- We feature 45 funds for the 2024/25 edition of our Fundsupermart Recommended Funds List. Out of which, 32 of them are equity strategies.

- Our recommended fund for US equities has been changed to the JPMorgan Funds - America Equity A (acc) USD.

- We moved China from the “Core Equity” to the “Supplementary Equity” section of our list, and our new recommended fund is the Fidelity China Focus A-SGD.

- With the growing importance of digital technologies, we added the Eastspring Investments Unit Trusts - Global Technology SGD into the “Digital Economy” category, along with the existing Fidelity Global Technology A-ACC-USD.

- This year’s list features the JPMorgan Funds - Korea Equity A (acc) USD as we believe that South Korea has what it takes to become a new Asian Tiger.

It’s that exciting time of the year again – our annual update of the Fundsupermart Recommended Funds List is here!

Our research team has been publishing the list since 2001 to help investors make informed investment decisions. As the range of available funds continues to expand, our goal is to simplify your investment journey and offer a solid starting point for building a well-diversified portfolio. We update the list annually to ensure that our recommendations stay current and relevant.

As usual, this year’s list spans across equity and fixed income asset classes, covering global, regional, single market, and sector-focused strategies. For the 2024/25 edition, we included 45 recommended funds that have demonstrated their ability to deliver strong and consistent risk-adjusted returns relative to their peers.

In this article, we highlight the changes made to the equity section of our list.

Recommended equity funds

Within the 45 recommended funds featured this year, 32 of them are equity strategies.

2023 was a year of recovery for global equity markets, with the US economy showing resilience and proving less sensitive to higher interest rates. Furthermore, equities began this year on a strong note, with indices like the S&P 500 and Nikkei 225 hitting fresh all-time highs.

However, the rally has recently faltered. A second rate hike from the Bank of Japan (BOJ) sparked a yen rally, triggering a rapid unwinding of carry trades that shook global markets. Concerns surrounding a potential AI bubble and slower US economic growth have also surfaced.

In our view, the recent selloff is driven more by sentiment rather than any material changes in economic and corporate fundamentals. While market volatility may remain elevated in the short term, we view this as a source of opportunity and recommend investors stay the course.

Importantly, we believe the funds we have selected are capable of navigating uncertain times, and ultimately deliver superior risk-adjusted returns over the long term.

Table 1: Recommended equity funds

|

Core Equity |

|

|

Category |

2024 |

|

Asia ex Japan |

|

|

Digital Economy |

|

|

Europe |

|

|

Global |

JPMorgan Investment Funds - Global Select Equity A (acc) USD |

|

Global Emerging Markets |

|

|

Japan |

|

|

US |

|

|

Supplementary Equity |

|

|

Category |

2024 |

|

ASEAN |

|

|

Asia Pacific Property |

|

|

China |

|

|

China-Local |

|

|

Global Financials |

|

|

Global Healthcare |

|

|

Global Infrastructure |

|

|

Global Property |

|

|

Global Resources |

|

|

Greater China |

|

|

India |

RAMS Investment Unit Trust - India Equities Portfolio II A USD |

|

Indonesia |

|

|

Latin America |

|

|

Malaysia |

|

|

Singapore |

|

|

South Korea |

|

|

Thailand |

|

|

Source: iFAST Compilations |

|

(Related article: Market Outlook: Here’s why it’s time to buy during market selloffs)

Notable changes in this year’s list

Core Equity – US: JPMorgan Funds - America Equity A (acc) USD

The first notable change in the 2024/25 edition of the list is our recommended fund for US equities. We believe US equities should be a staple feature of every investor’s portfolio. The US is home to a large number of high-quality companies, mostly global industry leaders with sustainable competitive advantages that will allow them to stay ahead of the competition.

Our new recommended fund is the JPMorgan Funds - America Equity A (acc) USD. The fund is one of JPMorgan’s oldest, having been launched in 1988. Benchmarked against the S&P 500 Index (Total Return Net of 30% withholding tax), it combines elements of both value and growth investing to create a concentrated portfolio of US equities that can outperform in various market cycles.

As of 30 June 2024, the fund holds a total of 40 stocks, with the top 10 making up about 40% of the portfolio. The largest sector is information technology, at 27.6% of the portfolio. Several big tech companies are featured among its largest holdings, such as the likes of Microsoft, NVIDIA and Amazon (Table 2).

