- Valuations of Chinese equities have significantly declined due to worsening investor sentiment. With valuations at such low levels, we believe that the impact of economic challenges and restrictive policies has largely been factored in.

- China's property market may have reached its bottom. Moving forward, we expect increased stabilisation, though no strong catalysts are anticipated to drive a full recovery. The market is likely to continue weighing on GDP growth.

- China is gradually easing policies that previously prioritised control over growth, with sentiment now playing a more significant role in policy decisions. Restoring business confidence will be a gradual process, given the extent of past damage.

- For those still optimistic about China and willing to accept higher risk, now presents a favourable opportunity. China can serve as a tactical position within investment portfolios, but it involves higher risks and necessitates frequent monitoring.

- We are revising our stance on China from bearish to neutral, upgrading its star rating from 2.0 to 2.5 stars. This adjustment reflects an estimated upside potential of approximately 11.5% by 2026.

Chinese stocks present opportunities after declining to dirt-cheap levels

Over the past two years, China's economy has faced significant internal challenges, including a widespread property market crisis, weak employment prospects, deflationary pressures, declining confidence, and growing tensions with Western countries. In November 2022, we downgraded China to a 2.0-star rating, deeming it "unattractive" due to concerns about its economic outlook.

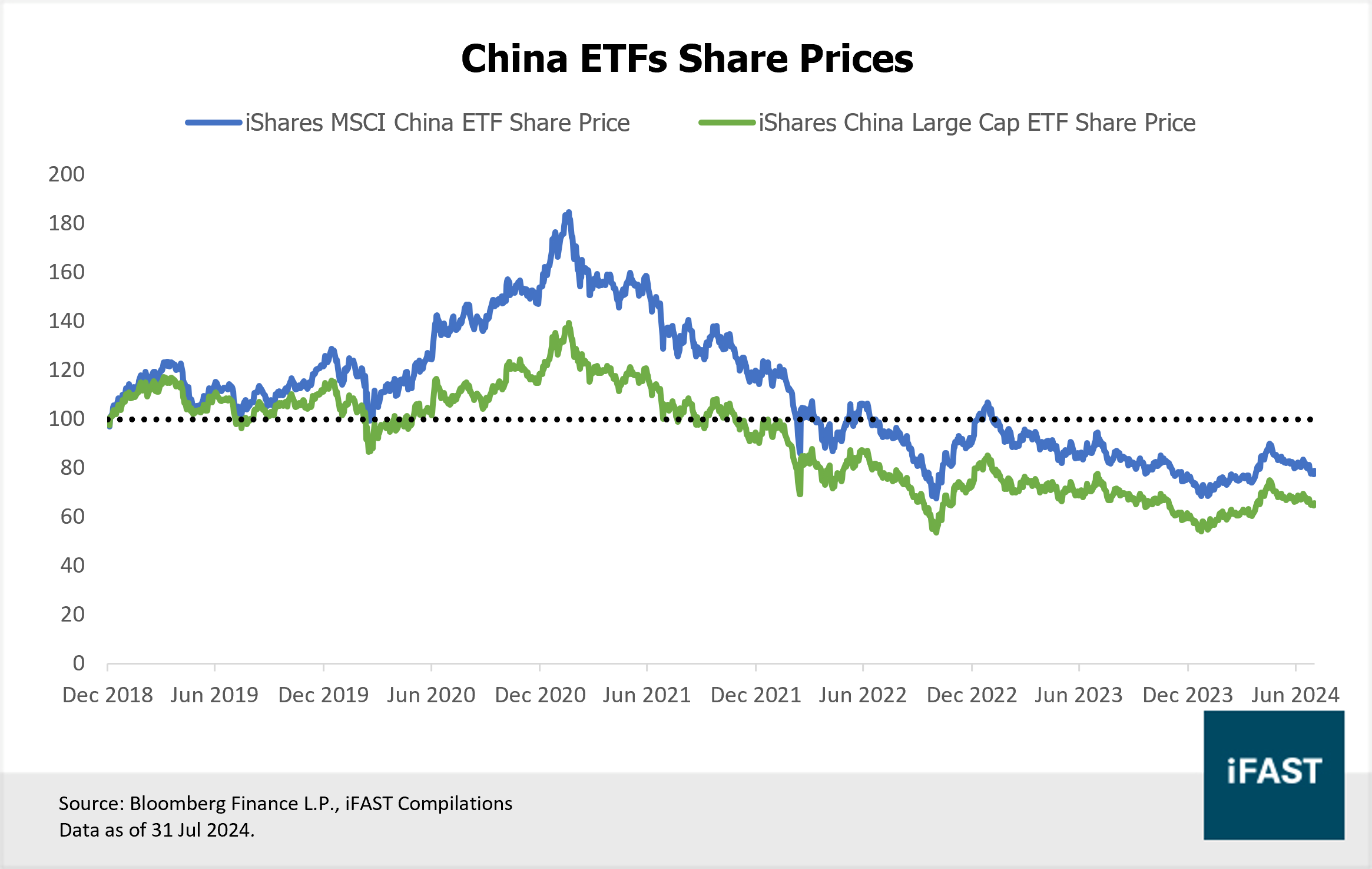

In the global market, investor sentiment towards China also deteriorated, leading to significant foreign capital outflows in 2022 and 2023. This exodus has been marked by a sharp decline in the value of Chinese shares and a pullback in business investments. Once-popular China ETFs, such as the iShares MSCI China ETF and iShares China Large Cap ETF, have seen substantial price drops. As of 31 July 2024, these ETFs are still trading at about half of their peak levels from February 2021.

Figure 1: China’s ETF prices have dropped to just half of their peak levels in February 2021

