In our previous article "Choosing the right critical illness insurance. Part 1", we elaborated on some of the ways you can get critical illness coverage from standalone plans. In this article, we continue from where we left off and highlight an alternative: an add-on critical illness coverage to existing plans.

Would you prefer to add-on coverage to an existing cover?

Apart from standalone plans for coverage, individuals can also opt for add-on coverage. This comes in the form of a critical illness (CI) rider or early critical illness (CI) rider and can be added onto other basic plans to enhance coverage. These CI and ECI riders can be added-on to term and whole life plans.

With the addition of an early critical illness (ECI) rider to a base plan, this will allow your base plan to also cover for critical illnesses. The coverage period of the ECI rider will follow the policy term of the main plan.

Addition of ECI rider to your term insurance

While term plans are generally used for protection purposes, the addition of an early critical illness (ECI) rider to a term plan will allow your policy to also cover for critical illnesses.

The critical illness coverage for ECI riders are similar to those of a standalone single pay-out critical illness plan with pay outs staggered according to the different stages of critical illnesses. A cap is also placed on the maximum amount payable at each stage of critical illness.

Type of coverage |

Add-on early critical illness (ECI) rider to a term plan

|

Features |

The addition of an early critical illness (ECI) rider to a term plan will allow your policy to cover for critical illness. The coverage period of this ECI rider will follow the policy term of the main plan (your term insurance). |

Pay-outs |

Pay-outs for critical illness are staggered and paid in stages of early, intermediate and advanced stage critical illness. |

Pros |

Doubles up as both a protection and critical illness plan.

Premiums start low if purchased at a younger entry age. |

Cons |

Coverage is only given for as long as the policy owner is paying for the premiums. This means that you have to pay for your plan for as long as it is in force. E.g. you would still be paying for your insurance premiums at age 70 should you wish to receive coverage then. |

Available Term insurance on FSMOne |

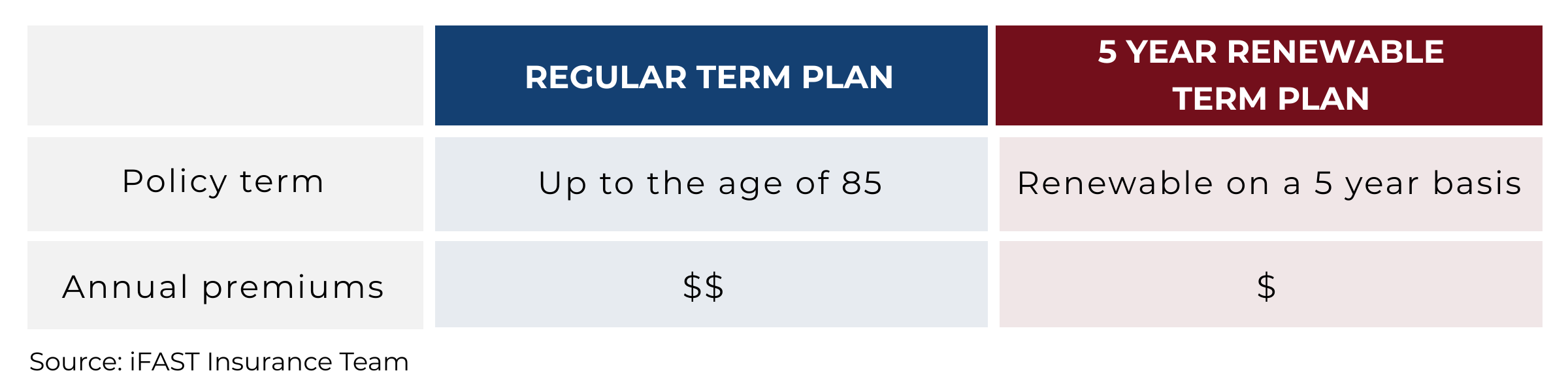

Apart from a regular term plan, ECI riders can also be added onto a 5 year renewable term plan. For this coverage option, we are looking at a term plan that is offered on a 5 year basis and can be renewed every 5 years. Offering the same coverage as regular term plans, the difference between these two options is the policy term and annual premiums.