Table 2: Top 10 holdings of the JPMorgan America Equity Fund

|

Company |

Sector |

Weight |

|

Microsoft |

Technology |

7.8% |

|

NVIDIA |

Technology |

6.9% |

|

Amazon |

Consumer Discretionary |

5.9% |

|

Meta |

Communication Services |

4.9% |

|

Apple |

Technology |

2.9% |

|

EOG Resources |

Energy |

2.9% |

|

Regeneron |

Healthcare |

2.8% |

|

Berkshire Hathaway |

Financials |

2.8% |

|

Broadcom |

Technology |

2.8% |

|

Kinder Morgan |

Energy |

2.8% |

|

Total |

42.5% |

|

|

Source: JPMorgan, iFAST Compilations Data as of 30 June 2024 |

||

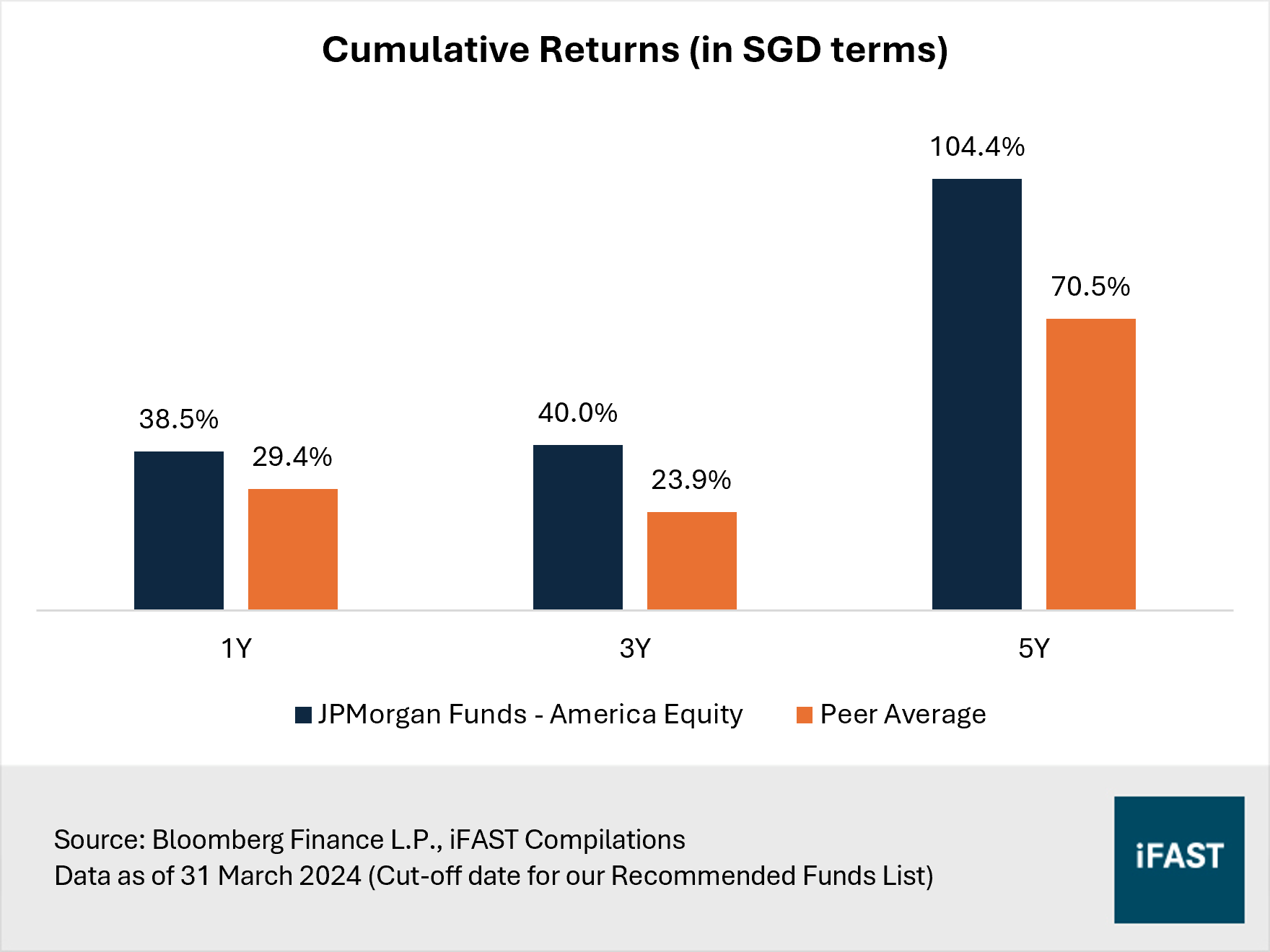

One of the reasons why we favour this fund is because of its solid long-term performance track record. On a cumulative basis, it managed to deliver returns of 38.5%, 40.0%, and 104.4% over the past one, three, and five years respectively, significantly outperforming its peer group (Figure 1).