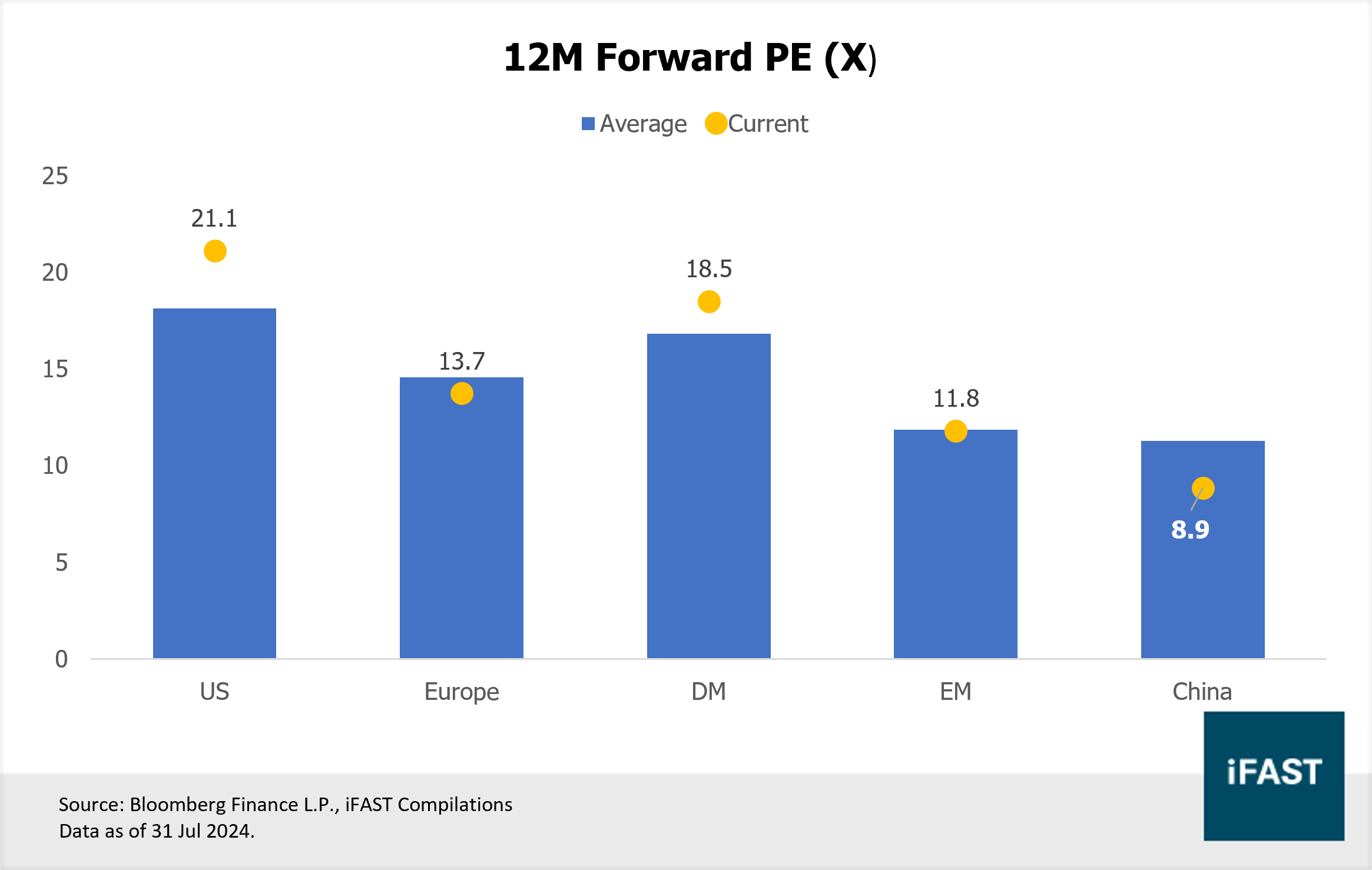

This has resulted in China's shares trading at exceptionally low prices. As of 31 July 2024, the 12-month forward PE ratio of the MSCI China Index was at a 21.4% discount compared to its 10-year historical average, and 17.1% below the 10.7X level at which we downgraded the market to 2.0 stars in November 2022. Additionally, China's valuation also shows substantial discount when compared to its emerging market peers and the global market as a whole. (Figure 2).

Figure 2: China’s valuation is much lower than its historical average and peers

Overall sentiment toward China remains bearish, but we believe the current valuations may be overly pessimistic as the market would have already factored in the impact of China's longstanding economic challenges and policies that have stifled industry growth. Also, with the recent waves of economic policies becoming more practical, these low valuations may present an opportunity for correction.

The property market may have bottomed

In terms of the property market, we acknowledge that we do not foresee any strong catalysts on the horizon that could fully resolve its issues, particularly given China's reluctance to use substantial stimulus measures to boost consumption. The recent 10 basis point cut in the five-year Loan Prime Rate (LPR) to 3.85% was too little to significantly impact mortgage demand or home sales. We believe a full recovery in the property sector will require more aggressive approaches to address the underlying demand challenges.

