Insurers are gradually starting to offer simple life insurance products online for clients to purchase themselves. But how do you calculate the amount of coverage you need without an advisor assisting you? There are no right or wrong answers, some advisor may advise you to do the calculation this way while an online article may recommend another method.

But one thing for certain, you should not put off making a decision to review your life insurance just because you do not have the time for it or you cannot come to a conclusion for the calculation.

Imagine the scenario whereby you are taken out of the picture completely. It can be a tremendous amount of financial burden on your spouse to take care of the family. Some might even be forced to change their lifestyle or child future educational plans.

In this article we would like to share a simple method on how you are able to derive the amount of life coverage you need just by doing a few simple calculations.

What is a protection gap?

A protection gap is a measure of the lack of protection against events that might cause financial detriments.

You can easily calculate this as the difference between your current insurance resources available against your current insurance needs.

Once you are able to identify your protection gap, it will give you a clear idea on whether you require additional insurance coverages. This also allows you to determine whether you are over or under-insure.

Insurance needs

There are a few items that will require immediate financial attention in the event of an unfortunate demise.

Do note that the items listed below might not be applicable to everyone.

After paying for the hospital medical expenses if any, the first expenses that comes immediately after death will be funeral costs.

Loans does not get waived off after death. Any existing loans can potentially become financial burden for your loved ones. Thus, it is recommended that your life coverage is sufficient to offset any existing debts.

A good way to calculate this will be to estimate the annual expenses needed per child and multiply it by the remaining years until the child reaches age 21. Example of expenses can be educational fees, insurance premiums and monthly living expenses etc. If there are plans in place for your child to study aboard, you should also take into account the expected fees and expenses involved.

This is to take into account any possible expenses in relation to your surviving spouse. These expenses can include e.g., utility bills of the household or even potential domestic helper expenses.

You may also include any other expenses that you need to consider that are not listed above.

Insurance coverage available

Firstly, you would have to identify the type of insurance product you have to accurately determine the amount of existing coverages you have currently. You will be able to find out the product type under page one of your benefit illustrations.

In general, there are 3 common types of life insurance products:

1. Non-participating policy

Policyholders of such products will not be entitled to any form of profits that the insurer makes as majority of the premiums are often only for the cost of insurance.

As such these products often come at a lower premium cost as compared to participating products for the same coverage level. You can identify your projected death benefit in the death benefit table of the benefit illustrations.

Examples of such products are: Term Life policies.

2. Participating policy

When you purchase a participating policy, your premiums are actually pooled together with the premiums of other policyholders into a common fund. Which is better known as the insurer participating fund. As such, policyholders are entitled to bonuses declared by the insurer.

In order to determine the death benefit, you should refer to either your death benefit or the surrender/account value. Often such products will determine the amount to be the higher of either the death benefit or surrender/account value in the event of death. Examples of such products are: Wholelife, Endowment, Annuity.

3. Investment-linked (ILP)

The difference between a participating policy and an investment linked policy is that policyholders of an ILP will have the full flexibility to choose which funds they wish to invest into. But there will not be any form of guaranteed benefits. Similarly, the death benefit can be the higher of either the death benefit or surrender/account value.

Determining your protection gap

Apart from your existing insurance coverages, you can also include any assets that you have (Savings, investments or any other assets) for this calculation.

Once you have calculated the figures for both your insurance needs and available insurance coverage. You can then determine whether you are having sufficient coverage.

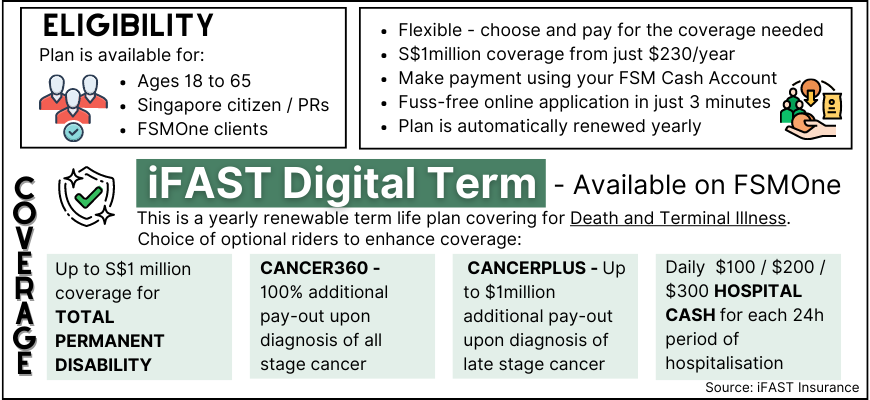

iFAST Digital Term

If you have uncovered that you have an existing insurance gap, we do recommend getting iFAST Digital Term to cover any shortfall you might have. Our product is a Term Life insurance which also means that it is a non-participating product with no additional cost for investment element. Such products are best suited for clients that are looking just for protection.

The application process is online and you will have the flexibility to add on riders to compliment your coverage without the need to meet up with any advisors. More information on our product can be found below:

And enjoy up to 45% commission rebates!

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

Interested to learn more? Check out these articles:

iFAST Digital Term – *NEW* on FSMOne

I cannot buy MINDEF's Group Insurance. What are my other options?

Can I rely on my MediShield Life or Integrated Shield plan for Cancer Coverage?

Our Rebate Program – Save more when you insure with us