The fund has also scored well in terms of risk management, with a maximum drawdown of -34.5% over a five-year period, versus the peer average of -36.3%. This is likely attributable to the fund’s strong emphasis on selecting quality stocks and robust risk controls.

Figure 1: The JPMorgan Funds - America Equity has significantly outperformed peers

Supplementary Equity – China: Fidelity China Focus A-SGD

Given the long-term structural challenges in the Chinese economy, we believe China should not form a core component of investors’ portfolios. Instead, China should be treated as a tactical position, offering potential opportunities from valuation gaps but require frequent monitoring due to higher risks.

As a result, we moved China and Greater China from the “Core Equity” to the “Supplementary Equity” section of our list. Our recommendation for Greater China, FSSA Regional China A Acc SGD, remains unchanged. But for Chinese equities, we have selected a new fund: the Fidelity China Focus A-SGD.

The Fidelity China Focus Fund aims to generate alpha mainly through stock selection, with a value-quality tilt and a bias towards mid to large-cap stocks. It prioritises companies with strong business models and cashflows, as they tend to offer investors better risk-adjusted returns.

The fund’s top sector allocations are consumer discretionary and financials, accounting for 25.5% and 15.1% of the portfolio respectively as of 30 June 2024. Notable holdings include tech giants like Tencent and Alibaba, alongside major banks like China Construction Bank and ICBC (Table 3).