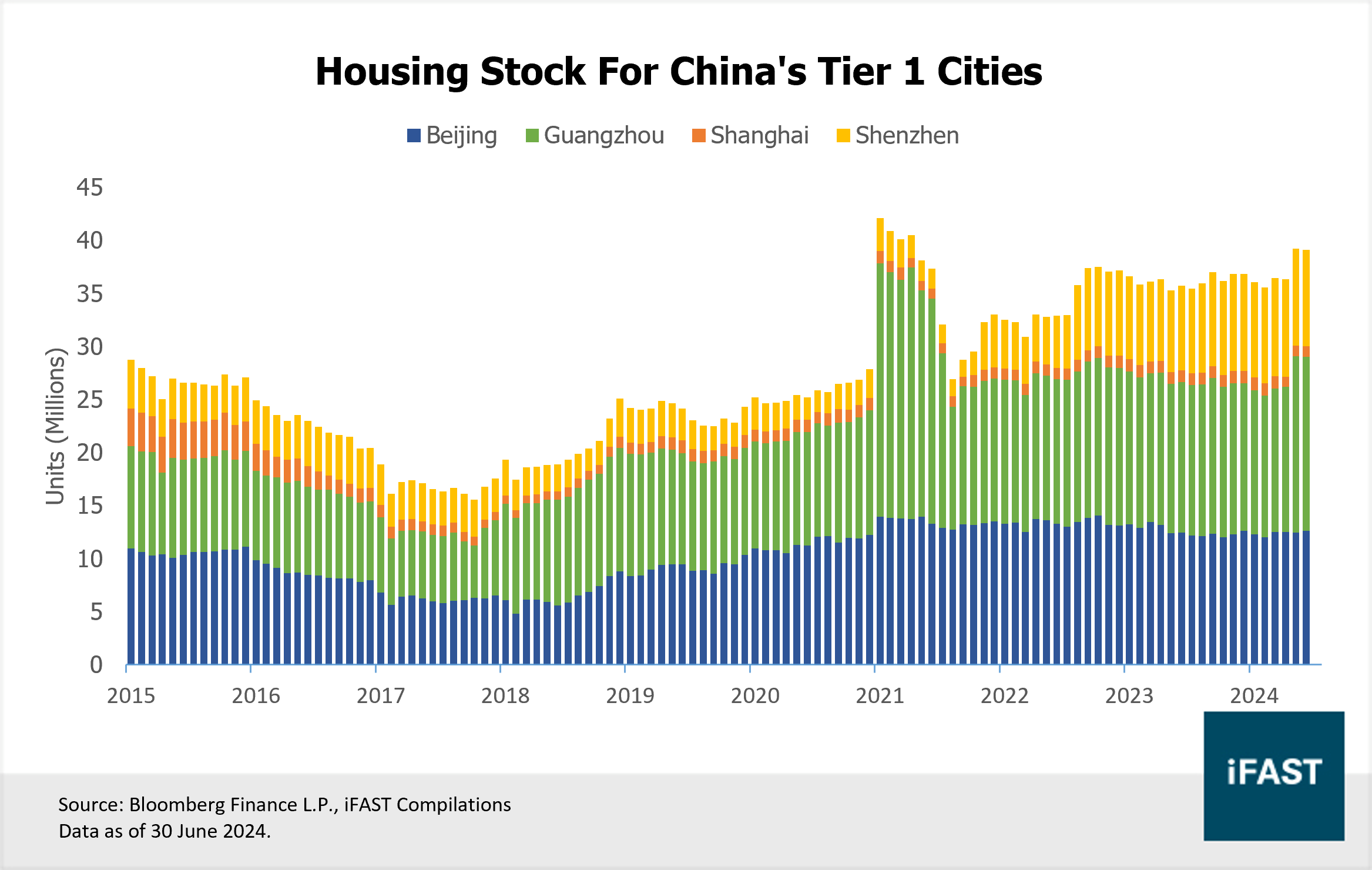

As such, we anticipate that the drag on GDP growth may persist. In tier-1 cities, housing inventory continues to accumulate as government and bank funding supports new completions, while demand remains subdued (Figure 3). The substantial inventory still needs to be absorbed before new investments can significantly drive recovery and growth.

