Did you know that Singapore pays more for cancer drugs as compared to that of Australia and South Korea? The spending on cancer drugs in Singapore has increased at a compounded rate of 20 per cent with MediShield Life paying out 50 per cent more for cancer treatments today as compared to that in 2017.1 As such, the government recently announced changes to MediSave and MediShield Life that will affect the coverage for cancer treatments. This is set to be effective from September 2022 with coverage from integrated shield plans changing from April 2023 onwards. These changes aim to moderate the increases in healthcare costs, in particular the cost of expensive cancer drug treatments.

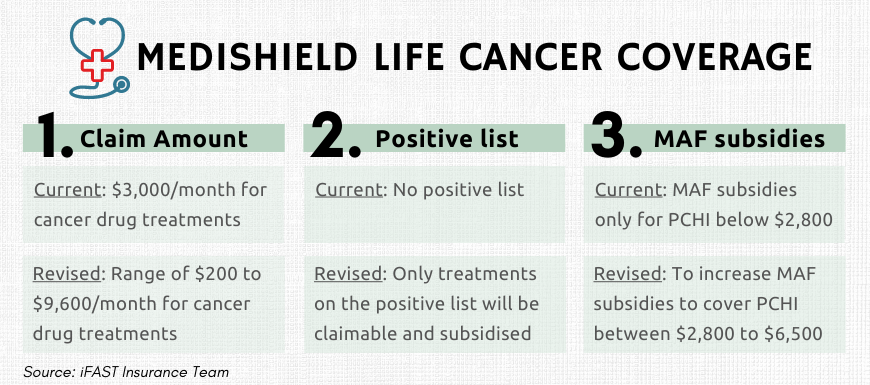

These are the 3 main changes to your MediShield Life cancer coverage

#1 Changes in claim amount for outpatient cancer drug treatments

Currently, MediShield Life allows a claim amount of $3,000 per month for all cancer drug treatments and services. This has however resulted in pharmaceutical companies raising prices to maximise the claims from MediShield Life.

Under the revised changes, claim amount will be changed to a range of $200 to $9,600 a month for drugs on the positive list only. Not only will this align the different cancer drug treatment costs but it will also allow for negotiations with pharmaceutical companies to lower their prices so their drugs can be included in the positive list. A separate claim limit of $1,200 per year will be created for outpatient cancer drug services to cover other expenses such as doctor consultations, scans, and blood tests.

Current |

Revised |

|

MediShield Life |

$3,000 per month for all cancer drug treatments and services. |

Range of $200 to $9,600 per month for cancer drug treatments on the positive list.

Additional $1,200 per year for cancer drug services. |

MediSave |

$1,200 per month for all cancer drug treatments and services.

Additional $600 per year for cancer scans.* |

$1,200 per month for cancer drug treatments with MediShield Life claim limit above $5,400, and $600 per month for other treatments on the positive list.

Additional $600 per year for cancer drug services and/or other cancer scans.* |

*MediSave can also be used for scans for post-treatment monitoring and radiotherapy patients.

(See "Cover Your “Missing” Hospitalisation Cash Benefits With These 3 Plans")

#2 Treatments on the MediShield Life positive list will get more subsidises from the government

The revised MediShield Life coverage will create a positive list for cancer drug treatments. This list will cover 90 per cent of the existing treatments in the public sector and will increase the percentage of subsidised Singaporean patients who can have their bills fully covered for their cancer drug treatments.2 This means that under the revised cancer coverage, close to 90 per cent of subsidised Singaporean patients who use treatments from the positive list will have their bills fully covered by subsidies and MediShield Life. This will be subjected to a 10 per cent co-payment for MediShield Life which can be paid via MediSave.

Additionally, while most Integrated Shield plans currently provide as-charged coverage for outpatient cancer drug treatments, this will change together with the revised MediShield Life coverage. From April 2023, Integrated Shield plans will only cover treatments that are on the MediShield Life positive list. Treatments not included in the positive list will not be covered by MediShield Life and MediSave.3

#3 More will be eligible for subsidies for specified high cost drugs

The Medication Assistance Fund (MAF) subsidies will be enhanced to include Singaporeans with a higher per capita household income (PCHI). Currently, Singaporeans will receive 50 to 75 per cent subsidies only if they have a monthly per capita household income below $2,800. Those with a PCHI above $2,800 will not be eligible for subsidies.

