In our previous article "The Basics Of Critical Illness Insurance", we simplified the technicalities of critical illness insurance and explained how these plans work. With a clearer understanding on the purpose and function of critical illness insurance, we now move on to the next part: choosing the right critical illness coverage. In this article, we elaborate on some of the ways to get coverage for critical illnesses.

#1 A standalone plan

Type of coverage |

Standalone single pay-out critical illness plan |

Features |

Covers for claims for a single critical illness. |

Pay-outs |

Pay-outs are staggered and paid in stages of early, intermediate and advanced stage critical illness. |

Pros |

The most straightforward way of getting coverage for critical illness.

Premiums usually start low but will increase with age. |

Cons |

Covers only for a single critical illness. No coverage is given should the insured be diagnosed with subsequent critical illnesses.

|

Product(s) available on FSMOne |

The most straightforward way of obtaining critical illness coverage is through the use of a standalone single pay critical illness insurance plan. Such plans will provide coverage for a specified list of critical illness conditions and procedures with this list varying slightly between insurers. Pay outs for such plans are staggered according to the different stages of critical illnesses (e.g. early, intermediate and advanced) with a cap on the amount you can receive at each stage of critical illness.

While such plans are easy to understand, do note that they only cover for a critical illness once. Upon paying out the full sum assured to the individual, these plans will terminate and no further coverage is given should the insured be diagnosed with another critical illness.

#2 A plan that covers for multiple critical illnesses

Type of coverage |

Standalone multi-pay critical illness plan |

Features |

Continual protection even after a critical illness claim.

Multiple pay-outs given across various stages of different critical illnesses. |

Pay-outs |

Pay-outs are staggered and paid in stages of early, intermediate and advanced stage critical illness. |

Pros |

Ability to make multiple claims for different critical illnesses with coverage “restarting” after a claim is made.

Receive pay-outs of up to 900 per cent of your sum assured. |

Cons |

Premiums may be more expensive.

