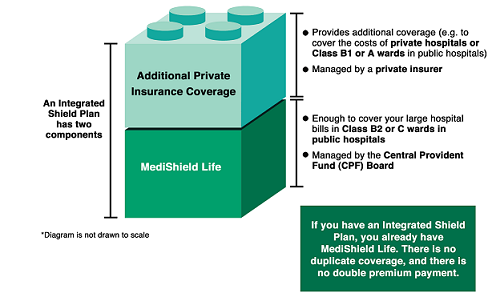

1. What is MediShield Life (MSHL)?

MediShield Life is a basic health insurance plan that offers universal coverage to all Singapore Residents. This means that all Singapore citizens and Permanent Residents (PRs) will be covered for life by MediShield Life regardless of pre-existing conditions or other life circumstances.

MediShield Life provides coverage for Class B2/C wards in public hospitals.

2. Do I really need Integrated Shield (IP) plans?

Offered by seven private insurers, IP plans allow individuals to enhance their coverage by offering more benefits such as as-charged coverage. Coverage is also given for private hospitals, with IP plans having a higher annual policy limit of up to $2.5 million. (Note: Annual policy limit will differ between plans.)

You may also consider adding on IP riders to further enhance your coverage and reduce or remove the co-insurance and deductible required.

(Source: https://www.moh.gov.sg/healthcare-schemes-subsidies/medishield-life)

3. I have an Integrated Shield (IP) plan, will I have to pay any out-of-pocket medical expenses?

An integrated shield plan is designed to allow individuals to enjoy treatment at higher ward classes (e.g. Ward B1 and above in public hospitals, or at private hospitals). IP plans also provide more comprehensive coverage such as higher cancer treatment coverage, as-charged inpatient benefits, and pre- or post- hospitalisation treatment benefits. With an IP plan alone, you will still have to pay co-insurance and the annual deductible.

If you would like to reduce your out-of-pocket expenses, opt for an IP rider. Some riders will remove your annual deductible and also reduce the co-payment needed. IP riders will also cap the maximum co-payment amount needed.

For Enhanced IncomeShield plans:

Medical bill from a panel provider |

Deductible needed for Private hospital |

Co-insurance payment needed |

Total out of pocket expense needed |

|

Enhanced IncomeShield Preferred |

$100,000 |

$3,500 |

($100,000 - $3,500) x 10% = $9,650 |

$3,500 + $9,650 = $13,150 |

Enhanced IncomeShield Preferred + Deluxe Care Rider |

$100,000 |

N.A. |

5% co-insurance capped at $3,000 with Deluxe Care rider |

$3,000 |

Enhanced IncomeShield Preferred + Classic Care Rider |

$100,000 |

N.A. |

10% co-insurance capped at $3,000 with Classic Care rider |

$3,000 |

Information generated on 18 November 2024, for illustration purposes only.

For Singlife Shield plans:

Medical bill from a preferred provider |

Deductible needed for Private hospital |

Co-insurance payment needed |

Total out of pocket expense needed |

|

Singlife Shield Plan 1 |

$100,000 |

$3,500 |

($100,000 - $3,500) x 10% = $9,650 |

$3,500 + $9,650 = $13,150 |

Singlife Shield Plan 1 + Private Prime rider |

$100,000 |

N.A.* |

$100,000 x 5% = $5,000 (but capped at $3,000 with Private Prime rider) |

$3,000 |

Singlife Shield Plan 1 + Private Lite rider |

$100,000 |

$3,500 |

($100,000 - $3,500) x 5% = $4,825 (but capped at $3,000 with Private Lite rider) |

$3,500 + $3,000 = $6,500 |

*For A&E or Preferred medical providers which may be found at https://singlife.com/medicalspecialists.

Information generated on 18 November 2024, for illustration purposes only.

4. Do Integrated Shield plans provide coverage for outpatient expenses?

Integrated Shield plans provide coverage for specified outpatient treatments such as kidney dialysis, or radiotherapy for cancer. For illnesses such as the common flu or for visits to the General Practitioner (GP), your IP plan will not provide coverage.

5. Can I seek treatment at a higher ward class than what my plan entitles me to?

Yes, you can seek treatment at a higher ward class than what your plan entitles you to. However, your coverage will be pro-rated according to the ward class entitlement of your plan.

This means that if you are on a standard IP plan with B1 ward coverage, but seek treatment at private hospitals, you should expect to pay higher out of your own pocket costs as your plan will only cover a smaller proportion of your hospital bill.

An illustration:

Ward Entitlement of plan |

Pro-ration factor if treatment is sought at private hospitals |

|

Enhanced IncomeShield Basic |

B1 Ward class and below in public hospitals |

50% |

Singlife Shield Plan 3 |

Standard B1 ward of a public hospital |

35% |

Information generated on 18 November 2024, for illustration purposes only.

6. How do I afford the increasing Integrated Shield premiums as I get older?

If you think your premiums are getting too high, here are the two things to ask yourself:

Keep your current coverage if you are still able to afford your current premiums. Only consider downgrading your plan if you are no longer able to afford your premiums as it is easy to downgrade your IP plan but harder to upgrade your IP plan should you need to do so in future.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://ask.gov.sg/moh/questions/cm2vs8bet00lkr5bfw987rvw4?from=topics

https://isomer-user-content.by.gov.sg/3/771e8dc9-7d46-45eb-9f91-bad20eff0450/comparison-of-private-hospital-ips.pdf

https://www.income.com.sg/kcassets/48ba2802-266a-4bec-b7cb-b61bff0e0f7c/Final%20Enhanced%20IncomeShield%20policy%20conditions%201%20Nov%202024.pdf

https://www.income.com.sg/kcassets/2b6a2966-c927-48ac-8fe8-26be5005d11b/Final%20Conditions%20for%20Deluxe%20Care%20Rider%201%20Nov%202024.pdf

https://www.income.com.sg/kcassets/b6b7c771-e78d-4a67-8733-87569af3eb80/Final%20Conditions%20for%20Classic%20Care%20Rider%201%20Nov%202024.pdf

https://singlife.com/content/dam/public/sg/documents/promotion/H44%20Singlife%20Shield%20TCs%20Sept%202024.pdf

https://singlife.com/content/dam/public/sg/documents/promotion/H46%20Singlife%20Health%20Plus%20TCs%20Sept%202024.pdf

Information retrieved on 18 November 2024.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.