Insurers conduct yearly reviews of their Integrated Shield Plans to ensure that both coverage and premiums remain sustainable and up to date with the medical advancements in the long run. Following the recent changes to MediShield Life that took place from 1 April 2025, Income will also revise their plans with effect from 1 October 2025. These changes will affect both Enhanced IncomeShield and IncomeShield plans. If you have an existing Enhanced IncomeShield or IncomeShield, do note that these changes will only take effect upon policy renewal after 1 October 2025.

Here are the key changes to your Enhanced IncomeShield and IncomeShield plans.

1. New benefits

- Coverage for Mobile Inpatient Care @ Home (MIC@Home)

Mobile Inpatient Care is an alternative to hospital inpatient care and allows clinically-suitable patients the option to recover comfortably at their own homes instead of at a hospital ward. Eligible patients will have their MIC@Home treatment recognised as an inpatient episode with pre- and post-hospitalisation benefits also given.

This coverage for MIC@Home has been included in MediShield Life’s benefit under the normal ward inpatient benefit with effect from 1 April 2024.

From 1 April 2024, Income also included MIC@Home coverage as part of the existing inpatient benefit. Policy conditions for this benefit will officially be updated with effect from 1 October 2025 for Income’s Shield plans.

- New Outpatient benefits for Enhanced Preferred and Advantage plans

To ensure that your Shield plan remains competitive and aligned with your healthcare needs, Income has introduced 7 new outpatient benefits. This will provide up to two times the MediShield Life benefit limits for these seven treatments received at restructured hospitals:

|

New outpatient benefits: |

Policy benefit limits: |

|

Home Ventilation and Respiratory Support Service |

$1,680 each month |

|

Paediatric Home Care |

$840 each month |

|

Negative Pressure Wound Therapy |

$240 each day |

|

Repetitive Transcranial Magnetic Stimulation |

$240 each treatment |

|

Pasteurised Donated Human ilk |

$170 each day |

|

Hyperbaric Oxygen Therapy |

$1,560 each treatment |

|

Outpatient Parenteral Antibiotic Therapy |

$180 each day |

2. Revision of existing benefits

- Inpatient benefit for high-cost drugs for

blood conditions and conditions with childhood onset coverage

In line with MediShield Life’s expansion of coverage (progressively implemented from April 2025) to include cover for these high-cost drugs, Enhanced IncomeShield and IncomeShield plans will now only cover up to MediShield Life’s benefit limits. This is intended to manage policyholder’s premium increases and is part of Income’s claims and cost containment measures.

- Cell Tissue and Gene Therapy Products (CTGTP) benefit

With effect upon new purchases or renewals from 1 October 2025, Income will align with the Ministry of Health (MOH)’s guidelines to only cover treatments specified on MOH’s CTGTP list. The current CTGTP list includes treatment using Kymriah and Yescarta.

While Income previously provided coverage for CTGTP benefit on an “as charged” basis per policy year, the new benefit will only be payable for one treatment per indication per lifetime.

Cell, tissue and gene therapy benefit:

|

Enhanced Preferred |

Enhanced Advantage |

Enhanced Basic |

Enhanced C |

|

|

Current benefit (each policy year) |

As charged, up to $250,000 |

As charged, up to $250,000 |

As charged, up to $150,000 |

As charged, up to $150,000 |

|

With effect from 1 October 2025 (one treatment per indication per lifetime) - Kymriah - Yescarta |

$250,000 |

$250,000 |

$150,000 |

$150,000 |

- Pro-ration factors for Enhanced Advantage and

Enhanced Basic plans

A pro-ration factor applies when you choose to seek treatment at a ward class higher than what your Integrated Shield plan allows you to. In such cases, the pro-ration factor will be applied to adjust the amount claimable. Read our article here to find out more about this pro-ration factor and how this affects you.

Starting 1 October 2025, the pro-ration factor for Enhanced Advantage and Enhanced Basic plans will be reduced. Individuals with these plans will have a smaller portion of their bills covered when receiving treatment in a ward class higher than their entitlement. Individuals who seek treatment within their plan entitlement will not be affected.

|

Benefit |

Enhanced Advantage |

Enhanced Basic |

|

Inpatient treatment at private hospital or private medical institution or emergency overseas treatment |

Decreased from 65% to 50% |

Decreased from 50% to 35% |

|

Day surgery or short-stay ward at private hospital or private medical institution or emergency overseas treatment |

Decreased from 65% to 55% |

Decreased from 50% to 40% |

|

Outpatient hospital treatment at private hospital or private medical institution or emergency overseas treatment |

Decreased from 65% to 45% |

Decreased from 50% to 30% |

|

Inpatient treatment for restructured hospital Class A ward |

Not applicable |

Decreased from 85% to 70% |

- Increase in Annual policy limit

The annual policy limit for Enhanced Advantage plan will increase from $500,000 to $1,000,000 for plans purchased or renewed after 1 October 2025. Policy limit for other plans remains unchanged.

|

|

Enhanced Preferred |

Enhanced Advantage |

Enhanced Basic |

Enhanced C |

|

Current benefit |

$1,500,000 |

$500,000 |

$250,000 |

$150,000 |

|

Revised benefit from 1 October 2025 |

$1,500,000 |

$1,000,000 |

$250,000 |

$150,000 |

This revision puts Income’s Class A ward plan’s annual policy limit on par with other insurers and offers more incentive for individuals to opt for Class A ward plans as this potentially strikes the perfect balance between premiums and coverage.