Plans tend to be more complicated and may be difficult to understand. |

Product(s) available on FSMOne |

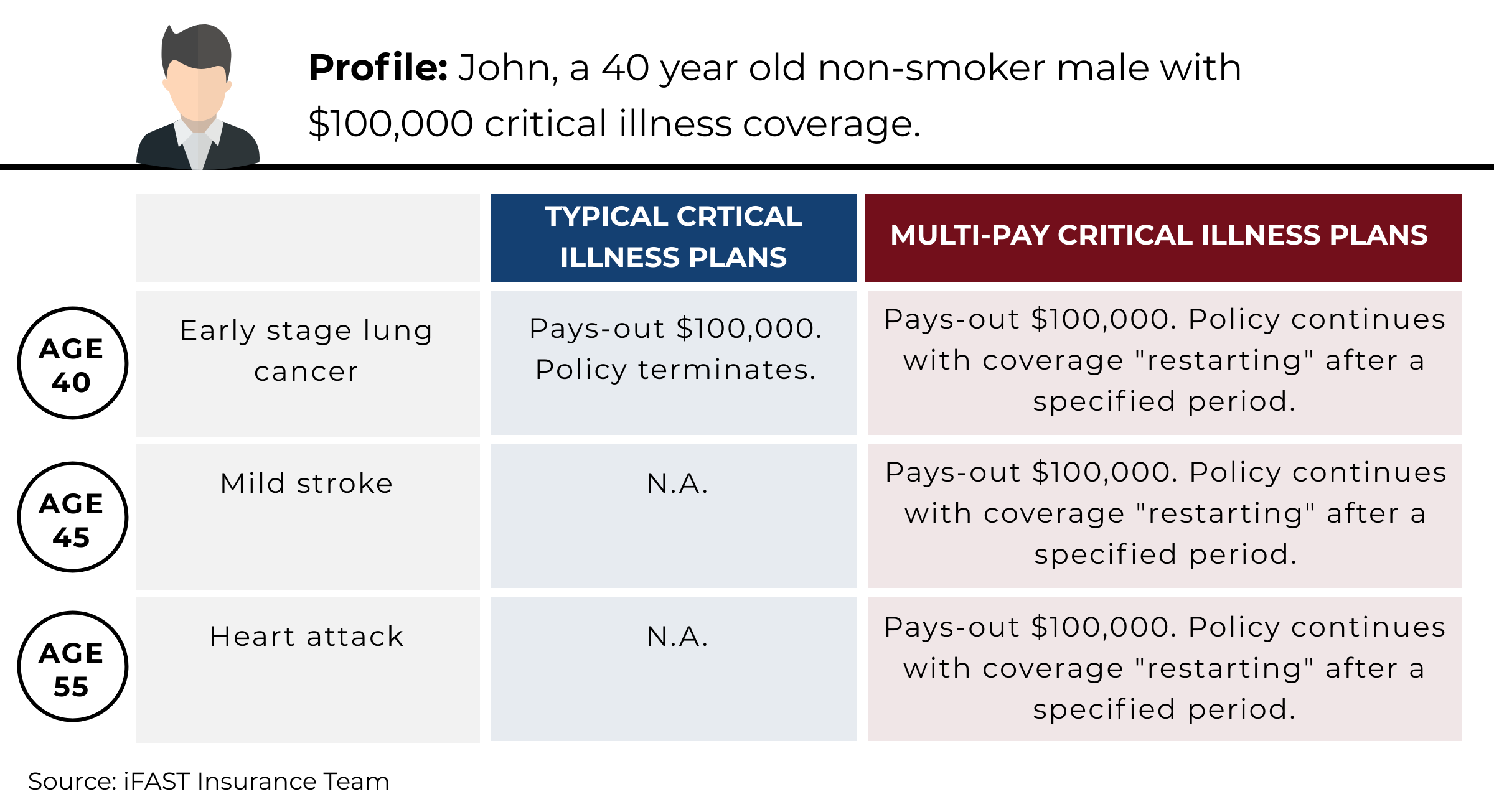

A multi-pay critical illness plan provides the most comprehensive coverage with continual protection offered against critical illnesses even after a critical illness claim. This means that you can make multiple claims for different critical illnesses and will not have to worry about lacking coverage after one critical illness claim.

For example, John has a multi-pay critical illness plan. At age 40, John is diagnosed with early stage lung cancer and receives a pay-out from his policy. A few years later, John suffers from a mild Stroke. With a multi-pay critical illness plan, he enjoys continual coverage even after a critical illness claim. This means that he will still be covered for his subsequent critical illness (i.e. mild stroke) and will be able to make another claim.

Typical critical illness coverage options only covers for a single critical illness. Coverage will terminate upon the 100 per cent pay-out of your sum assured. Multi-pay plans however allows coverage to “restart” after a fixed time period with claims payable for more than 100 per cent of your sum assured. Such plans thus allows for peace of mind knowing that you will still be able to receive coverage should you suffer from subsequent critical illnesses.

However, multi-pay plans tend to be more complicated with the multi-pay benefit triggered by various categories and conditions. Additionally, while multi-pay plans reassures in the face of multiple critical illnesses, do note that such plans will have higher premiums.

#3 A faster way to get insured with pay-outs given upon diagnosis

Type of coverage |

Standalone direct purchase critical illness insurance plan |

Features |

Coverage for specified critical illnesses with the option to purchase online without financial advice. |

Pay-outs |

Lump sum pay-out may be given upon diagnosis of critical illness or staggered and paid in stages with this dependent on the conditions of the plan purchased. |

Pros |

Straightforward process of purchase with application and claims done directly online.

Direct purchase insurance usually do not require medical underwriting. Competitive premiums. |

Cons |

Coverage may not be as comprehensive as compared to traditional critical illness plans.

|

Product(s) available on FSMOne |

Direct purchase critical illness plans are plans that can be directly purchased online and can be sold without financial advice. These plans are suitable to be used by those who already know what product or coverage they require and do not need further advice.

