What are endowments?

Endowments, also known as a saving plan, are a disciplined way to save. By helping us to build up a pool of savings over a fixed period of time, endowments can be used to help us to achieve our financial goals.

For endowments, you will be required to pay a fixed amount at regular intervals (e.g. monthly, quarterly, or annually), for a specified time period (e.g. 5 to 25 years). This frequency of payment can be adjusted according to your preference.

(See "The Truth About Endowments")

What happens at the maturity of my endowment plan?

Your endowment has a cash value that comprises of both guaranteed and non-guaranteed components. At maturity, your cash value will be paid out to you and your policy terminates. While it may sound similar to a fixed deposit, endowments will require you to commit to the full policy period in order to reap the highest benefits. Not only would you receive lower returns should you choose to surrender your plan for an early withdrawal, but you may also have a pay a penalty for doing so.

(See "When Is Whole Life Insurance The Better Option?")

If you purchased an endowment plan with the intention of saving towards a saving goal, then congratulations, you have achieved your goal! Upon maturity of your endowment, you will receive a lump sum pay-out. This can then be used for the goal that you were saving towards.

However, if you had purchased an endowment as part of your retirement planning, then this is our advice to you.

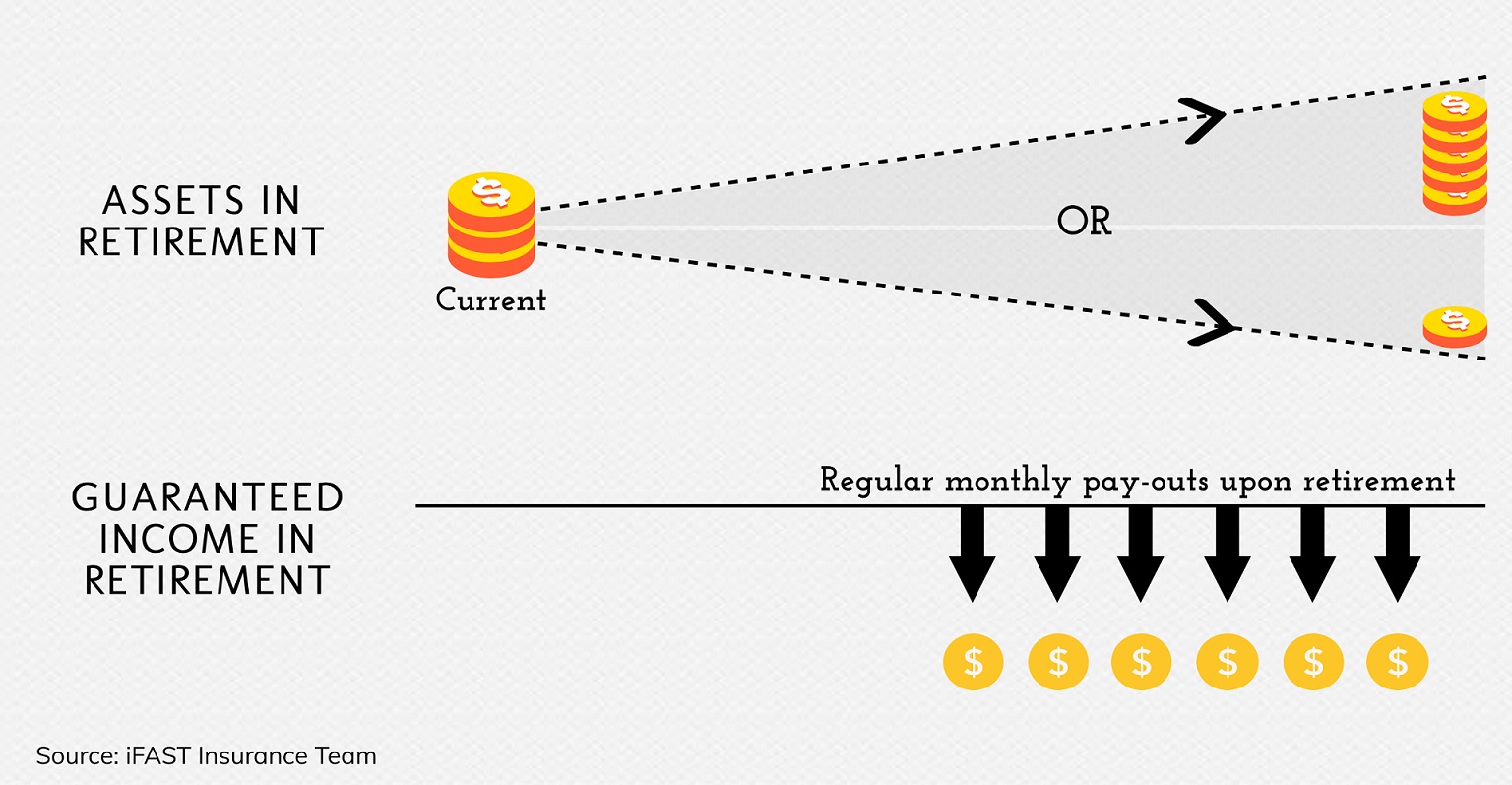

Switch to annuities for retirement

If you bought an endowment with the intention of planning for your retirement, you may want to consider switching to an annuity plan instead. Commonly used for retirement planning, annuities offer the option to receive a regular stream of income in retirement.