Integrated Shield plans offering Class A ward cover:

|

Enhanced IncomeShield Advantage |

Raffles Shield A |

Singlife Shield Plan 2 |

AIA Health Shield Gold Max B^

|

GREAT Supreme Health A Plus^ |

HSBC Plan B^ |

PRUShield Plus^ |

|

|

Annual policy limit |

$1,000,000 |

$600,000 |

$1,000,000 |

$1,000,000 |

$1,000,000 |

$1,000,000 |

$1,000,000 |

^FSMOne does not distribute these products. Information retrieved from respective insurer’s websites and is accurate as of 19 August 2025. For illustration purposes only.

3. Premium revision

Income will also be revising the premiums of both the main Integrated Shield Plan (IP) and riders. Premiums for main plans will increase by 4.5% on average, and the increase for main plan with riders will average at 10.8% premium increase. Seniors aged 65 and above, will have their premiums unchanged or increase less with this premium increase averaging at 5.6%.

We have compiled both current and revised premiums in the tables below for easy reference:

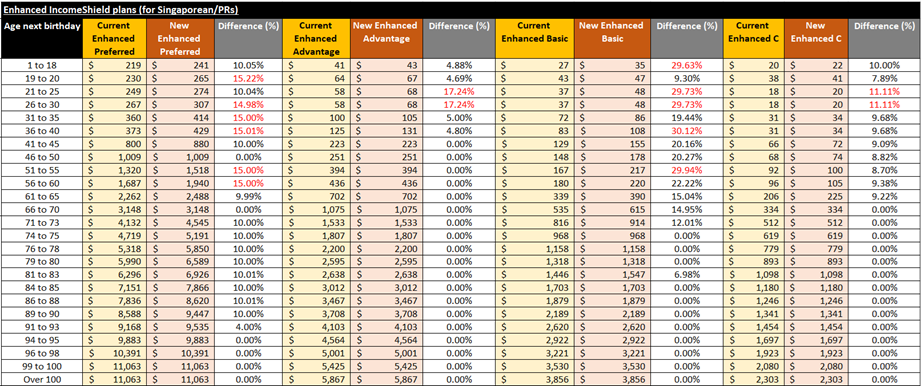

- Main plan: Enhanced Preferred,

Enhanced Advantage, Enhanced Basic, Enhanced C

Enhanced Basic plans experience the highest percentage increase with this averaging at 14.48%. Increase in premiums average at 10.51% for Enhanced Preferred plan and just 2.69% for Enhanced Advantage plans.

Premiums shown are retrieved on 19 August 2025 for policies issued on standard terms and are for illustration purposes only.

Note: While Income has tried to minimise the impact that seniors will face for this premium adjustment, those between the ages of 71 to 90 will still face a 10% increase in premium for Enhanced Preferred plan. Other plans (Enhanced Advantage, Enhanced Basic, Enhanced C) will mostly experience 0% premium increase to main plan for the older age group.

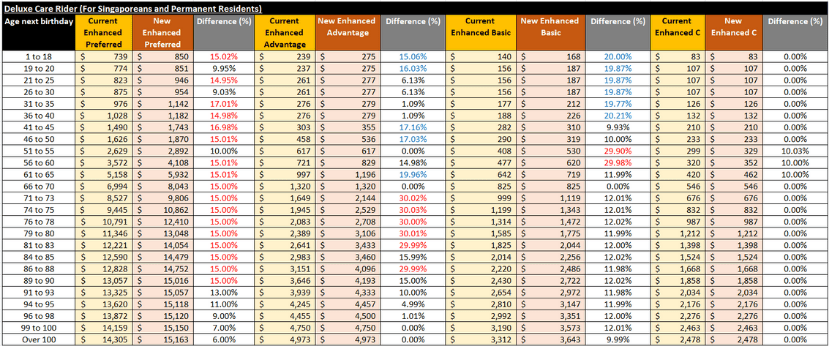

- Deluxe Care rider

Deluxe Care rider faces higher premium increases with this averaging at a 13.95% increase across the Enhanced Preferred, Enhanced Advantage, and Enhanced Basic plans. This increase is exceptionally high when the Deluxe Care Rider is added to Enhanced Advantage plan with the premiums increasing by as much as 30% for individuals aged 71 to 83.

Premiums shown are retrieved on 19 August 2025 for policies issued on standard terms and are for illustration purposes only.

