#1 Underinsuring the value of your home and its contents

Did you know that an insurer will prorate the amount payable if you are found to have underinsured the reinstatement or replacement value of your property and its contents?

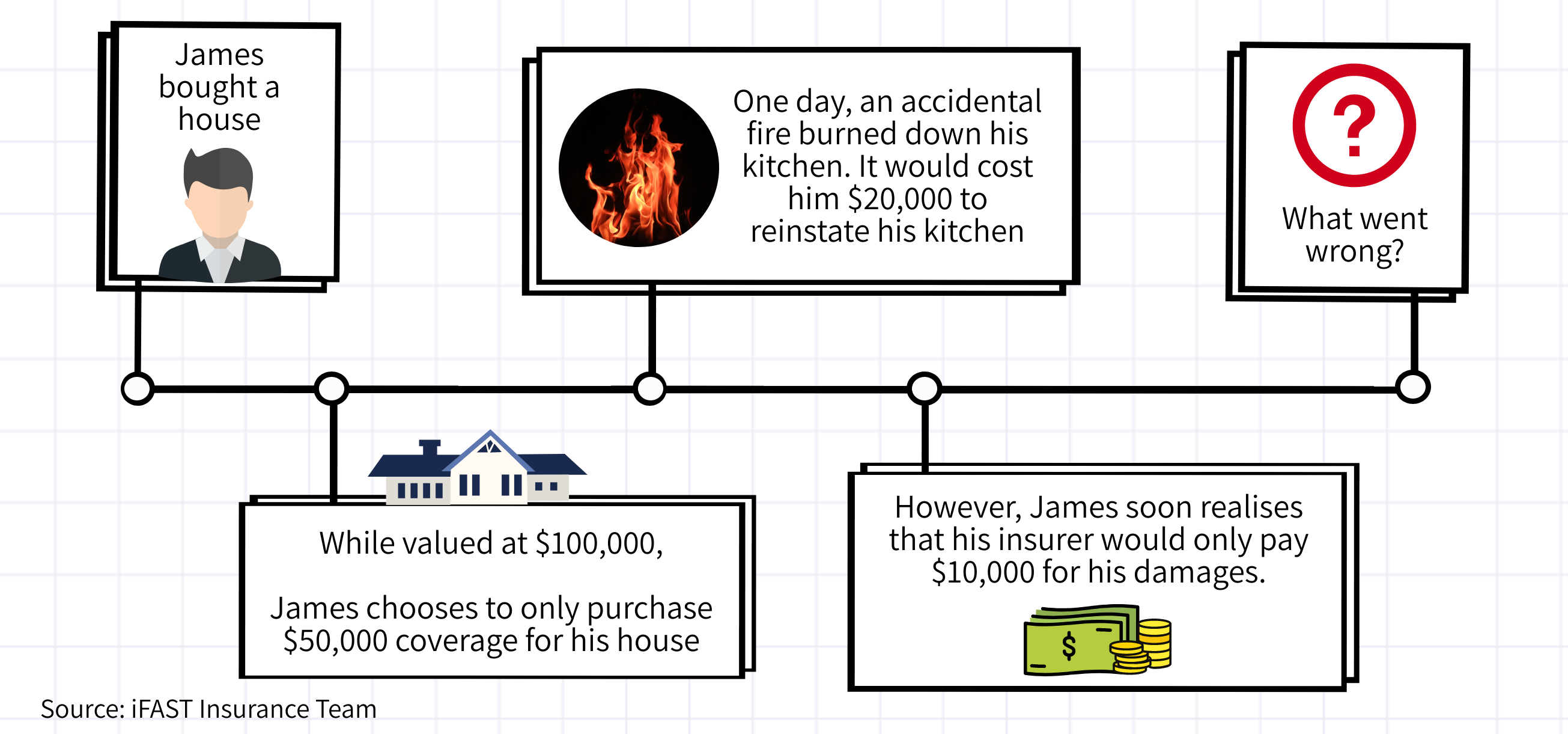

Take for example James, as shown in the image below, his property and its contents is valued at $100,000.

However, with only $50,000 coverage, he is under-insuring his property. Therefore, while the fire damage would require $20,000 to reinstate his kitchen, his insurer will only pay him $10,000 as he under-insured his property.