With a shorter coverage period, premiums for 5 year renewable term plans tend to be lower than those of regular term plans. However, do note that the premiums for such renewable plans are not guaranteed with there being a risk of premiums increasing at the next renewal cycle.

Type of coverage |

Add-on early critical illness (ECI) rider to a 5 year renewable term plan. |

Features |

The addition of an early critical illness (ECI) rider to a term plan will allow your policy to cover for critical illness. The coverage period of this ECI rider will follow the policy term of the main plan (your term insurance).

For this option, coverage is offered on a 5 year basis and is renewable every 5 years. |

Pay-outs |

Pay-outs for critical illness are staggered and paid in stages of early, intermediate and advanced stage critical illness. |

Pros |

Premiums are lower than a regular term plan.

Doubles up as both a protection and critical illness plan. Affordable alternative to getting critical illness coverage. |

Cons |

Premiums are not guaranteed and may increase at every renewal with this subjected to the insurer's discretion.

Coverage is only given for as long as the policy owner is paying for the premiums. This means that you have to pay for your plan for as long as it is in force. E.g. you would still be paying for your insurance premiums at age 70 should you wish to receive coverage then. |

Available Term insurance on FSMOne |

(See "Is Your Term Insurance A Costly Mistake?")

To only have to pay for your premiums for a limited number of years

Type of coverage |

Add-on early critical illness (ECI) rider to a whole life plan |

Features |

The addition of an early critical illness (ECI) rider to a whole life plan will allow your policy to cover for critical illness. The coverage period of this ECI rider will follow the policy term of the main plan (your whole life insurance). |

Pay-outs |

Pay-outs for critical illness are staggered and paid in stages of early, intermediate and advanced stage critical illness. |

Pros |

Coverage is given for life as long as the policy owner pays the premiums for the specified time period (e.g. 15, 20 or 25 years).

Doubles up as both a protection and critical illness plan. Whole life insurance accumulates cash values and therefore has a surrender value. This allows you the flexibility to surrender and cash out your policy should a need arise. |

Cons |

Higher upfront annual premiums due to the limited pay function of whole life insurance. |

Available whole life insurance on FSMOne |

Manulife LifeReady Plus, Manulife ReadyLife Income, NTUC Star Assure, NTUC Star Prime Life, NTUC Legacy Solitaire, TM Legacy Lifeflex

