What is CareShield Life?

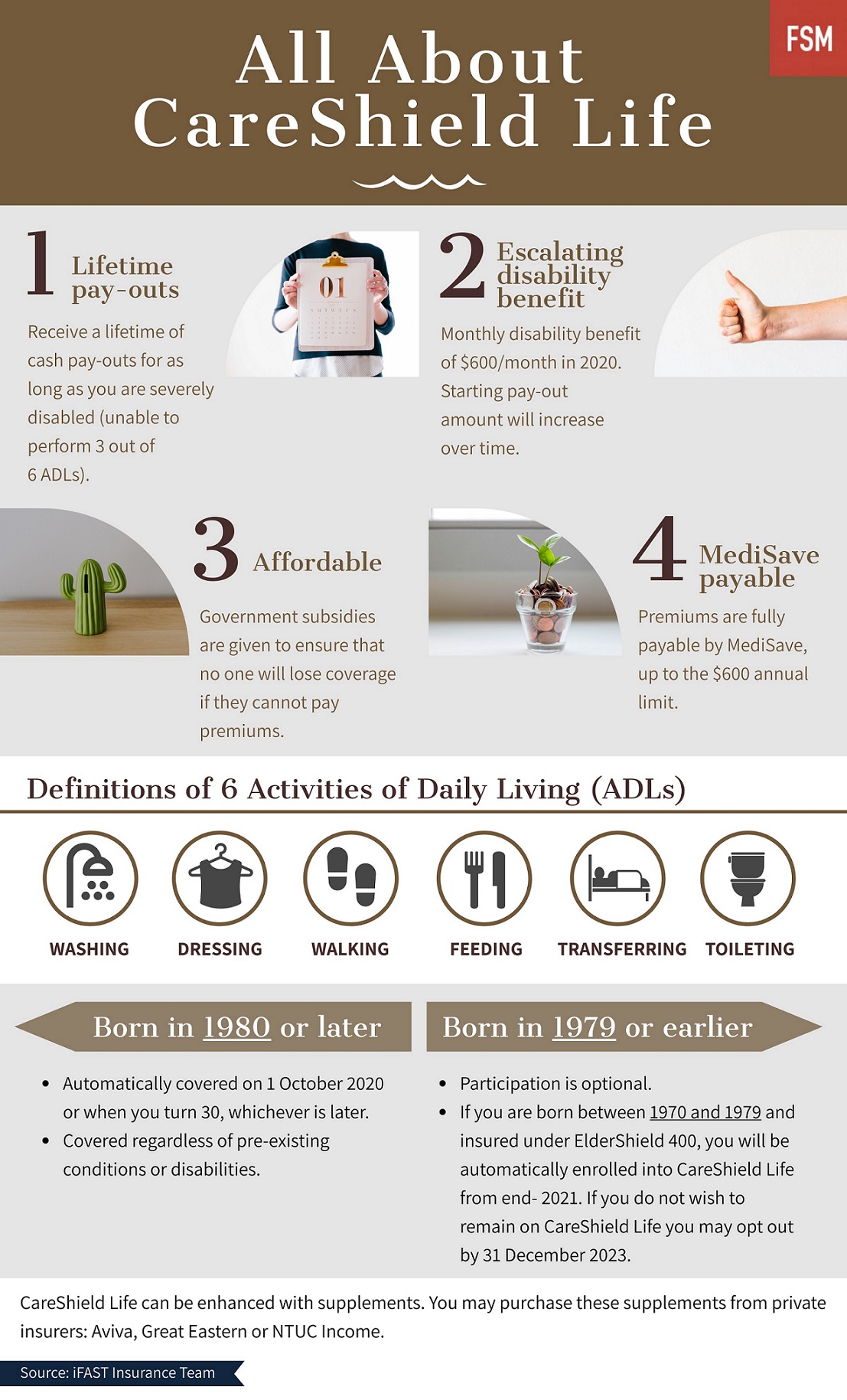

A form of disability insurance, CareShield Life provides basic financial support for all Singaporeans should they become severely disabled. This is defined as the inability to perform at least 3 out of 6 Activities of Daily Living (ADLs) with the six ADLs being washing, dressing, walking, feeding, transferring and toileting.

