The purpose of insurance

A means of protection against financial loss, having insurance ensures that you or your dependents will be financially able in the event that you meet with any mishap. Therefore as a child does not have any dependents who are financially reliant on them, he/she might not actually need to have much insurance.

Prioritising insurance for a child

Rather than to purchase a plethora of policies for your child, instead consider what are your intentions behind doing so. This will allow you to prioritise your insurance purchases for your child.

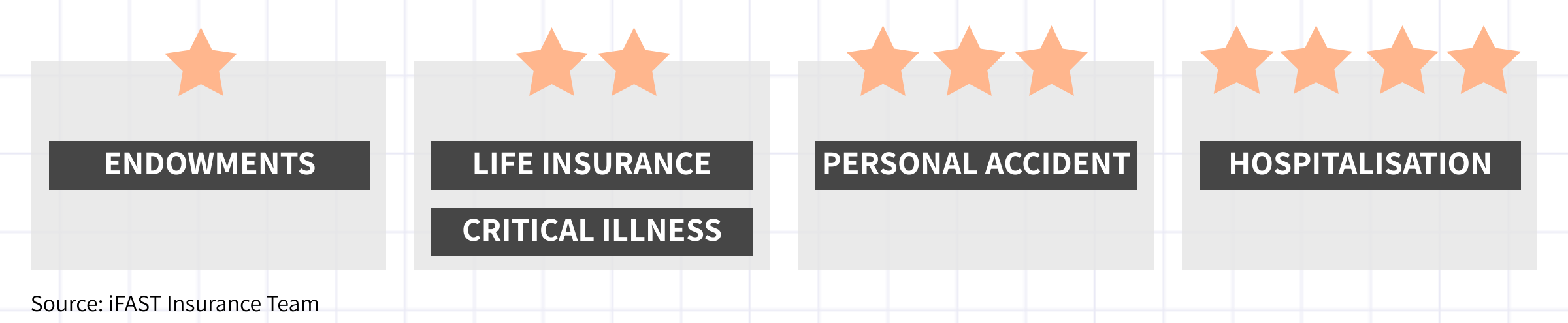

In this article, we break down insurance for a child into four categories and elaborate on which insurance you should prioritise for your child.

(See "Cheap Critical Illness Cover For Those In Their 30s")

#1 Hospitalisation insurance

If you can only afford one insurance plan for your child, we strongly recommend purchasing hospitalisation insurance. Here are our reasons why.

Ensuring insurability

Insurers will impose exclusions or load the insured with premiums should he/she be diagnosed with a medical condition. Getting a hospitalisation plan for your child at an early age prevents this by ensuring that he/she will be fully covered should they unfortunately be diagnosed with any illness or medical conditions in future.

Financial safety net

Additionally, as young children may be more prone to injuries, getting comprehensive hospitalisation insurance for your child also acts as a financial safety net for you. This allows you to let your child receive the appropriate treatment without having to worry about the cost involved.

While all Singaporeans and Permanent Residents (PRs) will receive basic hospitalisation insurance via MediShield Life, we recommend enhancing this coverage for your child. This can be done with the addition of an integrated shield plan and a rider. For more information on integrated shield plans, you may refer to our article "Are Integrated Shield Plans Necessary?".

Estimated cost: $776/year

MediShield Life |

Integrated shield plan (Enhanced Incomeshield Preferred)* |

Integrated shield plan rider (Income's Preferred Deluxe Care Rider)* |

|

Yearly premiums for Age 1 to 18 |

$130 |

$205 |

$441 |

*Premiums are calculated for the most comprehensive plan and are accurate as of 25 November 2020.

(See "Our honest opinions about CareShield Life and its supplements")

Protect my child

#2 Personal accident

Personal accident (PA) insurance provides coverage for accidents (e.g. falls, sprains or other accidental injuries) and infectious diseases (e.g. dengue fever, HFMD, covid-19 etc.) and are typically used to complement existing life or hospitalisation plans. While PA plans are not alternatives to life or health plans, they are capable of providing coverage at affordable costs.