|

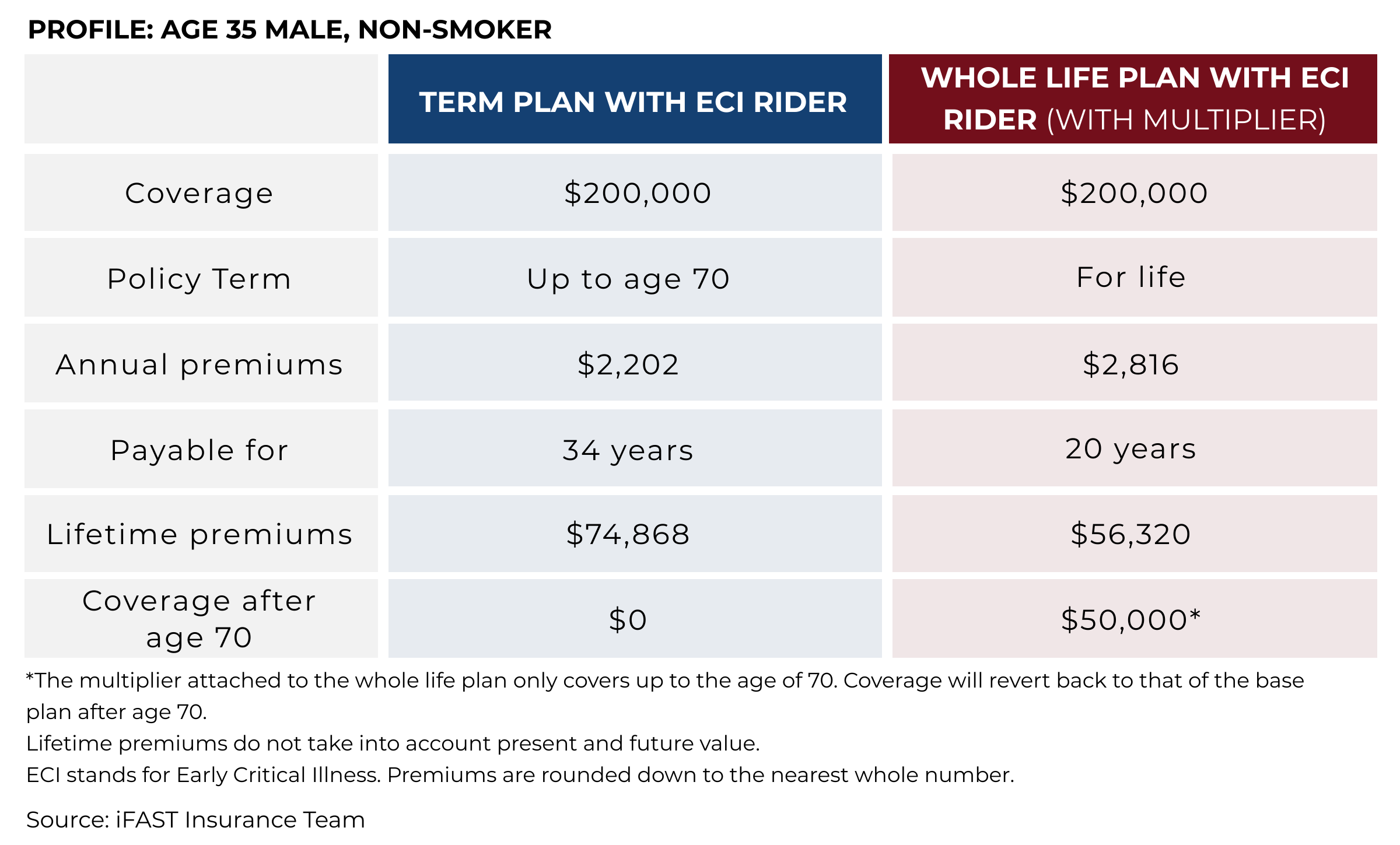

Similar to term plans with ECI rider, the addition of an ECI rider to a whole life plan will allow your policy to also cover for critical illnesses. This will allow your whole life plan to double up to provide both protection and critical illness coverage.

While the upfront annual premiums of a whole life plan is higher, whole life plans have the option to only pay for premiums for a specified time period (i.e. limited pay). This means that you would be able to enjoy a lifetime of coverage as long as you pay the premiums for the specified time period (e.g. 15, 20 or 25 years). On the other hand, coverage for term plans are only given for as long as premiums are being paid. Your term plan will lapse when you stop paying your premiums.

As shown in the table, while the annual premiums of a whole life plan with ECI rider is higher, the limited pay benefit of whole life plans results in the lifetime premiums being lower than that of a term plan with ECI rider. Additionally, with whole life plans, the insured can continue to receive basic protection and ECI coverage for life.

Lastly, whole life plans accumulates cash values, thus allowing you the flexibility to surrender your policy and receive the surrender value should the need arise.

In summary,

Coverage |

Cost |

|

Standalone single pay-out critical illness plan |

✔✔ |

$$ |

Standalone multi-pay critical illness plan |

✔✔✔ |

$$$ |

Direct purchase critical illness plan |

✔ |

$ |

Targeted critical illness plan |

✔ |

$$ |

Cancer plan |

✔ |

$ |

Add-on early critical illness (ECI) rider to a term plan |

✔✔ |

$$ |

Add-on early critical illness (ECI) rider to a 5 year renewable term plan |

✔✔ |

$ |

Add-on early critical illness (ECI) rider to a Whole Life plan |

✔✔ |

$$ |

On understanding critical illness coverage:

The Basics Of Critical Illness Insurance

Choosing the right critical illness coverage. Part 1

Cheap Critical Illness Cover For Those In Their 30s

Comparing Critical Illness Coverage 2020

Critical illness coverage on a budget for age 40 and above

Over 8,100 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

![]()

Promotion: From now till 31 October, receive 1,000 Reward Points* when you transfer your shield plan into FSMOne. *Terms and Conditions apply. Click here to find out more.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Chubb, Etiqa Insurance, FWD Insurance, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Best Personal Accident Insurance Singapore 2020

Don't Make These 3 Mistakes With Your Home Insurance