Figure 3: House inventory continues to accumulate in tier-1 cities

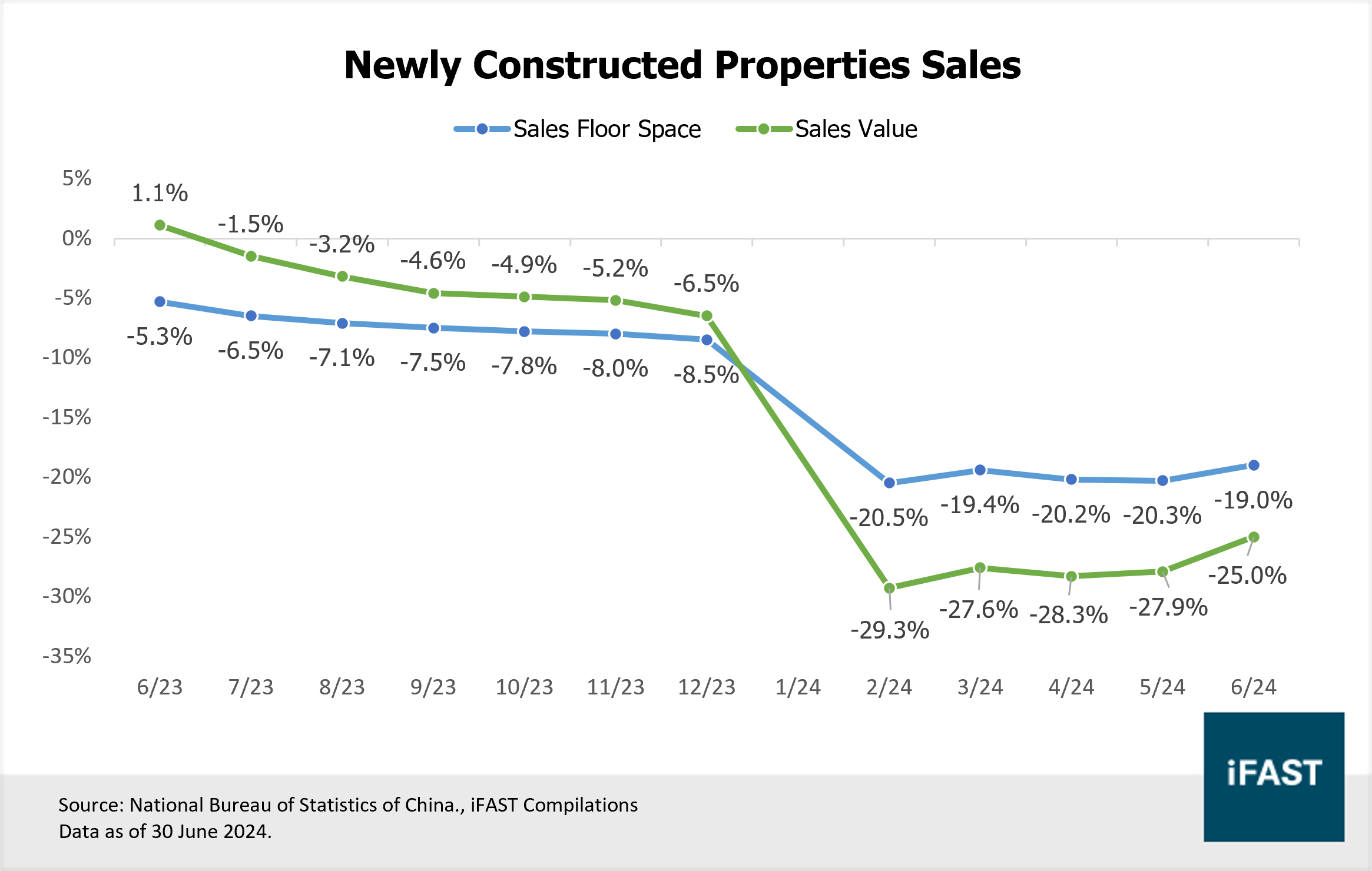

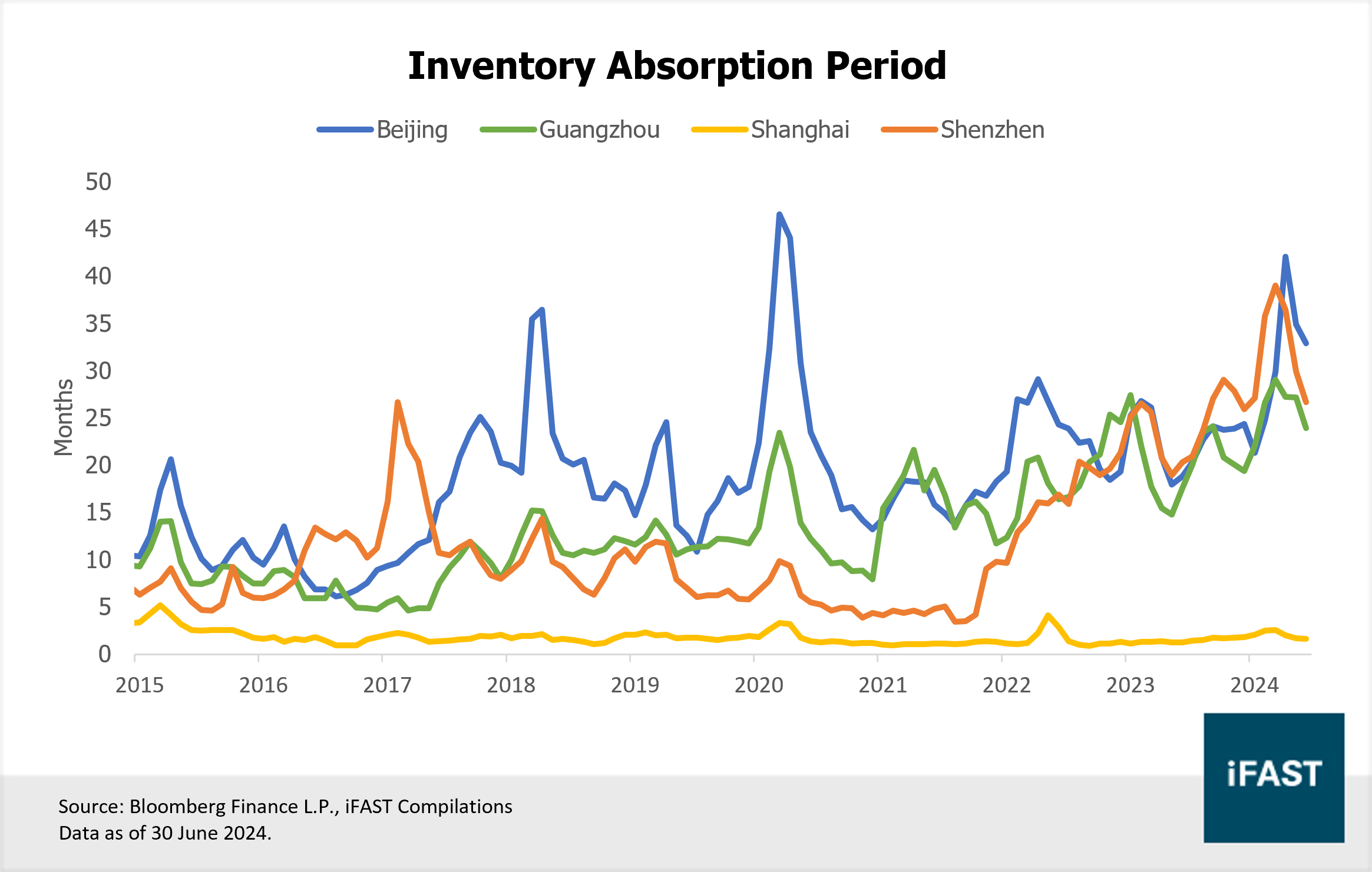

While we do not expect a full recovery in the property market, we have seen some signs of stabilisation. Sales declines have shown some moderation since reaching their lowest point in February of this year (Figure 4). Additionally, the inventory absorption period in the tier-1 cities has decreased from its peak in March and April 2024 (Figure 5). We view price stability in major cities as a leading indicator for the broader housing market, given their better employment opportunities, amenities, and appeal to younger populations. As such, the property market may have reached its bottom.

Figure 4: New home sales continued to decline but at a slower rate

Figure 5: The housing inventory absorption period in tier-1 cities has decreased from its peak

