios to consider.

#1 Are you unable to upgrade your existing ElderShield coverage?

If you had tried to upgrade your existing ElderShield coverage but was unable to do so due to pre-existing medical conditions, consider switching to CareShield Life. This would allow you to receive enhanced coverage of a higher starting monthly disability pay-out and a lifetime of disability pay-outs in the event of a severe disability.

If you are currently on ElderShield, a switch to CareShield Life is only possible if you are not already severely disabled.

Our recommendation: Yes, switch to CareShield Life

(See "3 Reasons To Not Get Basic Critical Illness Insurance")

#2 Do you only have basic coverage without any ElderShield supplements?

If you are on the basic ElderShield scheme with no supplements, you may benefit from the increased coverage of CareShield Life. This is because CareShield Life offers a higher monthly disability benefit with this fixed at $600 in 2020 as compared to the $300 or $400 a month from ElderShield. CareShield Life also provides the monthly disability benefit for life thus ensuring that you would be able to receive coverage for as long as you remain severely disabled.

However, do note that the premiums for CareShield Life are different. While there will be subsidies for first five years of premiums (2020 to 2025), the amount for future premiums are still undetermined.

ElderShield 300 |

ElderShield 400 |

CareShield Life |

|

Premiums at entry age |

Male: $151.67

Female: $194.26 |

Male: $174.96

Female: $217.76 |

Male: $175

Female: $218 |

Our recommendation: Yes, switch to CareShield Life

(See "What Happens If I Don’t Have Long-term Care Insurance?")

#3 Do you have existing ElderShield supplements?

Do you have existing ElderShield supplements or other long-term care insurance that will pay a higher monthly disability benefit? If you do, then perhaps reconsider your switch to CareShield Life. This is because switching over may give you a monthly disability benefit that is lower than what you would get from your other policies.

Note that CareShield Life cannot be opted out of should you wish to cancel your policy in the future.

Our recommendation: Maybe. You may wish to consider factors such as premiums payable and duration of pay-outs given before deciding whether to stay or to switch.

(See "Am I Ready To Retire?")

#4 Have you opted out or been denied of entry to ElderShield?

With CareShield Life offering universal coverage, this means that you would be able to join CareShield Life now even if you have previously opted out of ElderShield or were above the maximum entry age for ElderShield in 2002. This is provided that you are not severely disabled at time of entry. Enrolment into CareShield Life will begin from end-2021.

Estimated CareShield Life premiums for those born in 1979 or earlier can be found here.

Our recommendation: Yes, consider enrolling into CareShield Life to enjoy the enhanced coverage benefits.

(See "Cheap Critical Illness Cover For Those In Their 30s")

Over 8,100 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Want An Early Retirement? Achieve Your Retirement Goals With Annuities

Best Personal Accident Insurance Singapore 2020

Is My Company's Insurance Benefit Really Reliable?

Best Motorcycle Insurance Singapore 2020

----

1Source: https://www.careshieldlife.gov.sg/careshield-life/benefits.html