Starting from 1 October 2020, all Singaporeans and Permanent Residents (PRs) vwho were born in 1980 or later will be automatically enrolled into CareShield Life at the age of 30. If you are born in 1979 or earlier and wish to switch to CareShield Life, you may do so in 2021 if you are not severely disabled. Transitional subsidies are also available from 2020 to 2024 to help Singaporeans with the transition to CareShield Life.1

(See "Cheap Critical Illness Cover For Those In Their 30s")

What are the differences between ElderShield and CareShield Life?

ElderShield |

CareShield Life |

|

Entry age |

Age 40 |

Age 30 |

Administered by |

Private insurers: Aviva, Great Eastern or NTUC Income. |

Singapore government |

Monthly disability benefit |

300 or $400, dependent on plan chosen |

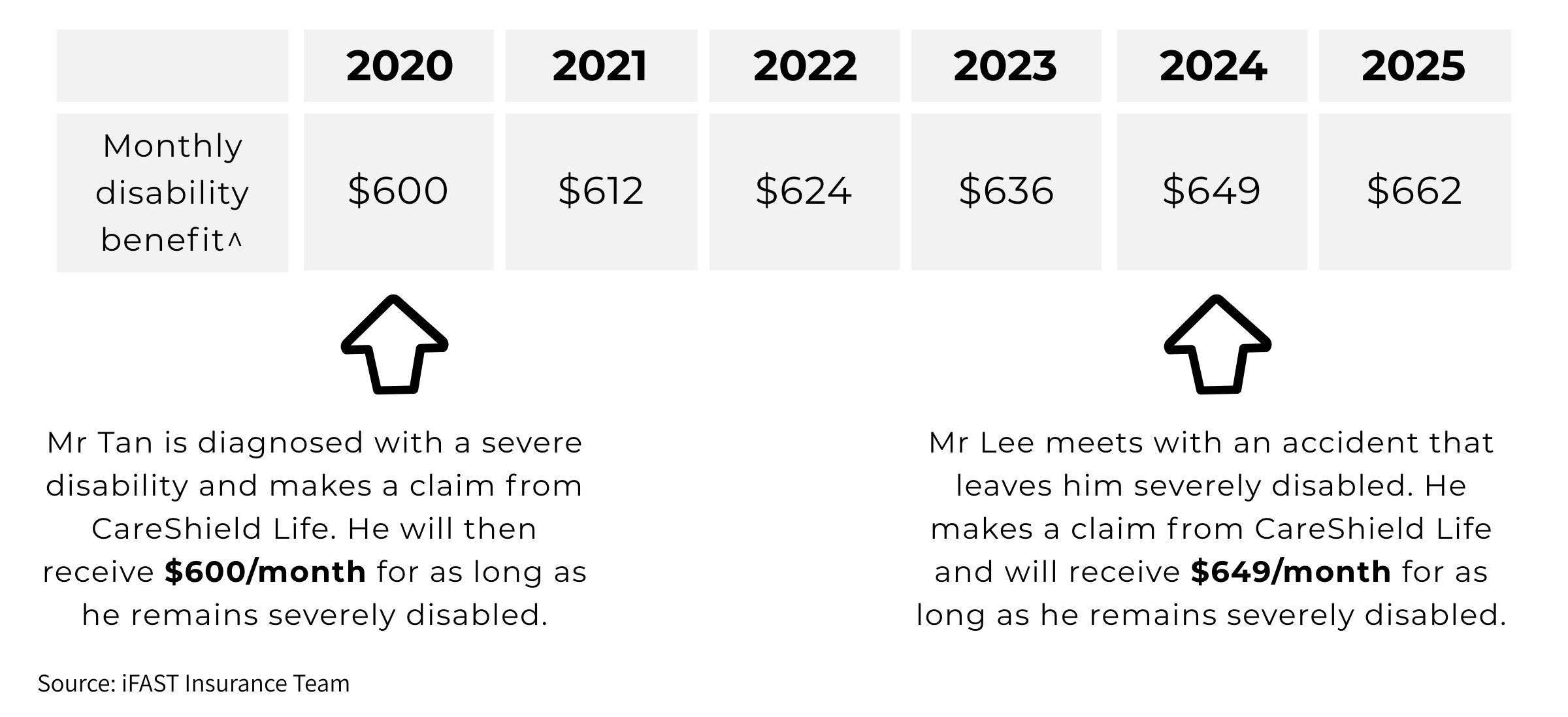

Starting pay-out of $600 in 2020 |

Escalating monthly disability benefit |

No |

Yes. Monthly disability benefit will increase at a projected rate of 2% p.a. until the age of 67.2

However, should an individual make a claim before age 67, his/her monthly disability benefit will be fixed at the year of claim. |

Duration of pay-outs |

For up to 60 or 72 months, dependent on plan chosen |

For life

|

Option to opt out? |

Yes |

No

|

One of the biggest difference between CareShield Life and ElderShield is the monthly disability benefit given in the event of a severe disability. While ElderShield only pays out for up to 60 or 72 months, CareShield Life will provide a monthly disability benefit for life. Pay-outs from CareShield Life is also higher with this starting at $600/month in 2020 and increasing over time.

^Monthly disability benefit is calculated on a projected 2% p.a. increase and is rounded down to the nearest decimal place.