Sentiment and pragmatism are becoming increasingly influential in shaping policy decisions

In response to a struggling economy, China has been gradually relaxing policies that previously prioritised control over growth. Sentiment is now playing a more significant role in shaping China’s policy framework. This shift began in January when China withdrew proposed video game regulations and dismissed Feng Shixin, head of the publishing unit at China’s Publicity Department, after the draft rules led to billions of losses in the video gaming industry.

Since then, there have been no further crackdowns on industries, signalling that the government is now realising the need to revive the entrepreneurial spirit. During the Third Plenary Session, China committed to treating private companies on par with state-owned enterprises, supporting their share listings, bond sales, and international expansion, and consulting with entrepreneurs before drafting new policies.

However, the intense crackdowns on sectors like technology, education, and gaming have left businesses highly cautious. This hesitance is evident in the sluggish growth of private investments, which saw only a marginal increase of 0.1% year-on-year in the second quarter. In June, Chinese corporations continued to amass fixed deposits, reaching CNY55.7 trillion, while reducing their cash holdings in current accounts. We believe that restoring investor confidence and encouraging more private investment will require a considerable amount of time.

Another key takeaway from the Third Plenary Session is the government's shift towards more pragmatic solutions for addressing economic issues.

Firstly, China dropped its past fixation on chasing high GDP growth figures, as highlighted by Xi Jinping's statement that China may accept lower GDP growth in the future while prioritising high-quality development.