Take for example Hand Foot and Mouth Disease (HFMD). A highly contagious disease, children attending childcare or day care centres may be exposed to a higher risk with the recovery period taking up to a week or more. With outpatient treatment not covered by MediShield Life, your child’s treatment costs would then have to borne by you. In such a scenario, having a personal accident plan would allow you to submit a claim for compensation if your plan includes coverage for specified infectious diseases.

As young children are more prone to accidents and illnesses, we recommend parents to get personal accident insurance for their child. Alternatively, some PA plans also offer free child cover if the parents purchase personal accident plans for themselves.

Estimated cost: $90 to $200/year (after discounts)

Sompo PA Junior Teddy |

FWD Personal Accident |

Income PA Assurance Plan 1 |

TM PA Plan A |

MSIG Protection Plus Silver |

Manulife Ready Protect Accelerate |

|

Coverage amount for child |

$30,000 |

$100,000 |

$100,000 |

$20,000 |

$10,000 |

$50,000 |

Infectious disease cover |

Yes |

Yes |

Optional add-on |

No |

No |

Yes |

Yearly premiums^ |

$185 |

$120 |

$198 |

Free child cover if you and/or your spouse applies for a personal accident insurance together with your child. |

Free child cover if you and/or your spouse applies for a personal accident insurance together with your child. |

$96 |

Ongoing promotions |

25% off when you use code "IFAST". |

30% off until 30 November 2020. |

^Premiums shown are before discounts and are for the basic plans offered. Accurate as of 25 November 2020.

(See "Best Personal Accident Insurance Singapore 2020")

#3 Life insurance or critical illness insurance

With no dependents financially reliant on your child, a life insurance is a not a necessity. However, parents may still choose to buy life insurance to lock in the insurability of your child. This ensures that the child will have coverage even if he/she is diagnosed with any medical conditions in future.

As life insurance is a gift of insurability to your child, this is a good-to-have and not a must-have. Therefore, consider purchasing this only if you are comfortable with the premiums required.

Estimated cost: $300 to $1,200/year

Name of plan |

TM Term Assure 2 |

Manulife LifeReady Plus |

TM Term Assure 2 |

Manulife LifeReady Plus |

Type of plan |

Term plan with critical illness rider |

Whole life plan with multiplier |

Term plan with early critical illness rider |

Whole life plan with multiplier and early critical illness rider |

Coverage |

$200,000 to age 65 |

$200,000 until age 70 and $50,000 for rest of life or until age 99 |

$200,000 to age 65 |

$200,000 until age 70 and $50,000 for rest of life or until age 99 |

Premiums payable for |

Until age 65 |

20 years |

Until age 65 |

20 years |

Yearly premiums |

$304.80 |

$683.99 |

$552.80 |

$1,255.66 |

Lifetime of premiums required |

$19,812 |

$13,679.80 |

$35,932 |

$25,113.20 |

Premiums shown are accurate as of 25 November 2020.

(See "Is Your Term Insurance A Costly Mistake?")

#4 Endowments or savings plan

Seen as a disciplined way to save, endowments are also known as a savings plan. Offering minimal protection, endowments should not be seen as insurance for protection. Instead, parents should only consider endowments if they would like to use endowments to save for their child’s education.

Offered on a regular premium or single premium basis, endowments accumulates cash values with a lump sum payable to the policy holder at maturity. By choosing to coincide your endowment’s maturity with when you will need the money, this ensures that you will have enough by the time your child is ready to enter tertiary education. This protects your child’s future by ensuring that he/she will not be denied of an education as a result of financial constraints.

However, while endowments are a good-to-have, we believe that this is not a must-have for your child. As such, we rank this as the least important type of insurance to purchase for your child.

Estimated cost: The actual cost of an endowment plan would differ between individuals and plans as this is based on how much you would like to receive at plan maturity.

(See "The Truth About Endowments")

Over 8,100 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Should I switch from Eldershield to CareShield Life?

Critical illness coverage on a budget for age 40 and above

How Much Can I Receive From An Annuity?