Table 3: Top 10 holdings of the Fidelity China Focus Fund

|

Company |

Sector |

Weight |

|

Tencent |

Communication Services |

6.9% |

|

Alibaba |

Consumer Discretionary |

6.8% |

|

China Construction Bank |

Financials |

4.5% |

|

ICBC |

Financials |

4.5% |

|

China Merchants Bank |

Financials |

3.9% |

|

BOC Aviation |

Industrials |

3.4% |

|

Prosus |

Consumer Discretionary |

3.1% |

|

ENN Energy |

Utilities |

2.9% |

|

China Mengniu Dairy |

Consumer Staples |

2.9% |

|

China Oilfield Services |

Energy |

2.9% |

|

Total |

41.8% |

|

|

Source: Fidelity International, iFAST Compilations Data as of 30 June 2024 |

||

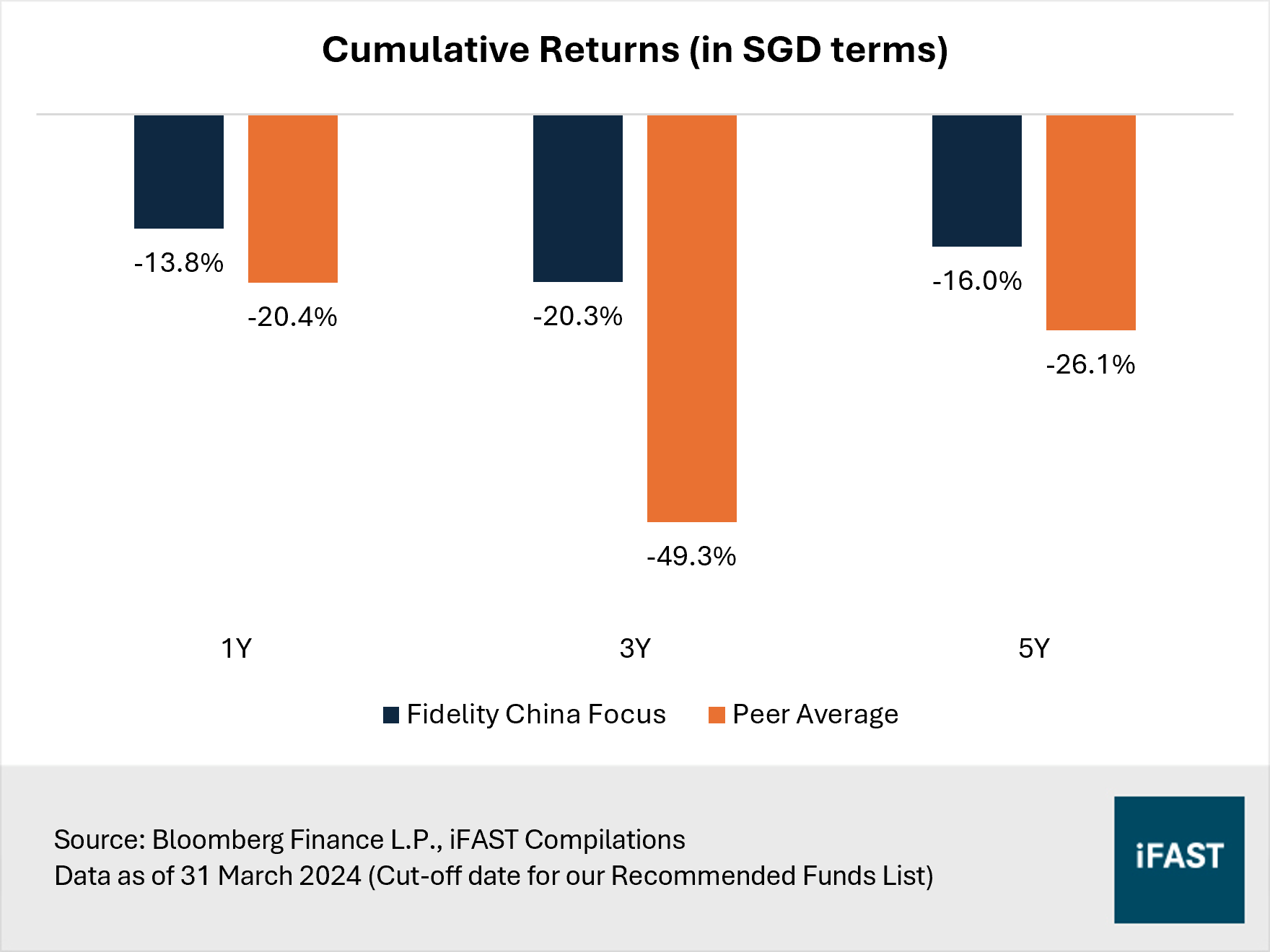

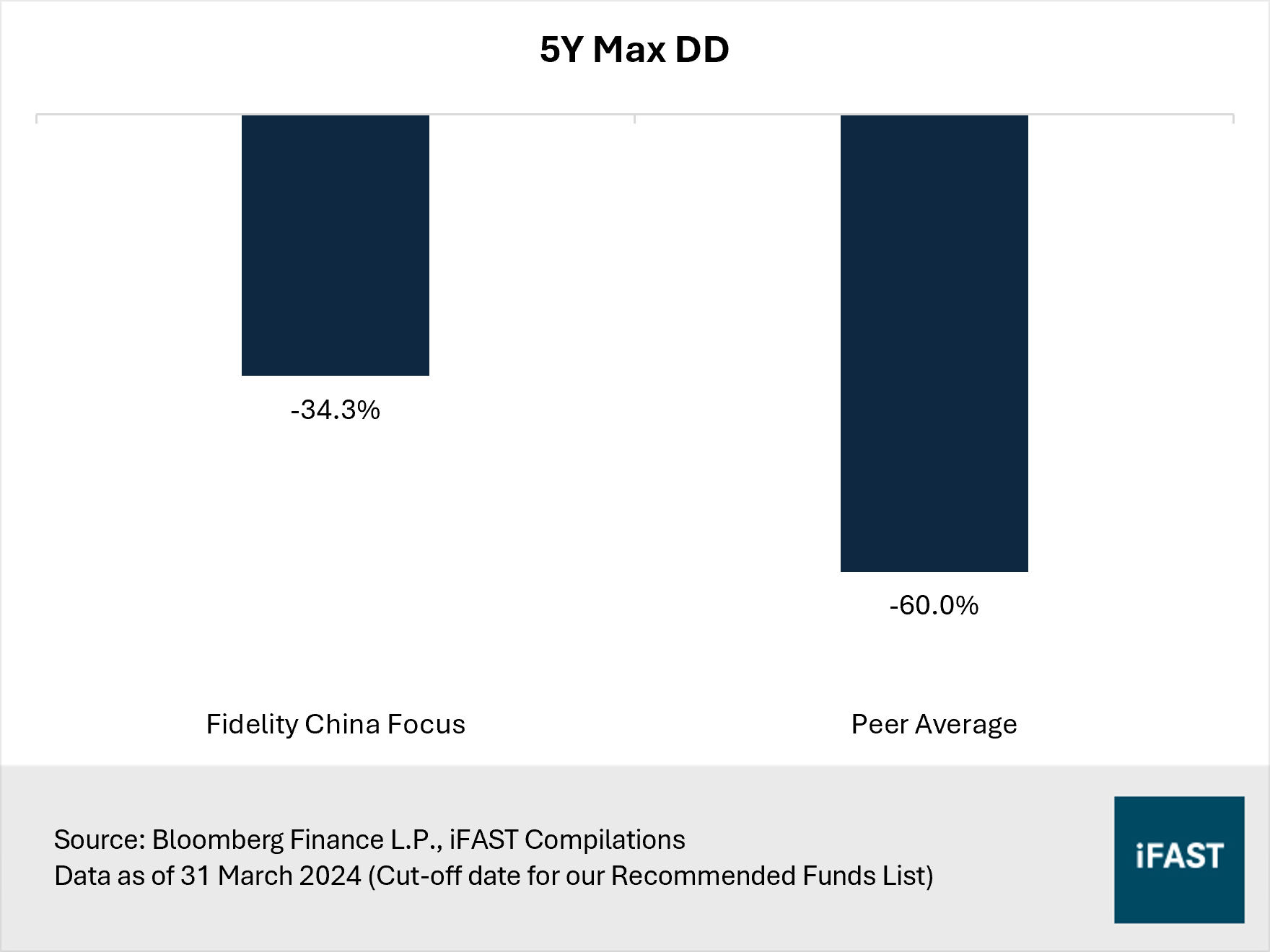

As compared to its peers, the fund has delivered significantly lower losses over one-year, three-year, and five-year periods (Figure 2). Furthermore, its maximum drawdown is roughly half that of its peers, showcasing its superior resilience in volatile markets (Figure 3).

Figure 2: Fidelity China Focus has done exceptionally well against peers over a three-year horizon

Figure 3: Maximum drawdown is nearly half that of peers

(Related article: Revising Our Stance on China: From Negative to Neutral)

An addition to Core Equity – Digital Economy: Eastspring Investments Unit Trusts - Global Technology SGD

