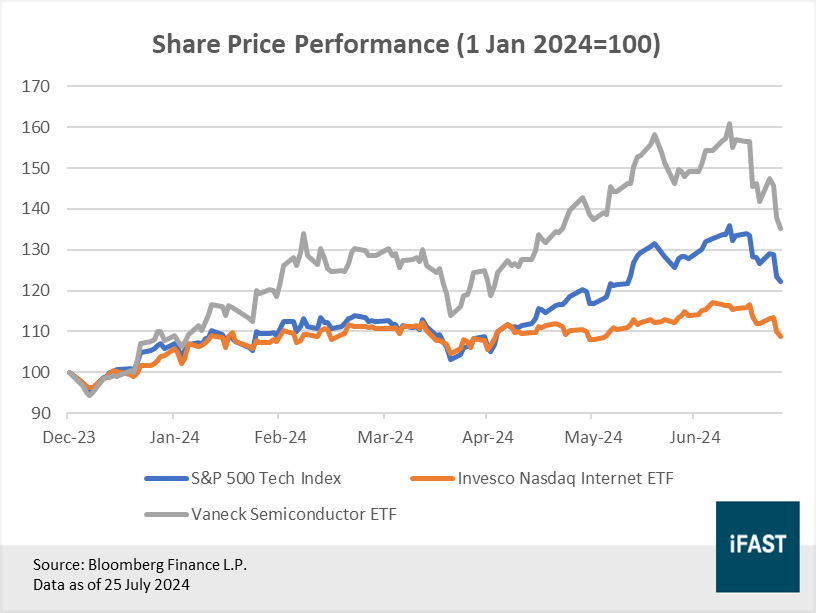

• It’s been a rough two weeks for tech stocks. S&P 500 Technology Index has fallen more than -10% from its peak, while major tech ETFs such as the Invesco Nasdaq Internet ETF and the Vaneck Semiconductor ETF plunged -7.1% and -15.9% respectively.

• With share prices of several tech companies trading close to their all-time highs, investors may be highly motivated to take profits at any sign of negative news.

• The recent selloff was most likely sentiment driven rather than a material deterioration in fundamentals. We reiterate our positive outlook for the tech sector and encourage long-term investors to make use of this opportunity to increase their position.

After making a strong start to the year, US tech stocks have taken a huge beating over the past two weeks. As of 25 July 2024, the S&P 500 Technology Index has fallen more than -10% from its peak, while major tech ETFs such as the Invesco Nasdaq Internet ETF (NASDAQ:PNQI) and the Vaneck Semiconductor ETF (NASDAQ:SMH) plunged -7.1% and -15.9% respectively. Despite the selloff, tech stocks are still sitting on gains of more than 22% on aggregate year-to-date (Figure 1).

Figure 1: Despite the recent selloff, US tech stocks are still up by 22% on aggregate this year

The rout was precipitated by sharp declines in the share prices of big tech companies, which together carry significant weight and have been responsible for the majority of the gains for most US tech ETFs this year. NVIDIA, one of the best performing constituents of the Magnificent 7 group of stocks, shed more than -16% of its value over the past two weeks. Meanwhile, Microsoft, Alphabet and Apple plunged by approximately -10% a piece over the same period.

The selloff over the past two weeks is likely to have been triggered by a mixture of reasons which ultimately led investors to question the sustainability of this rally.

In the semiconductor space, there were rumblings that US regulators were planning to implement tougher rules to further clamp down on chip exports to China. While such restrictions are already in place to a certain extent, the Biden administration is reportedly considering imposing more extreme measures such as the foreign direct product rule (FDPR), which would effectively restrict the export of semiconductor products that use even the tiniest amount of US technology to fabricate.

Sentiment surrounding chipmakers is visibly poor as even companies like TSMC and SK Hynix which just recently reported strong second quarter earnings were not spared from the selloff. The latter, which delivered record high quarterly revenues on the back of higher memory prices and strong demand for AI memory (including high bandwidth memory), saw its share price tumble close to -9% the day after results were announced.