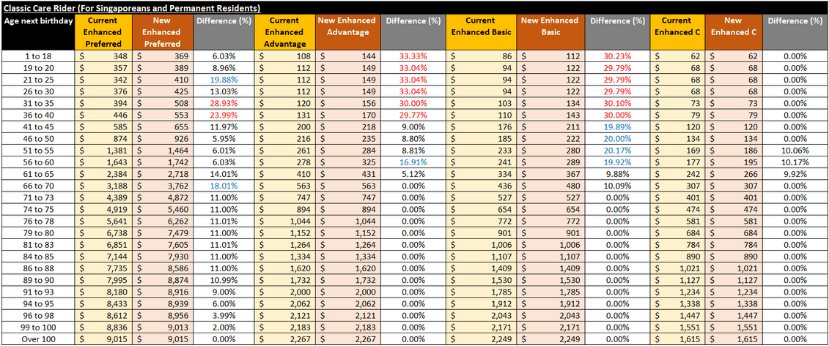

- Classic Care rider

Premiums for the Classic Care rider will see the steepest increases among individuals aged 31 to 40, with this averaging around 30% across the various plans. This premium increase is most significant for (1) those under age 40, and (2) when the rider is added to the Enhanced Preferred plan.

Premiums shown are retrieved on 19 August 2025 for policies issued on standard terms and are for illustration purposes only.

Should I still hold on to my Enhanced IncomeShield plan?

With the recent changes to your Enhanced IncomeShield, you may be wondering if this plan is still suitable for you. Here is our take on the changes and the impact that this may have.

- While premiums may be a consideration when selecting an Integrated Shield plan, this should not be your only consideration, as Integrated Shield plans are yearly renewable, and renewal premiums are not guaranteed. With the insurer’s occasional premium revisions for Integrated Shield plans, there is no guarantee that the lowest-priced plan now will continue to be the lowest-priced plan in future.

- We also do not recommend switching Integrated Shield plan providers solely for the promise of “better” benefits. This is because insurers periodically review and adjust their Integrated Shield plan coverage to keep pace with changes to MediShield Life and medical advancements. This means that a plan offering certain “better” benefits today may not always provide the same advantages in future. Instead, consider what the insurer can offer – for example, the availability of panel doctors, efficiency of claims processing, and the ease of pre-authorisation procedures.

- Lastly, while we do not recommend switching insurers, this is what you can do:

Maintain your current plan if you can afford the premiums. This is because it is easier to downgrade than to upgrade your plan type in future should there be the need to do so. However, if you feel that the recent premium revisions have made your current premiums unaffordable, reach out to us here to let us review your coverage and advice on your next steps.

⚡Did you know? FSMOne has a commission rebate program that allows you to receive up to 45% commission rebate on your insurance purchases! This is also applicable to Integrated Shield Plan purchases! Click here for more information on our commission rebate program.

Read also,

- Should I downgrade my Raffles Shield plan coverage? This is what we think

- Assess your Singlife Shield plan with this one guide

- New MediShield Life and Integrated Shield plans. Here is what has changed.

- I have life and health insurance. Am I well covered?

- Simplifying Singapore’s hospital insurance – All about MediShield Life and Integrated Shield plans

- MediShield Life is not for private hospital bills. Here’s why.

|

Available Products on FSMOne Insurance |

|

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Information

obtained from:

https://www.moht.com.sg/our-programmes/integrated-general-hospital/mic-home

https://www.income.com.sg/media/Income/Orphan/1-September-2024-benefit-changes-and-premium-revision-FAQs.pdf

https://www.moh.gov.sg/managing-expenses/schemes-and-subsidies/medishield-life/medishield-life-benefits#Cancer-Drug-List

https://www.moh.gov.sg/managing-expenses/schemes-and-subsidies/cell-tissue-and-gene-therapy/product-list-cell-tissue-gene

https://www.income.com.sg/kcassets/48ba2802-266a-4bec-b7cb-b61bff0e0f7c/Final%20Enhanced%20IncomeShield%20policy%20conditions%201%20Nov%202024.pdf

https://www.greateasternlife.com/content/dam/corp-site/great-eastern/sg/gels-ftrp-imc-cm/health-insurance-/great-supremehealth/gels-pdt-pd-gsh-gtc-benefit-and-premium-tables-eng.pdf

https://www.aia.com.sg/en/our-products/health/medical-insurance/aia-healthshield-gold-max

https://www.insurance.hsbc.com.sg/content/dam/hsbc/insn/documents/health/hsbc-life-shield-brochure.pdf

https://www.prudential.com.sg/-/media/project/prudential/pdf/ebrochures/prushield/prushield-ebrochure-english.pdf

https://singlife.com/content/dam/public/sg/documents/medical-insurance/singlife-shield/singlife-shield-policy-contract-2025.pdf

https://www.raffleshealthinsurance.com/wp-content/uploads/2024/04/Raffles-Shield-Product-Summary-1-April-2024.pdf

Information

retrieved on 19 August 2025.

Disclaimer:

All

materials and content found in this article are strictly for information

purposes only and should not be considered as an offer or solicitation to

transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice. More information on iFAST Digital Term can be found here: https://secure.fundsupermart.com/fsmone/insurance/ifast-digital-term.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.