Annuities are suitable for: |

Annuities are not suitable for: |

The time frame for annuities

Similar to endowments, annuities require premiums to be paid first before pay-outs commence at a later date. Payment of premiums can be done via a one-off payment (i.e. single premium) or a regular payment for a specified period of time (i.e. limited pay).

With annuities, you are given the option to choose when you want your pay-outs to begin. This allows you time your pay-outs to start at your desired retirement age.

(See "Want An Early Retirement? Achieve Your Retirement Goals With Annuities")

Pay-outs from annuities

While the returns of annuities may not be as high as compared to investments, most annuities have a guaranteed cash value component. Like endowments, the cash value or pay-outs from annuities are made up of a guaranteed and non-guaranteed component. This proportion of guaranteed and non-guaranteed pay-outs will differ between plans with some plans having a higher guaranteed portion and others having a higher non-guaranteed portion.

Guaranteed pay-out from annuities |

Non-guaranteed pay-out from annuities |

Returns will differ between insurers and plans. |

Illustrated at 3.25% and 4.75%. Actual returns are dependent on the performance of an insurer's participating fund. |

Is this similar to CPF Life?

CPF Life is also a type of annuity. However, there are several notable differences between CPF Life and private annuities. While CPF Life offers higher returns than private annuities, the tradeoff is the inflexibility of pay-out age, liquidity and lack of option to pay using your SRS.

CPF Life |

Private annuities |

|

Returns |

Higher |

Lower |

Flexibility in pay-out age |

No. Pay-outs will only commence at age 65 and can be deferred to no later than age 70 |

Yes. Pay-outs are determined by you. You will therefore be able to choose when you wish your pay-outs to commence. |

Liquidity |

Capital in your CPF Life cannot be withdrawn. All top-ups to CPF Life are irreversible and irrevocable. |

With a surrender value, private annuities offer the option to cash out should there be an urgent need to raise cash. |

Payment with SRS |

No |

Yes |

You may read more about our comparison between CPF Life and private annuities in our article I Already Have CPF Life, Do I Still Need Annuities?".

Annuities for a regular stream of income

Providing a regular stream of income for life, annuities allow you a hands off approach to your retirement planning. As your guaranteed income from annuities is not subjected to market volatility, this ensures that you will enjoy income certainty in your retirement years.

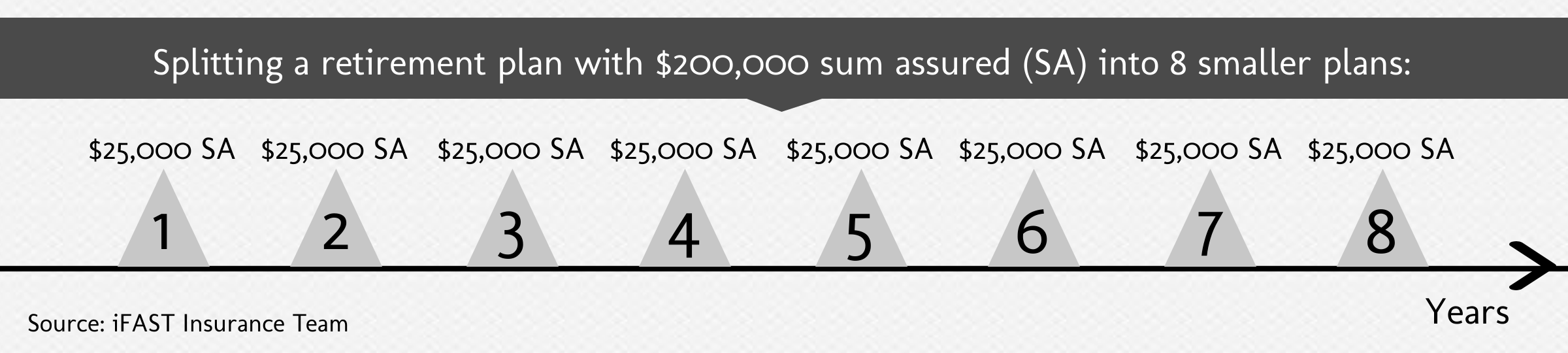

If you are concerned about the high premiums associated with annuities, one tip we have is to purchase multiple smaller annuity plans over a period of time rather than one single annuity with a large sum assured. This will allow you to slowly buy in and build up your nest egg comfortably. As most annuities provide pay-outs on an annual basis, doing so also allows you to schedule the frequency of your pay-outs.

With income certainty and protection by the Policy Owner’s Protection Scheme (PPF Scheme), annuities therefore offer a conservative method for retirement planning.

(See "3 Tips For The Best Retirement Strategy")

Over 9,500 users trust FSMOne with their insurance planning

Live better, safer. Take risks with your investments, not your insurance.

Speak to our experts today to get proper protection.

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Don't Need A Full Critical Illness Plan? Here's Your Alternative

How Much Can I Receive From An Annuity?

Diabetes and Glaucoma – Will Your Insurance Cover This?