It is difficult to deny the growing importance of digital technologies in the world today, and we believe they will drive massive disruption in the years to come. As such, the digital economy should be a cornerstone of investors’ portfolios. We recommend a 20% equity allocation to digital economy stocks, reflecting the importance we place on this sector.

(Related article: Transitioning from GDP-weighting: Our new portfolio strategy revealed)

To better capture the essence of the underlying companies in the universe, we've renamed the ‘Global Technology’ category in our list to ‘Digital Economy.’ Given the substantial allocation, we think the exposure to digital economy could be split between two funds for diversification benefits: Fidelity Global Technology A-ACC-USD, a fund we've consistently recommended, and the newly added Eastspring Investments Unit Trusts - Global Technology SGD.

The latter invests in long-term technology drivers, focusing on companies with high quality management, strong barriers to entry, and un-appreciated growth but at a reasonable price. It holds in a wide range of firms in the digital economy, ranging from internet companies (29.4% of portfolio as of 30 June 2024), players in the semiconductor industry (29.3%), to software providers (20.2%).

Close to 90% of the fund’s holdings are in US companies, with the remainder mainly comprising of firms from Taiwan, Hong Kong, and the Netherlands. The top 10 positions, consisting of Microsoft, NVIDIA, and Alphabet, make up around half of the portfolio (Table 4).