However, in future, the criteria to receive subsidies will be raised from the current PCHI of $2,800 to $6,500. This will help more Singaporeans to be eligible for these subsidies for specified high cost drugs.

| Monthly per capita household income (PCHI) | Current |

Revised |

Between $0 to $2,000 PCHI |

75% |

75% |

Between $2,000 to $2,800 |

50% |

50% |

Between $2,800 to $3,300 |

0% |

50% |

Between $3,300 to $6,500 |

0% |

40% |

Above $6,500 |

0% |

0% |

(See "What durians can teach you about your Critical Illness plan")

What these changes means for us

This means that Singaporeans and PRs who have MediShield Life can expect a lower amount payable via MediSave if we use clinically proven and cost-effective cancer drug treatments. This is the result of a lower pre-subsidy bill for cancer drug treatments together with higher subsidies given for treatments on the positive list. More Singaporeans will also be eligible for MAF subsidies with high cost drugs also included in future subsidies.

Illustration of a Singaporean with breast cancer, requiring one high-cost drug and one low-cost drug treatment.

Cancer drug bill |

||

Current |

Revised |

|

Bill before subsidy |

$3,130 |

$1,785 |

Subsidy given |

$10 |

$890 |

Amount claimable from MediShield Life |

$2,805 |

$800 |

Net amount payable |

$315 |

$95 |

Amount payable via MediSave |

$315 |

$95 |

Your out-of-pocket expenses |

$0 |

$0 |

Information as shown by Ministry of Health.4

Do note that your MediShield Life is subjected to a 10% co-insurance. You may use your MediSave to pay this 10% co-insurance.

For patients currently undergoing cancer treatments

These changes to MediShield Life are set to be implemented only in September 2022. This will allow patients who are currently undergoing treatments to complete their current treatments and adjust their course of treatment accordingly.

With these revisions to MediShield Life allowing for higher coverage levels, will I still need a cancer plan?

The revised coverage from MediShield Life will allow higher coverage for cancer treatments. However, it is important to understand that cancer insurance serves a different purpose. This is because while MediShield Life covers for cancer treatments, coverage is given on a reimbursement basis. This means that if your treatment costs $1,000, MediShield Life will reimburse you $1,000 and nothing more. As such, while MediShield Life will cover your hospitalisation and selected outpatient treatments, it will not provide any income replacement. This is when a cancer plan comes into play.

Unlike MediShield Life that operates on a reimbursement basis, cancer plans will provide a lump sum pay-out when conditions are fulfilled. This can either be a full 100 per cent pay-out given upon diagnosis or may be given in staggered amounts based on the severity of your illness. This can then serve as your income replacement during your recovery period. Alternatively, your pay-outs from a cancer plan can also be used for your daily expenses, to pay for any household expenses, or even to pay for a certain treatment that may not be included in MediShield Life’s positive list.

MediShield Life |

Cancer insurance plans |

|

Type of coverage |

Reimbursement basis |

Lump sum pay-out |

Administered by |

CPF board |

Private insurers |

Typically used for |

Hospitalisation coverage and specified outpatient treatments. |

Income replacement during your recovery period. Pay-outs can also be used for long-term care costs, daily expenses or any other uses as you deem fit. |

(See "Cheap Cancer Insurance Singapore 2021")

Cancer insurance plans available on FSMOne:

Name of plan |

Allianz Cancer Protect |

FWD Cancer Insurance |

MSIG CancerCare Plus |

NTUC Cancer Protect |

TM Protect Cancer |

Annual premiums^ (after discounts) |

304.08 |

$161.19 |

$155.22 |

$334.60 |

$263 |

Ongoing promotions |

30% off first year premiums. T&Cs apply. |

20% off premiums. Valid until 31 October 2021. T&Cs apply.

| - |

- |

^Profile: Age 40, non-smoker male for $100,000 sum assured. Premiums shown are before discounts and is accurate as of 6 December 2021.

Let FSMOne help you with your insurance planning

Over 10,300 users trust FSMOne with their insurance planning.

Live better, safer. Get a free review from our advisers today!

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Is CPF Life enough for me to retire?

Should I switch from Eldershield to CareShield Life?

Is maternity insurance a must-have for all expecting mothers?

Best Personal Accident Insurance 2021

How much should I be spending on insurance for my child?

----

1 Source: https://www.moh.gov.sg/docs/librariesprovider5/default-document-library/annex-a12145e9763d74fe587ad80b942d86fdb.pdf

2 https://www.moh.gov.sg/home/our-healthcare-system/medishield-life/what-is-medishield-life/what-medishield-life-benefits/outpatient-cancer-drug-list

3 Source: https://www.moh.gov.sg/news-highlights/details/government-enhances-subsidies-to-improve-affordability-of-cancer-treatment_17Aug2021

4 Source: https://www.moh.gov.sg/docs/librariesprovider5/default-document-library/annex-b880319b554ef4ba881959cd09d6f32b4.pdf