A brief recap on MediShield Life and the Integrated Shield (IP) plans offered by Raffles Health Insurance.

In this article, we study the different Raffles Shield plans and riders to determine if you should pay for the highest-tiered Private plan, and share alternatives to get private hospital coverage at lower premiums.

Raffles Shield Private |

Raffles Shield A |

Raffles Shield B |

MediShield Life (MSHL) |

|

Ward entitlement |

Private hospital |

Class A wards in public hospital |

Class B1 wards in public hospital |

Class B2/C wards in public hospitals |

Annual policy limit |

Up to $1,500,000 |

Up to $600,000 |

Up to $300,000 |

$150,000 |

What do the different hospital ward classes mean:

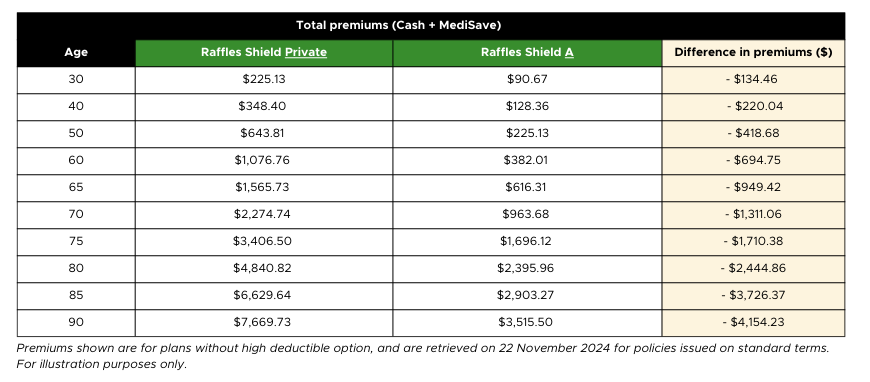

#1 Difference in benefits between Raffles Shield Private and Raffles Shield A

Is there really a significant difference in coverage and benefits between Raffles Shield Private and Shield A plans? Here are the five main differences between the two plans.

[💡 If you do not plan to visit panel providers for treatment then the annual limit for Shield A and Private plans are actually the same at $600,000 per policy year. List of panel providers for Raffles Shield can be found here.]

Differences between Raffles Shield Private and Raffles Shield A |

Similarities between Raffles Shield Private and Raffles Shield A |

List of differences and similarities are for illustration purposes only. Please refer to your policy wording for more information. Information retrieved on 22 November 2024.

#2 Do I need riders for my Raffles Shield plan?

Integrated Shield plan riders are intended to enhance your hospitalisation coverage by offering additional benefits. The three IP riders available for Raffles Shield plans are:

The addition of Key Rider will reduce the co-payment needed from 10% to 5%. This will also be capped at $3,000 per policy year for pre-authorised treatment under the extended panel. Note that there will be no cap on co-payment for treatments that are not pre-authorised.

Key Rider will also remove the annual deductible required, and offer additional benefit for Cancer Drug Treatments that are not on the Cancer Drug List (CDL).

The addition of Premier Rider will increase your monthly Cancer Drug Treatments on the CDL limits to 2 times the MediShield Life (MSHL) limit. Non-CDL Cancer Drug Treatments will also have a $20,000 annual limit for drug classes A to E.

Premier Rider will also offer additional benefits such as immediate family accommodation, post-hospitalisation follow-up Traditional Chinese Medicine (TCM) treatment, post-hospitalisation home care, emergency outpatient due to accident, and ambulance services.

[💡 Post-Hospitalisation Follow-Up TCM Treatment for Raffles Premier rider includes Physician’s consultations, herbal medication, acupressure, acupuncture, cupping and moxibustion. Benefit is given if treatment is done within 180 days at TCM clinics at Raffles Hospitals or Government Restructured Hospitals only. There is no per visit cap for this benefit.]

Cancer coverage with MediShield Life (MSHL) is limited to $200 - $9,600 per month for drugs on the Cancer Drug List (CDL). Cancer drug services claims are also limited to $3,600 per annum with no coverage given for non-CDL treatments.

Raffles Cancer Guard Rider enhances this coverage by offering up to 18 times the MSHL limit for Cancer Drug Treatments on the CDL. This allows you to get up to 23 times the MSHL limit when you add Raffles Cancer Guard Rider and Premier Rider to your Raffles Shield Private or Shield A + Raffles Hospital Option plan.

You will also receive up to $250,000 per year for non-CDL Cancer Drug Treatments with the addition of Raffles Cancer Guard Rider.

