Are you wondering what the link between buying durians and getting insurance coverage is? While it may seem absurd to link the two together, they actually have more points in common than you would think. In fact, we can even apply some of our "lessons" learnt from buying durians to getting insurance coverage! In this article, we simplify the process of buying critical illness insurance by explaining it in durian terms.

Durians and insurance

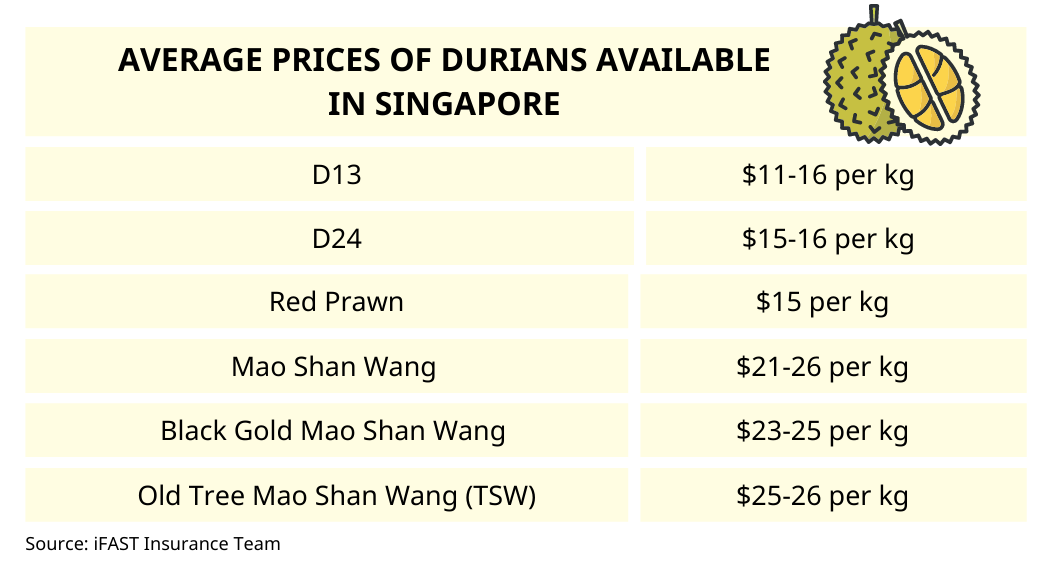

A quick search on Google will reveal the extensive variety of durians that we have access to in Singapore with prices varying greatly between the different cultivars. Prices for these durians start from as low as $2 per durian1 and can go up to $116 per kilogram.

When we buy durian, we naturally expect the quality and taste of the durian to commensurate with the price that we pay. If you pay $116 per kilogram for your extra premium Pahang Signature Black Gold durian2, naturally this should not taste the same as your typical Mao Shan Wang. Likewise, we cannot expect to only pay $2 a durian and expect it to be a premium Mao Shan Wang. Just like how durians come in various grades and price points, the same applies to insurance coverage too, especially critical illness insurance.

#1 You get what you pay for - both durians and critical illness insurance

Just like how you will not expect premiums durians to cost just $2, the same should apply when it comes to getting critical illness insurance coverage. While this does not mean that the most expensive policy will have the best coverage, you should expect your coverage to correspond with your premiums. This means that benefits in your policy such as a complimentary health checkup and/or continual protection even after a critical illness claim will likely result in a higher premium required.

An example of such durian |

Price point |

What it means in critical illness insurance terms |

|

Premium durians |

Mao Shan Wang |

Average of $21 to $25 per kilogram |

Early critical illness insurance |

Basic durians |

"Non-branded" durians |

$2 per durian |

Traditional critical illness insurance |

#2 Cheap, "non-branded" durians are like getting basic critical illness insurance

To put your durian buying habits into critical illness insurance terms, this basically means that basic durians are like basic critical illness insurance. While basic durians are still durians, you would not expect them to taste like a Mao Shan Wang. Likewise, while a basic critical illness plan will cover you for critical illness, this will only be for the 37 specified critical illnesses as defined by Life Insurance Association (LIA). Coverage will also only be given for advanced stage diagnosis. This means that you should you be diagnosed at an early or intermediate stage of critical illness, you will not get coverage nor receive a pay-out that can tide you through your recovery period.

