Term Insurance

Term insurance are a type of life insurance plan that covers for death and total permanent disability (TPD). Providing coverage for a fixed number of years, term plans are usually used to cover a temporary protection gap. This protection gap is generally found during your working years when you are drawing an income and have dependents who are financially reliant on you. As term plans tend to have lower premiums, they are often seen as the affordable way to get insurance coverage.

What does Buy Term Invest the Rest (BTIR) mean?

Buy Term Invest the Rest is the concept of buying a term insurance with the same coverage as whole life insurance and investing the difference in premiums. As term plans have a fixed duration as compared to whole life plans, it can provide similar coverage but at a lower cost. With a lower annual premium, this extra savings could be used for your investments instead.

Profile: Age 40, non-smoker male.

Term plans |

Whole Life plans |

|

Covers for |

Death and Total Permanent Disability (TPD) |

Death and Total Permanent Disability (TPD) |

Coverage amount |

$600,000 |

$600,000 until age 70, and $200,000 after age 70 |

Annual premiums |

$813.60 |

$6,301.32 |

Premiums payable for |

25 years |

20 years |

Coverage given for |

Up to age 65 |

Up to age 99 |

Information is accurate as of 12 January 2022.

Why should I Buy Term Invest the Rest (BTIR)?

Now that we understand what BTIR means, here are the three main benefits of choosing to use the BTIR model.

#1 Lower premiums

Term plans tend to offer more affordable premiums as compared to a whole life plan with the same coverage levels.

An Illustration: Comparison of premiums between a Term and Whole Life plan for an age 30, non-smoker male.

Product |

Sum Assured |

Premium Term |

Annual Premiums |

Term |

$600,000 |

35 years |

$531 |

Whole Life |

$600,000 until age 70, and $200,000 after age 70d |

20 years (coverage if given for up to age 99) |

$4,790.74 |

Information is accurate as of 12 January 2022.

As shown in the table above, a term life plan can give you the coverage you need at a more affordable price as compared to a whole life plan. By choosing a term insurance plan, this allows you to "save" the difference in premiums between a whole life and term plan. You will then be able to invest these savings following the BTIR model.

#2 Premiums saved can be invested or compounded in your CPF Special Account

The difference in premiums between a term and whole life plan is $4,259.74 for a 30 year old non-smoker male. If we were to put this into a CPF Special Account (SA) and left to compound at the CPF SA rate of 4 per cent per annum1, this is how much your premiums saved could potentially be worth.

Profile: Age 30, non-smoker male.

Age |

Yearly savings from difference in premiums |

Interest rate for CPF SA account |

Total value of savings without compounding |

Total value of savings after compounding |

30 |

$4,259.74 |

4% |

$4,259.74 |

$4,430.13 |

35 |

$4,259.74 |

4% |

$25,558.44 |

$29,384.94 |

40 |

$4,259.74 |

4% |

$46,857.14 |

$59,746.28 |

45 |

$4,259.74 |

4% |

$68,155.84 |

$96,685.50 |

50 |

$4,259.74 |

4% |

$89,454.54 |

$141,627.71 |

55 |

$4,259.74 |

4% |

$110,753.24 |

$196,306.77 |

60 |

$4,259.74 |

4% |

$132,051.94 |

$262,832.21 |

65 |

$4,259.74 |

4% |

$153,350.64 |

$343,770.59 |

*Total savings do not take into account present and future values.

Alternatively, you may also choose to invest your premiums saved into other investments of your choice for potentially higher returns.

#3 Control over your investments

As explained in our previous article "Understanding the difference between ILPs and Endowments", ILPs and Endowments offer individuals the option to save and accumulate cash values through these insurance or savings plan. However, one downside to doing so is that individuals have less control over their choice of investment products that they are investing into.

With the Buy Term Invest the Rest (BTIR) model, we recommend individuals to get a term insurance and invest the premiums saved instead. This allows you full control over your investments, giving you the freedom to choose investment options that have a lower management fee or lower administrative cost.

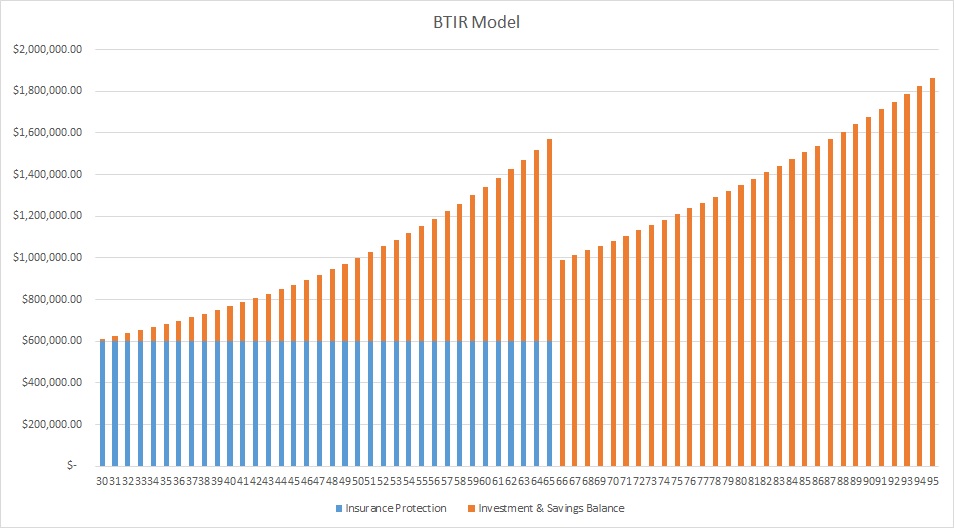

An illustration of how Buy Term Invest the Rest (BTIR) works

Mr Tan, a 30 year old male with $600,000 term policy coverage chooses to use the BTIR model. The chart below shows what were to happen if he were to save $1,000 a month and use these savings for an investment with a 4 per cent growth rate.

Figures are for illustrative purposes and the actual premiums and sum assured may differ for individuals. All investments comes with risk, no investments are a guaranteed win.

Upon maturity of the policy at age 65, assuming he no longer has any outstanding mortgage or loans to service, his savings and investment earnings could potentially be enough to cover his expenses for the remainder of his life. This is assuming that he requires a monthly expense of $1,338.2 With no dependents financially reliant on him at this stage, it would not be necessary for Mr Tan to continue with the term policy.

Do take note that this suggested course of action is for illustrative purposes only and does not take into account a person’s pre-existing health conditions and financial situations. If you would like to find out more, do consult an adviser or seek professional advice before taking any action.

Let FSMOne help with your insurance planning

Live better, safer. Get a complimentary review today!

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Is CPF Life enough for me to retire?

Debunking Cancer Insurance Myths – Here Are 4 Things You Must Know

My agent sold me an ILP. Should I keep it?

Your Cheatsheet To Insurance Terms

Have a question about Covid-19 travel insurance?

----

Source 1: https://www.cpf.gov.sg/member/growing-your-savings/earning-higher-returns/earning-attractive-interest

Source 2: https://www.numbeo.com/cost-of-living/in/Singapore