MediShield Life (MSHL) |

Raffles Shield Private |

Premier Rider attached to Raffles Shield Private |

Raffles Cancer Guard Rider attached to Raffles Shield Private |

|

Cancer Drug Treatment on the CDL (monthly limit) for one primary cancer |

$200 - $9,600 per month depending on cancer drug treatment |

5x MSHL limit |

2x MSHL limit in addition to base plan limit |

18x MSHL limit in addition to base plan limit |

Cancer Drug Treatment not on the CDL (annual limit) |

No coverage provided. |

No coverage provided. |

$20,000 annual limit for Drug Classes A to E. |

$250,000 annual limit for Drug Classes A to E. |

Cancer Drug Services (Annual Limit) |

$3,600 per year for Cancer drug services. |

5x MSHL limit |

2x MSHL limit in addition to base plan limit |

15x MSHL limit in addition to base plan limit |

How can I get private hospital coverage at lower premiums?

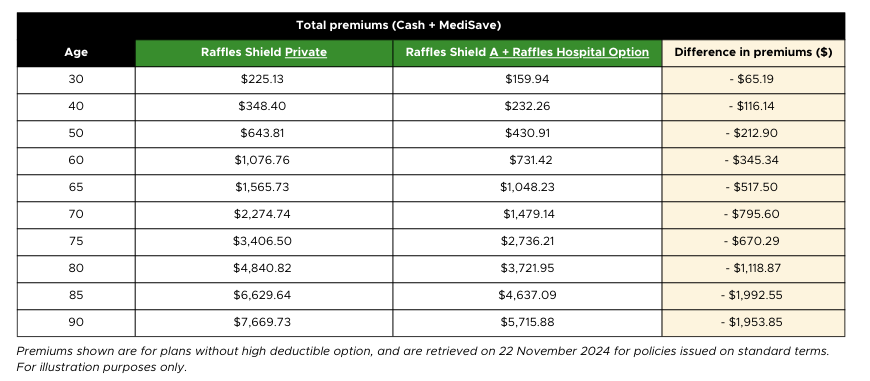

Want access to private hospitals but at a lower cost? If you are comfortable with the idea of only seeking treatment at Raffles Hospital and public hospitals, then downgrade from Raffles Shield Private plan to Shield A and add the Raffles Hospital Option. By doing so, you will still have access to private hospital facilities at Raffles Hospital but will pay less premiums as compared to a Shield Private plan. (Note that medical underwriting may be required for the addition of Raffles Hospital Option.)

Premiums for Raffles Shield Private vs Raffles Shield A + Raffles Hospital Option

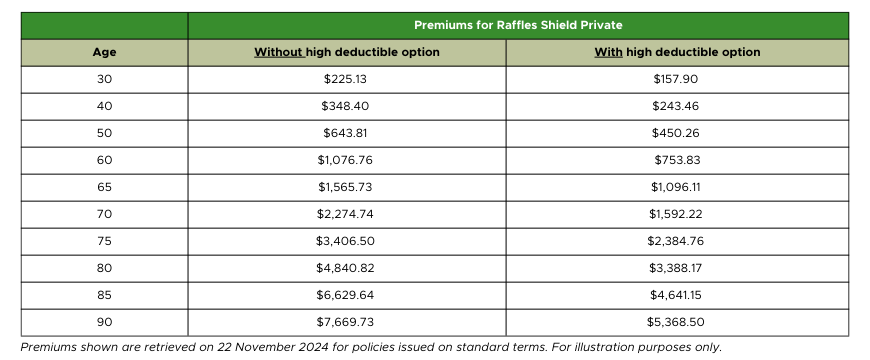

If you want coverage for all Private Hospitals, and do not want to be limited to Raffles Hospital or public hospitals only, then add the high deductible option to your Raffles Shield plan. This will increase your deductible to $10,000 per policy year for all ward types and ages, in exchange for 30% cheaper premiums.

Premiums for Raffles Shield Private without high deductible option vs Raffles Shield Private with high deductible option

Do note that you will not be able to add the High Deductible option if you have Key Rider added to your Raffles Shield plan.

Have a question? Speak to us about your shield plans here:

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Read also,

Information obtained from:

https://www.moh.gov.sg/managing-expenses/schemes-and-subsidies/medishield-life/medishield-life-benefits#Cancer-Drug-List

https://www.raffleshealthinsurance.com/products/raffles-shield/learn-more/raffles-shield-plans/

https://www.raffleshealthinsurance.com/wp-content/uploads/2021/03/Raffles-Shield-Product-Summary-1-April-2024-Finalv1-1.pdf

https://www.raffleshealthinsurance.com/products/raffles-shield/learn-more/raffles-cancer-guard/

Information retrieved on 22 November 2024.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to review the specific terms, conditions and exclusions in the relevant policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

While iFAST and its third-party providers strive to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

Purchasing a life insurance policy is a long-term commitment, and early termination may involve significant costs. The surrender value, if any, may be zero or less than the total premiums paid.

This advertisement has not been reviewed by the Monetary Authority of Singapore.