However, unlike ElderShield which can be opted out of, CareShield Life is made compulsory for all Singaporeans born in 1980 or later. To aid in this transition, the premiums of CareShield Life will be subsidised for the first five years, between the years of 2020 to 2024.3

Lastly, a point to note is that while ElderShield used to be administered by private insurers, CareShield Life is now administered by the government.4

(See "Best Personal Accident Insurance Singapore 2020")

Simple, high coverage, affordable. Insurance done right.

Am I able to enhance my CareShield Life coverage?

CareShield Life can be enhanced with supplements purchased from private insurers. An example of a CareShield Life supplement is Care Secure from NTUC Income.

Care Secure by NTUC Income |

|

The good |

The bad |

While CareShield Life would require an individual to be severely disabled and be unable to perform 3 out of 6 ADLs, coverage for Care Secure will commence with just the inability to perform 2 out of 6 ADLs. This allows the individual to get covered at an earlier stage of disability. Additionally, Care Secure also provides a support benefit and dependent benefit to allow you to receive additional pay-outs when you need it the most.

Care Secure also offers higher monthly pay-outs with individuals able to choose to receive up to $5,000 monthly pay-outs. However, do note that pay-outs from Care Secure includes the pay-out receivable from CareShield Life. This means that if you choose to receive a monthly disability benefit of $1,800 from Care Secure, you would receive $600 from CareShield Life and $1,200 from NTUC Income's Care Secure.

If you are concerned about an earlier stage of disability and wish to receive pay-outs from the first or second ADL, you may consider enhancing your coverage with other long-term care insurance plans.

(See "What Happens If I Don’t Have Long-term Care Insurance?")

Are CareShield Life supplements necessary?