(See "3 Reasons To Not Get Basic Critical Illness Insurance")

#3 Premium durians are like early critical illness insurance

A rich and creamy tasting durian, Mao Shan Wang is the popular, premium durian that most people opt for. In this case, Mao Shan Wang is like your early critical illness insurance. Just like how you can get a more premium durian by paying a little more for Mao Shan Wang, doing the same will allow you to get a critical illness plan with better coverage. This means that in addition to covering the 37 LIA specified critical illnesses, early critical illness plans may also cover for up to 129 conditions. This includes coverage for early, intermediate and advanced stages of critical illness. These plans may even provide a full pay-out upon a critical illness diagnosis.

As we mentioned in our article "Do You Really Need Early Critical Illness Insurance?", early critical illness is important and should be obtained by all working adults. Not only will this allow us income replacement should we need time off to recover, but the pay-outs from an early critical illness can also be used for our long-term medical expenses, treatment costs or any other daily living expenses that we may incur from the change in lifestyle required.

There are two types of early critical illness coverage:

1. Traditional early critical illness plans

2. Direct purchase early critical illness

Traditional early critical illness plans

Pros: |

Cons: |

Traditional early critical illness plans available on FSMOne:

Manulife - ReadyCompleteCare, Critical SelectCare Tokio Marine - TM MultiCare, TM EarlyCover |

|

Consider a traditional early critical illness plan if you would like an adviser to guide you through your application and claims process. While premiums for these plans tend to be higher than those of a direct purchase early critical illness plan, traditional plans offer coverage for a wider range of critical illness conditions. Some plans will even cover for multiple critical illnesses, with your sum assured benefit restarting after a specified number of months.

(See "Choosing the right critical illness coverage. Part 1")

Direct purchase early critical illness plans

Pros: |

Cons: |

Direct purchase early critical illness plans available on FSMOne:

FWD - Big 3 Critical Illness |

|

Promotion: Use promo code "IFAST" to enjoy 35% off your FWD Big 3 Critical Illness plan. |

|

Direct purchase early critical illness plans are suitable for individuals who wish to get an affordable fuss-free coverage against critical illness. With application and claims made directly online, there is no need to undergo any medical underwriting. Instead, applicants will only be asked to answer a simple health declaration during application.

While direct purchase early critical illness plans such as FWD’s Big 3 may cover for less critical illnesses as compared to traditional plans, we feel that coverage is still sufficient for those looking for an affordable alternative to traditional early critical illness plans. This is because the three illnesses covered by Big 3 (Cancer, Heart Attack and Stroke) are the top most commonly claimed critical illnesses in Singapore with these making up 90 per cent of critical illness insurance claims.4 Additionally, premiums are affordable and starts from just $14 a month^. The premiums for FWD’s Big 3 are also kept affordable even for those in the older age groups, thus making it suitable to be used as an entry level early critical illness plan.

Cost of annual premiums for $100,000 coverage for a non-smoker:

Age 20 |

Age 30 |

Age 40 |

Age 50 |

Age 60 |

|

Male |

$231.80 |

$253.80 |

$322 |

$771.30 |

$1591.70 |

Female |

$280.80 |

$314.50 |

$453.80 |

$910.60 |

$1353.70 |

*Premiums shown are before discounts and are rounded down to the nearest whole number. Information accurate as of 1 September 2021 with changes subjected to the insurer's discretion.

(See "Critical illness coverage on a budget for age 40 and above")

Over 10,300 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

^Profile: Age 30, non-smoker male for $100,000 coverage. Premium stated is after discount and is accurate as of 1 September 2021.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Cheap Cancer Insurance Singapore 2021

Is maternity insurance a must-have for all expecting mothers?

Fixed or Renewable – Which is the better term insurance?

Should I switch from Eldershield to CareShield Life?

Disappointed with the new integrated shield riders? This is what we think

----

1Source: https://www.todayonline.com/8days/eatanddrink/newsandopening/sheng-siong-now-sells-3-10-red-prawn-15kg-msw-durians

2Source: https://www.mrlifechanger.com/best-durian-price-singapore/

3Source: https://blog.seedly.sg/price-compilation-cheapest-durian-singapore-mao-shan-wang/

4Source: https://www.genre.com/knowledge/publications/ri15-4-droste-xiang-en.html