Beyond the chipmaking industry, Alphabet also saw a post earnings selloff even as the company beat estimates on both the top and bottom line. Shares of Microsoft were hammered after the company suffered a major cloud service outage, piling on to the negative sentiment on tech stocks.

Selloff likely to be sentiment driven. Long-term growth story remains intact

Overall, we believe that the recent selloff is predominantly driven by negative sentiment, rather than any material deterioration in fundamentals. With share prices of several tech companies trading close to their all-time high prior to the selloff, investors may be highly motivated to take profits at any sign of negative news.

Even though some investors have expressed fears that the market might be headed towards another tech bubble driven by an overinvestment in AI, we think that such fears are overblown at this point in time. For one, the hyperscalers which have been investing heavily in AI have reported healthy demand for their services.

Alphabet for instance reported strong revenue growth in its search advertising and cloud units. In its latest earnings call, Alphabet’s CEO said that “AI infrastructure and generative AI solutions for cloud customers have already generated billions in revenues”. The company is also seeing great progress with AI Overviews, which is a tool that summarises search results for users. The management of TSMC, the largest producer of AI chips also said that demand for AI chips continues to outpace supply, a situation that is unlikely to normalise before 2026.

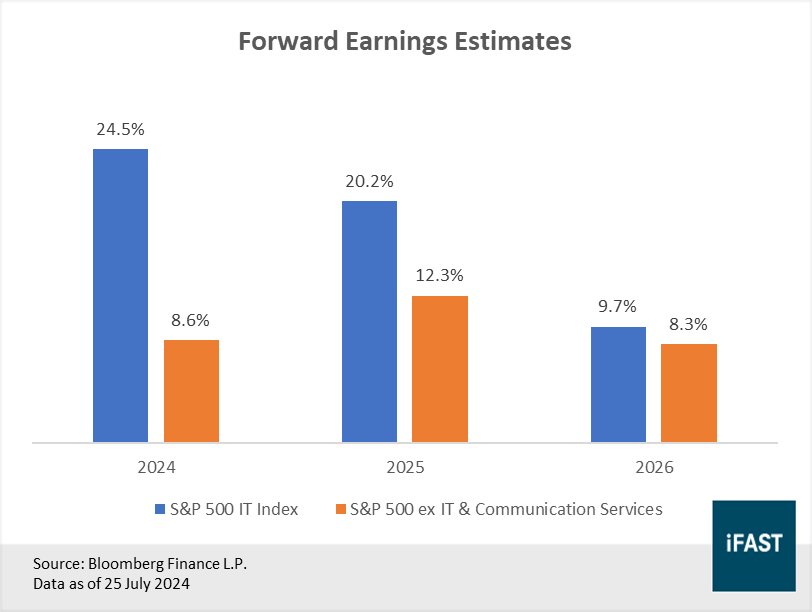

While valuations of tech stocks have gotten more expensive in recent times, they are still far from bubble territory. More importantly they are justifiable as tech companies continue to deliver impressive earnings growth that outpaces the broader market, a trend that is expected to persist as the world becomes increasingly digitalised (Figure 2).

Figure 2: US tech firms to deliver strong earnings growth in the years ahead

Don’t miss this golden opportunity to pick up more shares

Overall, we remain optimistic about the prospects of the tech sector. Besides the ability to deliver strong earnings growth (a key catalyst that should drive share prices higher), big tech stocks are arguably the most desirable group of companies to own in the current macroeconomic environment.

With inflation and interest rates likely to stay higher for longer, the focus on high quality companies, such as those with resilient earnings, strong balance sheets and competitive advantages cannot be understated. Big tech stocks check all these boxes. Long-term investors should consider making use of this opportunity to add to their position.

Table 1: Recommended products for US tech

|

Recommended Products |

|

|

Unit Trust |

|

|

ETF |

|

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in the Vaneck Semiconductor ETF.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.