Table 4: Top 10 holdings of the Eastspring Investments Global Technology Fund

|

Company |

Sector |

Weight |

|

Microsoft |

Technology |

9.6% |

|

NVIDIA |

Technology |

8.4% |

|

Alphabet Class A |

Communication Services |

5.8% |

|

Meta |

Communication Services |

5.3% |

|

Amazon |

Consumer Discretionary |

4.9% |

|

Apple |

Technology |

4.2% |

|

AMD |

Technology |

4.0% |

|

Marvell Technology |

Technology |

3.2% |

|

Alphabet Class C |

Communication Services |

3.1% |

|

Micron |

Technology |

2.9% |

|

Total |

51.4% |

|

|

Source: Eastspring Investments, iFAST Compilations Data as of 30 June 2024 |

||

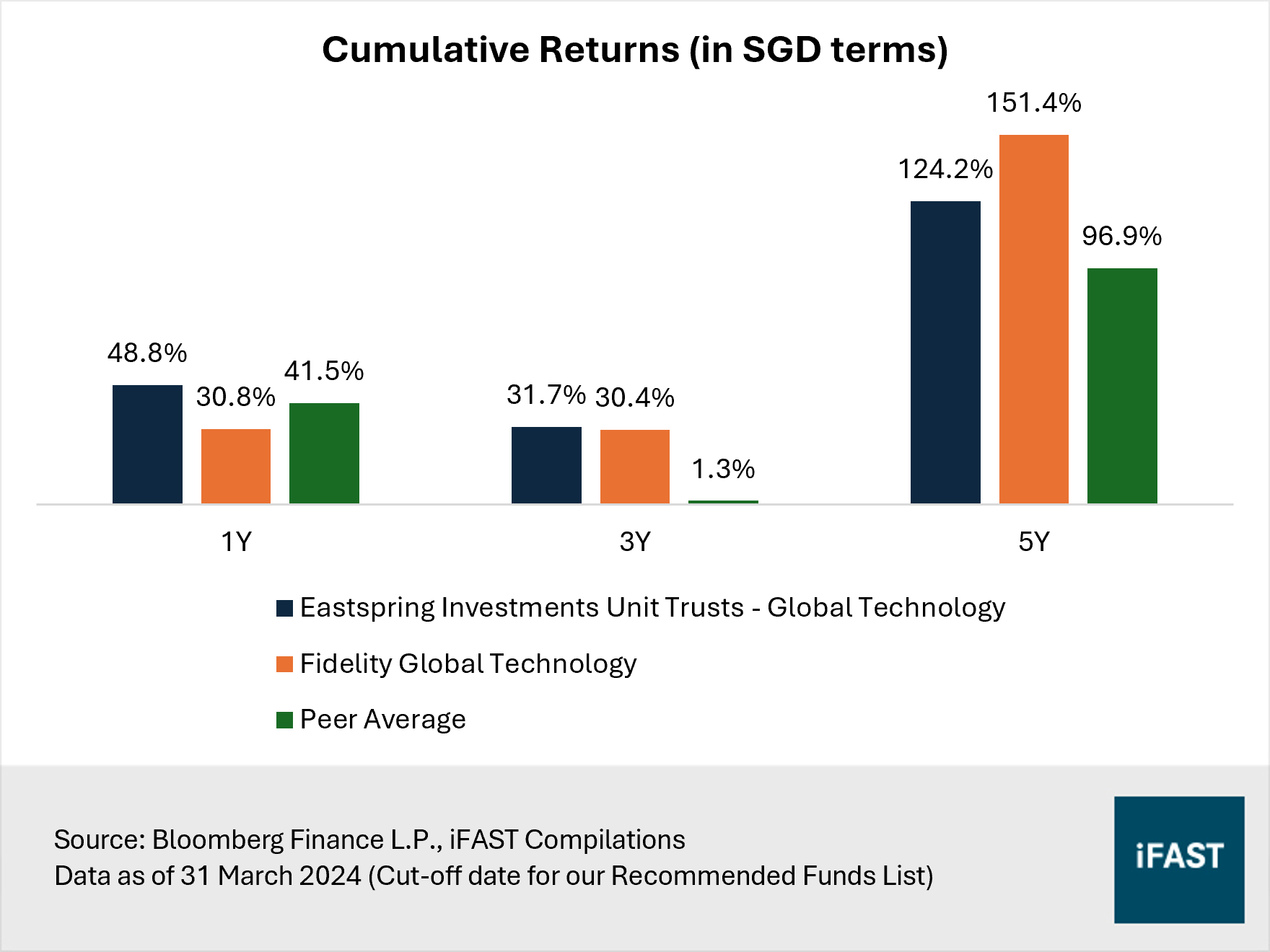

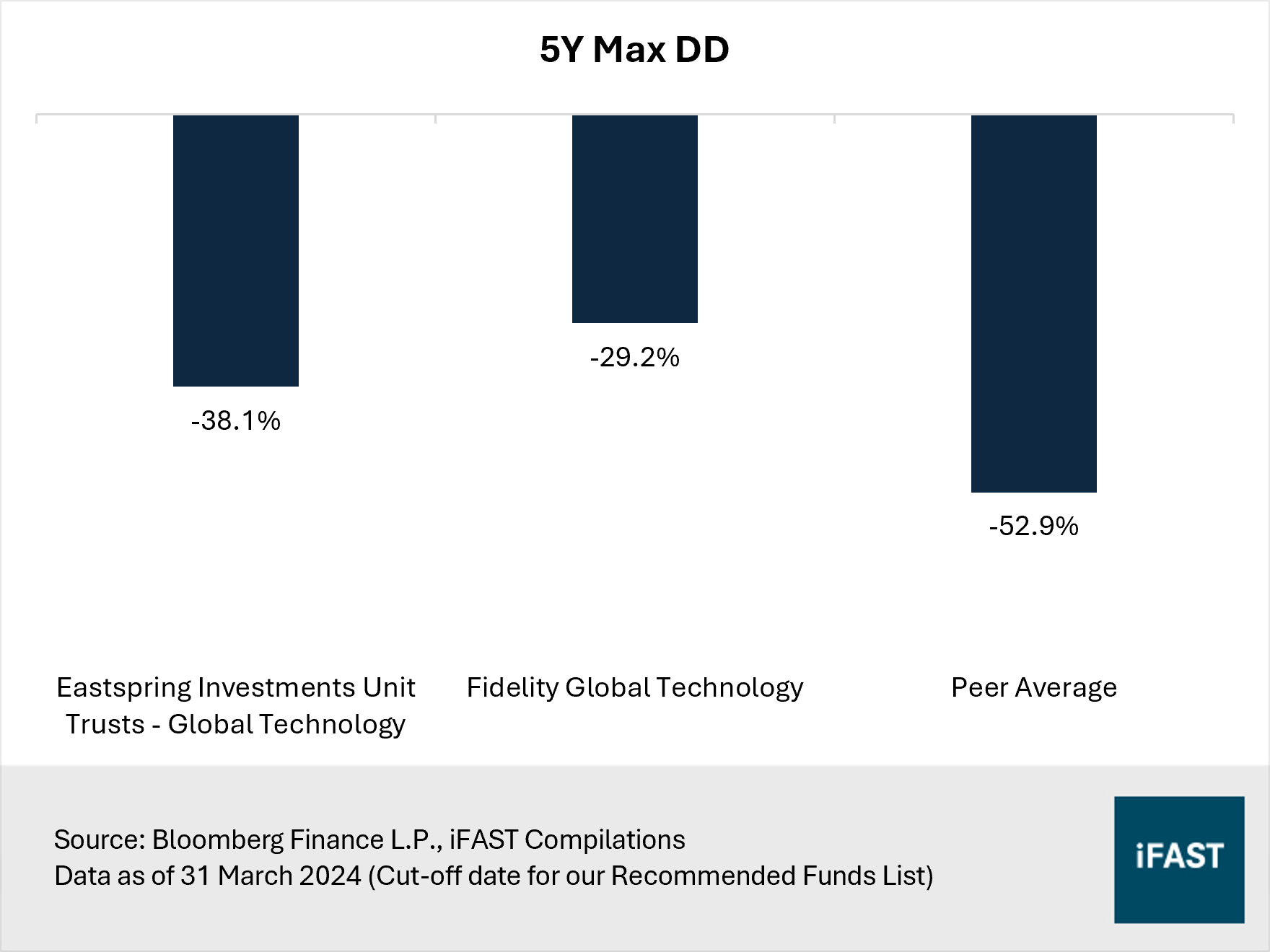

The fund has consistently delivered stronger returns over the past one and three years compared to the Fidelity Global Technology Fund and other peers (Figure 4). Although its five-year cumulative returns of 124.2% and maximum drawdown of -38.1% trail behind Fidelity Global Technology, it has still outperformed its peers by a significant margin (Figure 5).

Figure 4: The Eastspring Investments Global Technology delivered stronger returns versus its peer group

Figure 5: Smaller drawdown compared to its peer group

(Related article: US tech stocks are now on sale. Don’t miss this opportunity.)

A new market in Supplementary Equity – South Korea: JPMorgan Funds - Korea Equity A (acc) USD

With a consistent current account surplus, supportive government policies, technology leadership and world class brands, we believe that South Korea has what it takes to become a new Asian Tiger. In addition, a greater economic expansion for South Korea is likely yet to come on the back of the semiconductor upcycle.

We have opted to include the JPMorgan Funds - Korea Equity A (acc) USD in this year’s list. This fund seeks to generate most of its alpha through stock selection, utilising an investment style that incorporates value, growth, and quality attributes.

It typically maintains a concentrated portfolio, with its top ten holdings currently making up about 45% of the portfolio (Table 5). The top positions include Samsung and SK Hynix, the nation’s two largest semiconductor companies. The two collectively make up more than 70% of the global DRAM market and 50% of global NAND chip production.