Under-insurance occurs when your coverage amount is less than the full reinstatement or replacement value for your building, renovations and contents. Should you underinsure your property, insurers will prorate the amount payable to you in the event of a loss or damage. You would then be unable to claim for the full cost to reinstatement or replace your premises.

Cost to reinstate or replace your premises |

Insurance coverage |

Status |

Amount claimable from insurer in the event of a $20,000 fire damage claim |

$100,000 |

$50,000 |

Underinsured by $50,000 |

Amount payable will be prorated. As you are only insured for 50% of the full reinstatement value, your insurer will only pay 50% of your claim amount, which in this instance will be $10,000. |

$100,000 |

$100,000 |

Adequately insured |

Insurer will pay $20,000. |

Home insurance is meant to offer reassurance with knowledge that you would not have to bear the cost to replace or reinstate your home in the event of a fire, theft or any other insured event. Therefore, it is imperative that you purchase insurance for the full reinstatement or replacement value of your home so as to ensure that your home will be adequately insured.

(See "Is Your Term Insurance A Costly Mistake?")

Simple, high coverage, affordable. Protect your loved ones from the uncertainties of life

#2 Confusing home content insurance with mortgage insurance

If you are using your CPF savings to pay for your housing loan instalment for your HDB, then you will have to be insured with Home Protection Scheme (HPS). A mortgage reducing insurance, HPS provides coverage for your mortgage loan against the event of a death, terminal illness or total permanent disability (TPD).

However, do not confuse having mortgage insurance as having home insurance. Mortgage insurance will only cover for mortgage loan with home insurance required should you wish to receive coverage for home content, renovations, building and fixtures.

(See "MRTA: The Difference Between Keeping or Losing A Home")

#3 Thinking that HDB’s fire insurance is sufficient

All HDB owners with outstanding HDB loans are required to purchase compulsory HDB fire insurance. However, did you know that fire insurance is a building insurance and would only cover the building structure and not its contents? This means that in the event of a fire, only the building structures, fixtures and fittings provided by HDB will be covered. Your renovations and all household content, such as built in cabinets, air-conditioning system and cooking hob, will not be covered under HDB fire insurance.

If you own a private property and/or took up a bank mortgage loan, you may also be required by your bank to take up a fire insurance policy. Also known as the Mortgagee Interest Policy (MIP), this is similar to the HDB fire insurance and will not provide coverage for your home content.

To receive coverage for your domestic appliances, built-in cabinets and other furniture, a home content insurance is required. Not only will this cover for the loss or damage to your home contents, but it will also allow you to receive alternative accommodation expenses in the event that you and your family cannot continue to live in your home due to the damages incurred. Coverage for your renovation can also be added-on to further enhance your coverage.

Exclusive Promotion: Enjoy 26% off your FWD Home Insurance with promo code "IFAST".

To summarise,

Mortgage insurance |

Fire insurance |

Home content insurance |

|

Provides coverage for |

Mortgage loan in the event of death, terminal illness or total permanent disability. |

Building structures, fixtures and fittings provided by HDB. |

Home content and renovations. Some plans may also cover for buildings and fixtures. |

In the event of a claim |

Lump sum pay out which can then be used to pay off any outstanding mortgage. |

Covers cost to restore the physical structure of property to its original state. |

Loss or damages to home content will be payable on a reimbursement basis up to the table of limits. |

Examples |

Home Protection Scheme (HPS) |

HDB fire insurance scheme or Mortgagee interest policy (MIP) |

Home content insurance is available on FSMOne from AIG, Etiqa, FWD, Great Eastern, MSIG, NTUC, QBE and Sompo |

Ongoing Promotions

AIG |

Etiqa |

FWD |

Great Eastern |

MSIG |

NTUC |

QBE |

Sompo |

Receive a $50 shopping voucher upon successful enrolment. Valid till 30 June 2021.T&Cs apply. |

- |

- |

20% off. Valid till 31 January 2021. T&Cs apply. |

- |

- |

- |

*Information accurate as of 13 January 2021.

Over 8,100 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Chubb, Etiqa Insurance, FWD Insurance, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Stay Safe This Dengue Season With These 3 Tips

Diabetes and Glaucoma – Will Your Insurance Cover This?