We often look for alternative products so that our excess cash can grow at a better rate. If you ever tried looking for wealth accumulation products, you will most definitely come across “Insurance Savings Plans.” However, there have been cases where policyholders regret their purchases after finding out that the actual returns do not meet their expectations. So how can we better equip ourselves to make a decision on whether or not the returns of such products are indeed what we are looking for?

Endowment and Annuities

There is a good chance that the product you found or are being recommended is either an Endowment or Annuity. But what is the difference?

Endowment |

Offers you a lump sum pay-out at maturity date |

Annuity |

Offers you a monthly pay-out at a pre-determined age and for a pre-determined period |

Both Endowment and Annuity are participating products. For policyholders of participating products, a portion of the premiums you pay will be invested into the insurer’s participating fund. This also means that policyholders will be given non-guaranteed bonuses when it is declared by the insurer and this will be added into the policy cash value.

Death Benefit Table

One has to be clear that even though such products are designed to focus on wealth accumulation, these products will still contain an element of insurance. Thus, a portion of your premiums will still go towards paying for mortality charges in return for a death benefit.

Surrender Value Table

When we purchase an Endowment or Annuity, it is because we hope to achieve a better rate of return on our money and not for its death benefit. After scrolling pass the death benefit table, you will arrive at a table called “Surrender Value”. This is the table that you should be focusing on.

Under this table, there are two columns: Guaranteed and Non-Guaranteed. Your final maturity value will consist of both Guaranteed and Non-Guaranteed portions. The values that will not be affected by the performance of the participating fund will be the Guaranteed column.

For the Non-Guaranteed column, you will find two columns containing illustrated values at 3.00% and 4.25%. Do note that these values are only for illustrative purposes to allow policyholders a perspective of what the maturity value may look like and should not be taken as a definitive maturity value.

In short, the only values that are guaranteed is the guaranteed column. Other values are illustrative and are dependent on the performances of the insurer’s participating fund.

How do I know what kind of assets the participating fund invests in?

Insurers will provide a breakdown of their asset allocation of the participating fund in your policy illustration.

Common asset classes that participating funds invest in are: Fixed Income, Public Equity, Private Equity, etc. You should refer to your own policy illustration as asset classes and allocation may differ across insurers.

Where can I find the performance of the participating fund?

You can usually find this information on the first few pages of your policy illustration. Insurers will also provide historical investment rate of returns of the participating fund. However, do note that these are historical performances and should not be treated as future performances.

If the participating fund performs at 10%, does it mean I will receive 10% in bonuses?

Returns on participating fund are smoothed so that policyholders may receive consistent returns. This means that in a good performing year for the fund, insurer may keep the surplus. The insurer will then tap into such surplus to distribute bonuses to policyholders in years when the fund underperforms.

So how do I determine if the rate of return aligns with my expectation?

In your policy illustration, you will find the projected rate of return under the surrender value table. Below is an example of the text:

“Based on the Illustrated Investment Rate of Return of the Life Participating Fund:

At 4.25% p.a., your total Illustrated Yield at maturity is 3.00% p.a.

At 3.00% p.a., your total Illustrated Yield at maturity is 1.50% p.a”

These values will serve as an indication to policyholders. From the above example, if the participating fund performs consistently at 3.00% p.a. Your overall returns will work out to be 1.5% p.a. at policy maturity.

Are there products that provide me with only guaranteed returns at maturity?

As you can see, the usual Endowments and Annuity products in the market contains both Guaranteed and Non-Guaranteed returns. However, some insurers may offer products that provides only guaranteed returns to policy holders and are often only available for a short period of time.

Should I keep protection and investment separated?

We would recommend keeping protection and wealth accumulation separated. This is mainly because when client invest in a participating product, they will not be entitled to 100% of the investment returns of the participating fund due to the effect of bonus smoothening.

Furthermore, such product requires clients to stay committed to a longer term as any early termination will most likely result in client not being able to receive 100% of their premiums back.

Lastly when it comes to protection, there are cheaper options in the market for protection focused product like a Term Life insurance that will be able to offer a higher sum assured at a lower price.

We do acknowledge that products like Endowments and Annuity are still alternatives for clients that are risk-averse. But clients must be aware that they will have to stay committed to a long period of time.

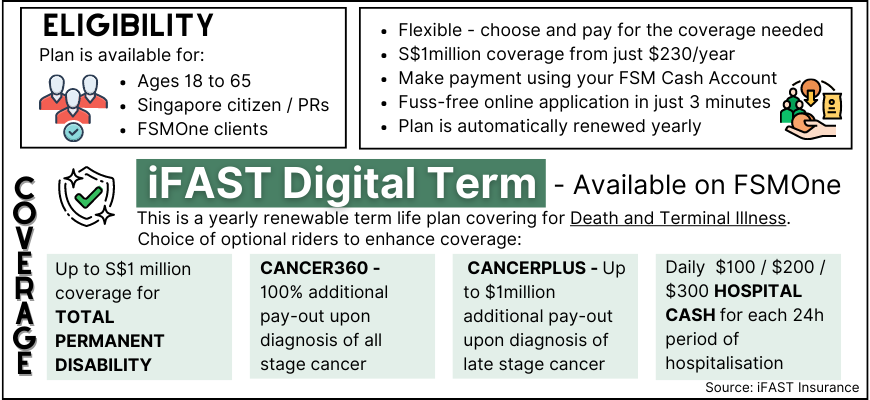

Look for affordable product that focus just on protection

If you decide to focus on getting insurance products just for protection, we recommend iFAST Digital Term. Our product is design to be simple and affordable so that clients will not need to spend a majority of their cash flow just for insurance. More information on our product can be found below:

And enjoy up to 45% commission rebates!

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

iFAST Digital Term – *NEW* on FSMOne

I cannot buy MINDEF's Group Insurance. What are my other options?

Can I rely on my MediShield Life or Integrated Shield plan for Cancer Coverage?

Will the New Cancer Drug Change Affect Me?