In general, such plans tend to have lower premiums and do not require medical underwriting. With the option to purchase and claim directly online, direct purchase critical illness plans tend to be more straightforward and are simple to understand. If you already know what product or coverage you require, you may consider getting direct purchase critical illness insurance.

However, a point to note is that the coverage from direct purchase critical illness insurance may be less comprehensive than the coverage from traditional critical illness insurance. For example, direct purchase insurance tend to have lower coverage levels with the Direct Insurance Purchase Guidelines regulating that individuals may buy no more than S$400,000 sum assured per insurer.1

#4 A plan that targets specific illnesses or conditions

Type of coverage |

Standalone targeted plan |

Features |

Covers for claims of specified conditions and procedures. |

Pay-outs |

Lump sum pay-out may be given upon diagnosis of critical illness or staggered and paid in stages with this dependent on the conditions of the plan purchased. |

Pros |

Tailored for a specific demographic, these plans will offer comprehensive coverage if you are concerned about certain medical conditions. |

Cons |

With its targeted coverage, these plans may not be suitable for all. |

Product(s) available on FSMOne |

With these critical illness plans targeted at a specific group, they are not suitable to be used by all. Instead, such plans would only be suitable for those who are worried about a certain condition. Individuals who fall outside of the targeted group will not be interested in these plans nor will they find them suitable.

For example, NTUC Lady 360 is a plan tailored for females and will cover for female specific procedures and conditions such as reconstructive surgery for mastectomy, eggs freezing and hormone replacement therapy.

On the other hand, FWD’s Heart Attack and Stroke plans covers for a single condition each: heart attack and stroke. With low premiums, these plans cater to individuals who are particularly worried about getting a heart attack or stroke and wish to get low cost coverage for this specific condition.

#5 Coverage even for pre-existing medical conditions

Type of coverage |

Standalone cancer plan |

Features |

Coverage for all stages of cancer. |

Pay-outs |

Lump sum pay-out may be given upon diagnosis of critical illness or staggered and paid in stages with this dependent on the conditions of the plan purchased. |

Pros |

Affordable premiums for up to $200,000 sum assured.

No medical check-up required. Option to purchase and claim directly online for certain plans. Lump sum pay-out is given upon the diagnosis of cancer for some plans. |

Cons |

Only covers for cancer. |

Product(s) available on FSMOne |

Cancer plans are often seen as an alternative for critical illness insurance with these plans offering coverage for all stages of cancer. Unlike typical critical illness plans where pay-outs are staggered and paid in stages, some cancer plans may offer a lump sum pay-out upon a cancer diagnosis.

With affordable premiums, individuals may use cancer plans to complement existing coverage. Alternatively, those who are currently unable to afford critical illness coverage may consider cancer plans for some coverage against the top critical illness.

Additionally, cancer plans tend to have a simplified application process with no medical underwriting required. This means that you may still be able to receive coverage even if you have existing non-cancer related medical conditions.

(See "Best Cancer Insurance Singapore")

On understanding critical illness coverage:

The Basics Of Critical Illness Insurance

Choosing the right critical illness coverage. Part 2

Cheap Critical Illness Cover For Those In Their 30s

Comparing Critical Illness Coverage 2020

Critical illness coverage on a budget for age 40 and above

Over 8,100 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

![]()

Promotion: From now till 31 October, receive 1,000 Reward Points* when you transfer your shield plan into FSMOne. *Terms and Conditions apply. Click here to find out more.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Chubb, Etiqa Insurance, FWD Insurance, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Best Critical Illness Insurance Singapore 2020

Is Your MINDEF Group Insurance Really The Cheapest?

Are Integrated Shield Plans Necessary?

Diabetes and Glaucoma – Will Your Insurance Cover This?

How Much Can I Receive From An Annuity?

----

1Source: https://www.lia.org.sg/media/1516/mu-6318-dpi-guidelines.pdf