Table 5: Top 10 holdings of the JPMorgan Korea Equity Fund

|

Company |

Sector |

Weight |

|

Samsung Electronics |

Technology |

9.9% |

|

SK Hynix |

Technology |

9.9% |

|

Shinhan Financial |

Financials |

4.0% |

|

LG Chem |

Materials |

3.6% |

|

Samsung Biologics |

Healthcare |

3.6% |

|

Hyundai Motor |

Consumer Discretionary |

3.6% |

|

Samsung Electro-Mechanics |

Technology |

2.8% |

|

Samsung Life Insurance |

Technology |

2.7% |

|

Naver |

Communication Services |

2.6% |

|

S-Oil |

Energy |

2.6% |

|

Total |

45.3% |

|

|

Source: JPMorgan, iFAST Compilations Data as of 30 June 2024 |

||

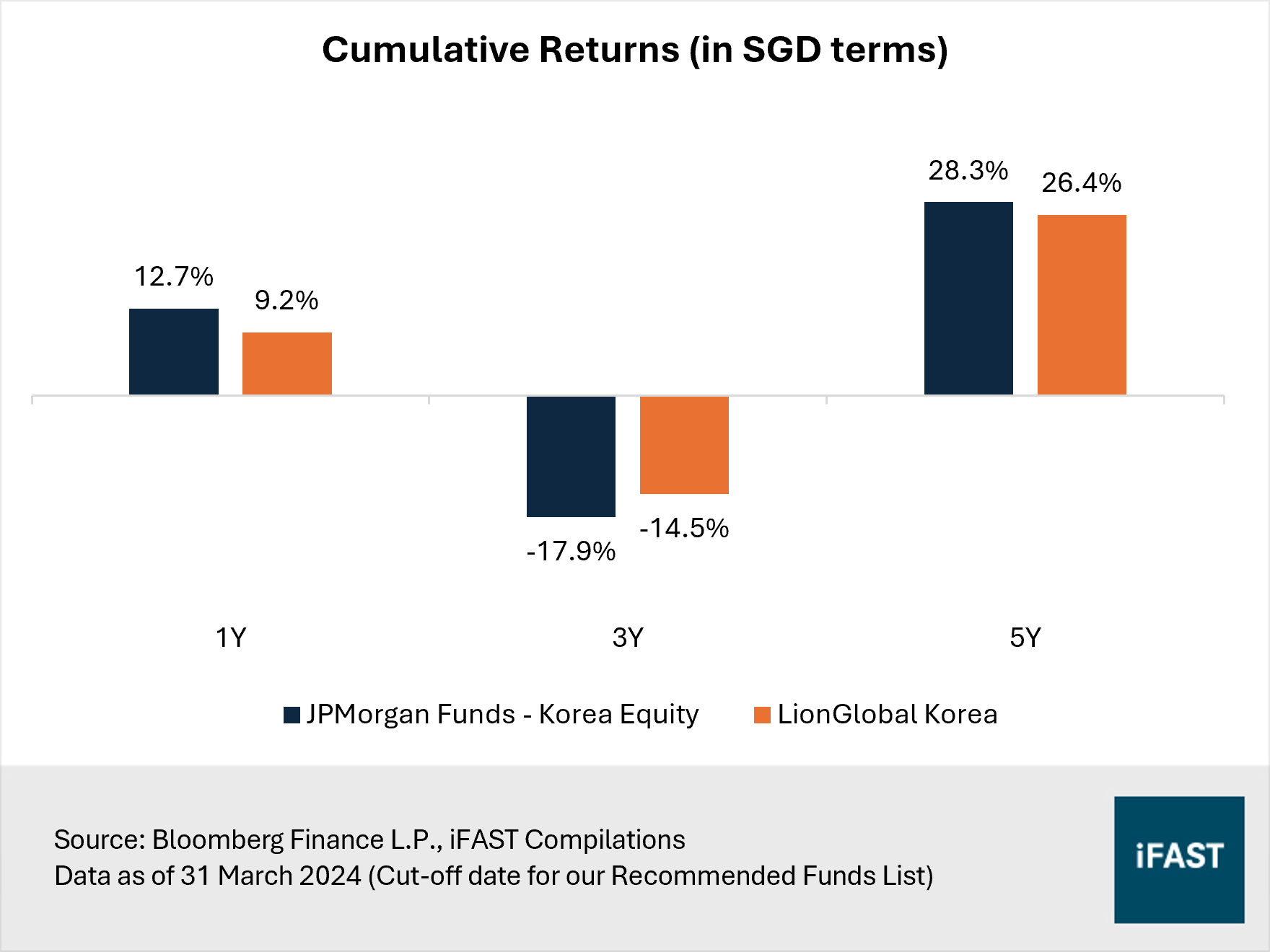

Compared to its peer, the LionGlobal Korea Fund, the fund has posted slightly higher returns over a five-year period, albeit with a higher drawdown of -43.0% versus -37.8% for the LionGlobal fund (Figure 6).

Figure 6: The JPMorgan Korea Equity has done well over the longer term

Fundsupermart Recommended Funds List: A good starting point for investors

If you’re feeling overwhelmed by the choices or simply don’t have the time to dive into every fund on our platform, our Fundsupermart Recommended Funds List is here to help. Click here to view the full report.

In addition to the funds we've highlighted above, we have also introduced some new recommended equity funds extensively in separate articles. Be sure to check them out below!

Table 6: Other new recommended equity funds

|

Category |

Recommended Fund |

Article |

|

Asia ex Japan |

||

|

Emerging Markets |

||

|

India |

RAMS Investment Unit Trust - India Equities Portfolio II A USD |

Seeking opportunities within the world’s fastest-growing major economy |

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.