The No.1 killer in Singapore: Cancer

Whenever you ask someone to name one critical illness condition, Cancer is often the one that comes to everyone's mind.

According to the latest data published by the Ministry of Health, Cancer accounts for 26.4% of the total deaths in Singapore for the year 20211. Cancer is also the number one killer in Singapore for the past few years.

Cancer treatments are definitely not cheap and often stretches over a long period of time. Many of us choose to purchase insurance so as to defray some of the potential hefty medical bills should one be diagnosed with cancer.

Upcoming outpatient cancer drug treatment changes

Many of us have purchased Integrated Shield Plans (IP) to further enhance our coverage against high medical costs.

Cancer being the number one killer has led to the rise in the cost of cancer treatments. To better sustain the rise in costs, the Ministry of Health (MOH) have announced a newly created Cancer Drug List (CDL).

This new change would mean that usage of MediShield Life and IP to reimburse outpatient cancer drug treatments will be restricted to the drugs included in the CDL only. As of 1 September 2022, more than 90% of cancer drugs that are approved by the Health Science Authority (HSA) are on the list.

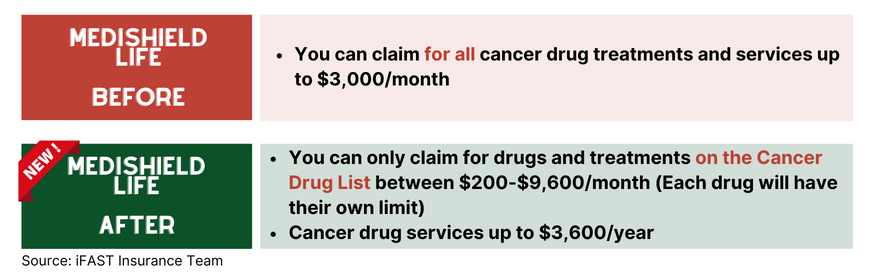

Changes to MediShield Life

For MediShield Life, these changes are already effective from September 2022. There will be separate limits for cancer drug treatments and cancer drug services.

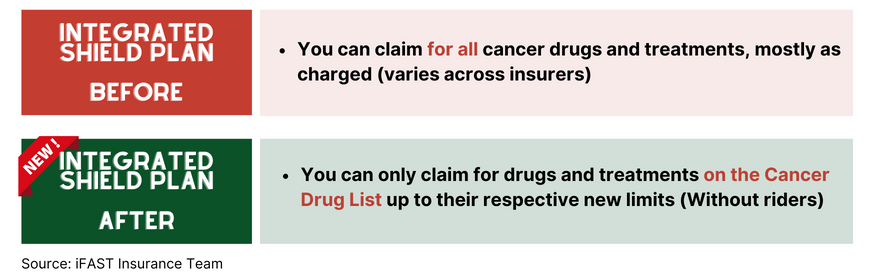

Changes to Integrated Shield Plan (Private Hospital Insurance)

For those with IPs, insurers will no longer be able to provide coverage for drugs and treatments not on the CDL from April 2023 if you do not have additional riders.

How am I affected?

Everyone is affected, even if you are holding on to the highest plan tier your IP insurer can offer you. The worry for everyone now is that what would happen if your treatment goes beyond that of the CDL?

With this new change, what it means is that you may have to fork out the treatment cost at your own expense if you are prescribed with a drug that is not in the CDL.

There is also a possibility that you will require multiple drugs from the CDL in a month. This will mean that you will only be able to claim up to the highest limit between the multiple drugs (not combine limits of the drugs) used since each drug will have their own limits.

The question will then be, should you tell your doctor to not administer a drug just because it is not covered or just stick to one drug?

We strongly do not encourage doing so because seeking treatment should be your upmost priority. Instead, you should check with your doctor whether there is alternative treatment.

The point here is, we should always give ourself assurance against the worst-case scenario. In this case it could be high medical bills at our own expenses.

Introducing iFAST Digital Term

When we first heard about the upcoming change, we immediately reached out to our insurance partner (Raffles Health Insurance) and insisted that our cancer riders must be on a basis where full pay-out is given upon diagnosis.

Furthermore, our product is created with the intention of providing protection coverage. Premiums are kept affordable as there is no investment element in this plan.

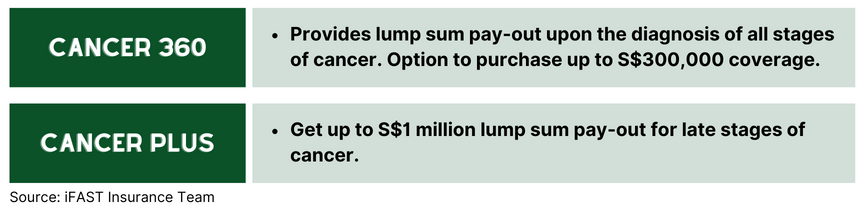

How our Cancer360 rider can help

While your MediShield Life and Integrated Shield plans are meant to reimburse your hospitalisation and/or medical costs, these plans will offer limited coverage for drugs and treatments that are not on MOH's CDL. This is where our Cancer360 rider can help to reassure you as a lump sum pay-out is given in the event of a cancer diagnosis. There are no restrictions on how you may use this Cancer360 pay-out, and your pay-out can be used to help alleviate your cost of drugs and treatments that are not on the CDL.

Our riders are also offered on an additional sum assured basis. This means that whenever our clients make a claim on any one of the cancer riders, it will not reduce the death sum assured of the core plan. Your death coverage remains intact. This way, you will receive a lump sum of money for any treatment cost that might potentially come your way. Our product is designed to provide assurance to our clients at a time when you need it most. We want you to focus on getting treatment rather than worrying about whether or not you can afford the treatment.

You may find more details on our cancer riders below:

When it comes to your personal health being, let's not take a gamble on whether you will be diagnosed. Instead, give yourself the assurance today so that you don't have to worry when you are diagnosed.

Plan early and consider getting a cancer cover to enhance your insurance coverage now!

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

You may also be interested in...

iFAST Digital Term – *NEW* on FSMOne.com

Insurance Rebate Program – Save more when you insure with us

This is why you should Buy Term Invest the Rest (BTIR)

Best Personal Accident Insurance Singapore

Should I switch from Eldershield to CareShield Life?

Source:

1https://www.moh.gov.sg/resources-statistics/singapore-health-facts/principal-causes-of-death

2https://www.moh.gov.sg/news-highlights/details/higher-medishield-life-claim-limit-for-cancer-drug-services