CareShield Life |

Care Secure (a CareShield Life supplement) |

|

Duration of pay-outs |

Lifetime cash pay-outs |

Lifetime cash pay-outs |

Condition for pay-outs to commence |

Severe disability, i.e. inability to perform 3 out of 6 ADLs |

Inability to perform 2 out of 6 ADLs |

Monthly pay-outs |

Starts at $600/month in 2020 and will increase annually until age 67 or when a claim is made, whichever is earlier |

Choice of monthly pay-out amounts, up to $5,000 |

Additional benefits |

- |

Support benefit, dependant benefit, and death benefit

|

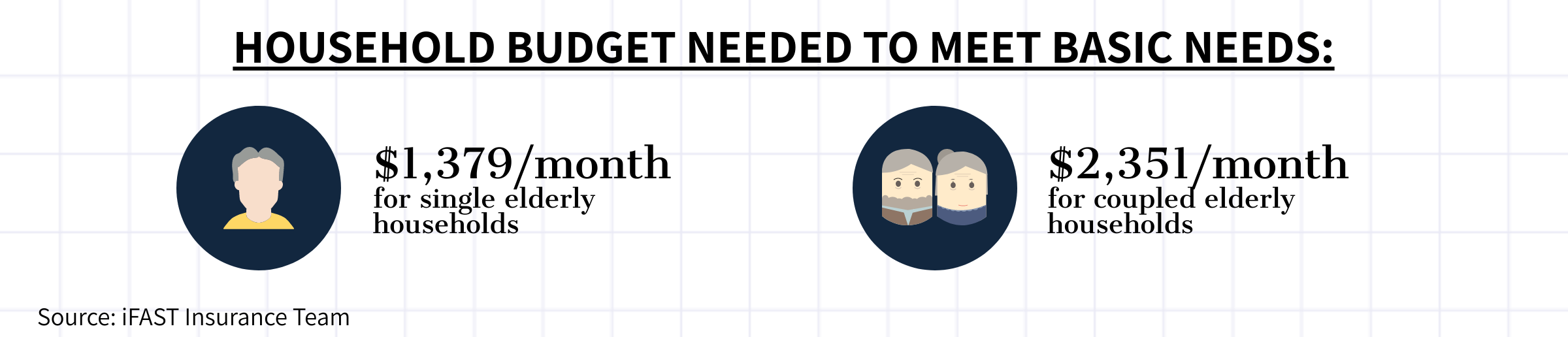

While CareShield Life offers a lifetime of cash pay-outs in the event of a severe disability, the starting pay-outs are set at just $600 in 2020. However, a study has found that Singaporeans aged 65 and above who are living alone would need at least $1,379 a month for basic needs.5 This results in a monthly shortfall of $779 should a senior, aged above 65, unfortunately becomes severely disabled. As such, we feel that supplements for CareShield Life and/or other long-term care insurance plans would be good to have if your budget allows for it.

(See "Should I switch from Eldershield to CareShield Life?")

Our recommendation

While CareShield Life supplements and/or other long-term care insurance plans will offer comprehensive coverage for long-term care, our take on this is that these supplements are a good to have but not a must have. This is because we feel that individuals should first consider their finances and determine their budget before purchasing any additional coverage. This will allows you to structure your insurance portfolio around what will best suit your coverage needs and ensures that you would not be overspending on insurance.

Here are a few questions to consider before committing to a CareShield Life supplement:

- Will my MediSave have enough to pay for a CareShield Life supplement on top of what I am already using it for? (E.g. CareShield Life, MediShield Life and Integrated Shield Plan premiums)

- If my dependents are not able to pay for their own premiums with MediSave, will my MediSave have enough to pay for their premiums too?

- If my MediSave is insufficient to pay for these premiums, will I be comfortable to use cash to top-up the balance required?

Consider getting a CareShield Life supplement and/or other long-term care plans if your answer to the above three questions is yes. However, if you feel that you would be stretching your finances by doing so then perhaps take time to reconsider and review your insurance portfolio.

Click on the button below to speak to our experts if you would like to find out how you should structure your insurance portfolio or want to find out more about CareShield Life.

Over 8,100 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

How Much Can I Receive From An Annuity?

Is Your Term Insurance A Costly Mistake?

Don’t Make These 3 Mistakes With Your Home Insurance

Best Critical Illness Insurance Singapore 2020

Is Your MINDEF Group Insurance Really The Cheapest?

----

2Source: https://www.careshieldlife.gov.sg/careshield-life/benefits.html