1. Sum Assured

Sum Assured is the amount that you choose to be covered for. For example, if you purchase a term life plan with a sum assured of $1 million, you will be covered for $1 million. This pay-out will be given in the event that you fulfil the conditions of the policy.

2. Policy Owner

Policy owner refers to the individual who owns the policy. This can both be the same individual as the life insured or a different individual.

3. Rider

Riders are optional add-ons to your life insurance policy that can help to enhance your policy’s coverage. There are 2 types of riders:

- Accelerator: This rider accelerates the benefit from your main plan.

- Additional: Benefits are given in addition to the benefit from your main plan.

For example, you have $500,000 coverage from your main plan and a $300,000 TPD rider. If you claim $300,000 from your TPD rider, you would then be left with $200,000 coverage from your main plan.

For example, you have $500,000 coverage from your main plan and a $300,000 TPD rider. After claiming $300,000 from your TPD rider, you would still have $500,000 coverage from your main plan as the rider benefit is given on an additional basis.

Main plan coverage |

Coverage from rider |

Total Coverage before a claim |

Amount claimed |

Remaining coverage after claim |

|

Accelerator rider |

$1,000,000 |

$300,000 |

$1,000,000 |

$300,000 |

$1,000,000 - $300,000 = $700,000 |

Additional rider |

$1,000,000 |

$300,000 |

$1,300,000 |

$300,000 |

$1,300,000 - $300,000 = $1,000,000 |

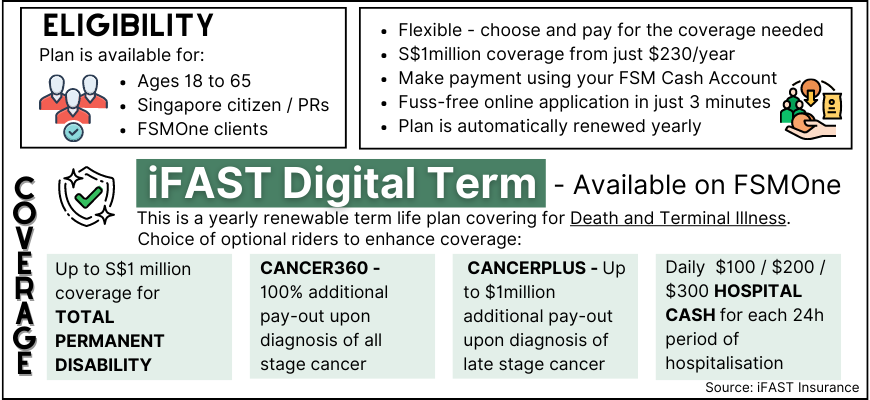

💡 Did you know? iFAST Digital Term offers additional riders for cancer coverage. Click here to find out more. |

4. Total Permanent Disability (TPD)

Total Permanent Disability (TPD) is a coverage that is usually added on as a rider onto your life insurance plan. TPD rider will provide a pay-out when an individual is found to be permanently disabled with no chance of recovery.

Note: This is not the same as disability coverage from your CareShield or ElderShield insurance.

(See: "Should I switch from Eldershield to CareShield Life?")

5. Hospital Cash

Hospital Cash is a benefit that provides daily cash benefits for each day that you are hospitalised. This is given in addition to any existing medical benefits and is meant to offer income replacement during the period when you are hospitalised.

💡 Did you know? Integrated Shield plan riders no longer offer a daily cash as one of its benefits. If you are interested in receiving this hospital cash benefit, you may consider iFAST Digital Term's hospital cash rider. |

6. Policy Term

Policy term refers to the duration of which your policy is in-force for, and the period for which you are covered. Term insurance usually have specified policy terms. This can range from one year (for yearly renewable plans) or for coverage of up to a maximum of age 100.

7. Level Term

Level term refers to a term insurance plan that provides coverage for a specified period of time. This may be for up to a specific age or for a fixed period.

For these plans, your premiums are locked in upon the purchase of the plan. This means that you will pay the same amount of premiums for the entire duration of your plan. However, do note that the upfront premiums may be higher as compared to a renewable plan.

8. Renewable Term

Renewable term refers to a term insurance plan with a shorter coverage term. Coverage period ranges from 1, 5 or 10 years and are automatically renewed at the end of each policy term. Changes to your health condition after the purchase of a renewable term will not affect your coverage.

Renewable term plans tend to start with lower upfront premiums making the entry point for such plans much more affordable. However, do note that future premiums are not guaranteed.

iFAST Digital Term |

TM Term Assure 2 |

|

Type |

Renewable Term |

Level Term |

Coverage period |

Renewable yearly |

30 year period |

Coverage amount |

Covers for $200,000 death, and total permanent disability (TPD) |

|

First year premiums* |

$54 / year^ |

$239 / year |

Lifetime premiums* |

$6,596 |

$7,170 |

*Profile: Age 30, non-smoker female for 30 year coverage. (Coverage period: Age 30 to 60)

^Premiums start low and changes yearly, with renewal premium based on life assured’s attained age.

9. Loading / Exclusions

Loading in insurance refers to an extra charge being added to your premiums. This loading is based on your level of risk. An example of this would be the insurer loading the premiums of your insurance policy due to your health conditions as the insurer deems you to be of a higher risk. In some cases, underwriters may decide to exclude certain conditions that you may have declared during the application instead of imposing a loading.

10. Medical underwriting

Insurers will require you to declare your health condition during the application process. If you have any pre-existing health conditions, the insurer may require you to undergo a medical check-up before they insure you.

💡 Did you know? iFAST Digital Term only requires you to answer 3 health questions to purchase your coverage. Click here for a free online quotation. |

And enjoy up to 45% commission rebates!

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

Can I rely on my MediShield Life or Integrated Shield plan for Cancer Coverage?

Home Insurance for Home Owners Singapore 2022

I cannot buy MINDEF's Group Insurance. What are my other options?