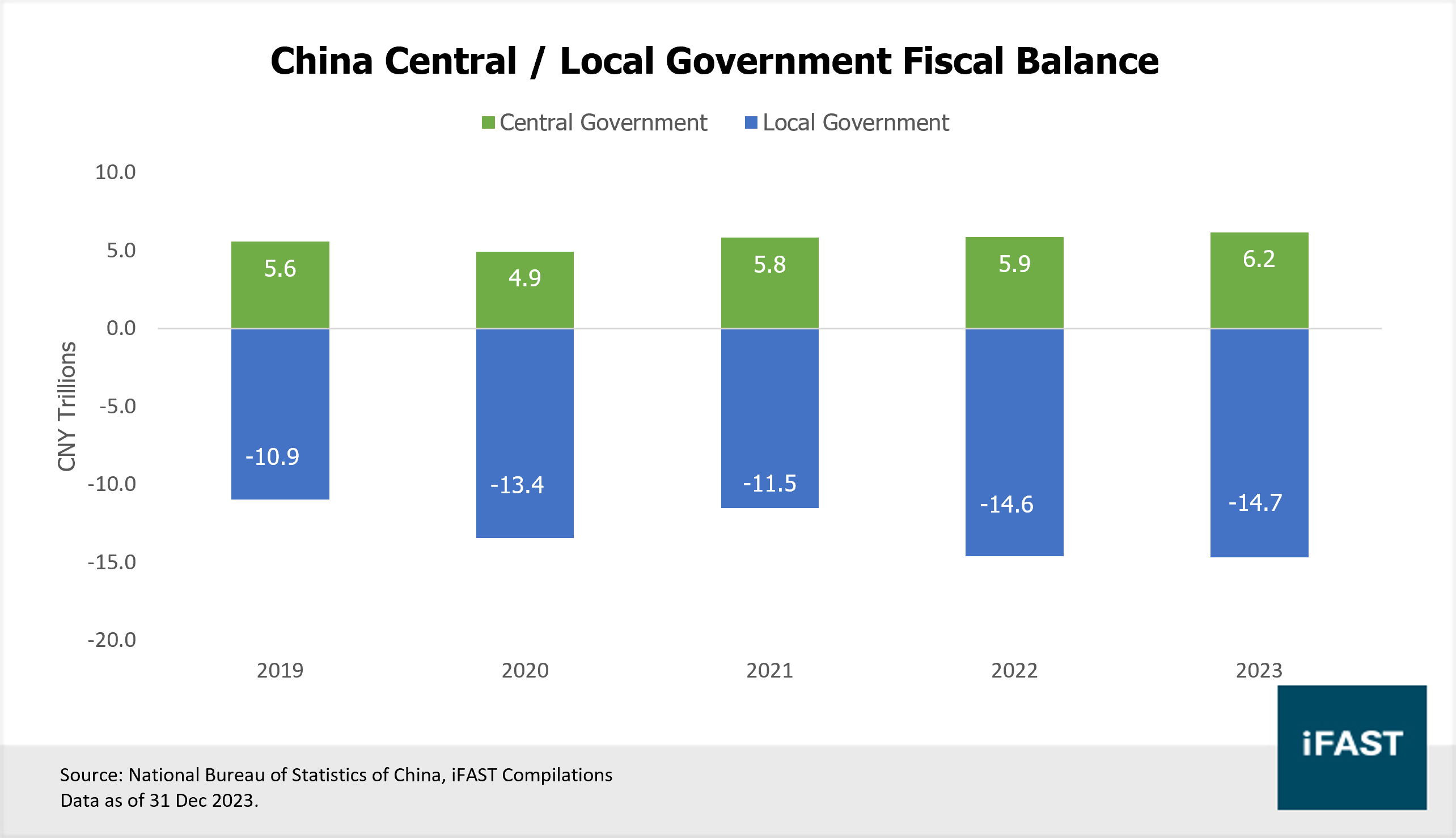

Secondly, China plans to restructure its fiscal system to alleviate the financial strain on heavily indebted local governments. A key measure includes reallocating a larger share of consumption and value-added tax revenues from the central government to regional governments. This adjustment in fiscal transfers represents a more practical approach than seeking new revenue sources to replace land sales in the short term, particularly given that the central government has maintained a budget surplus over the past five years (Figure 6).

Figure 6: Fiscal balance of China's central and local governments

As policies shift toward pragmatism, we expect to see more stabilising forces in the near term, though their impact on reversing the economic downturn will be limited. For instance, reallocating funds from central to local governments can help cover some expenses but will not fully address the fiscal imbalance due to high local debt levels. While this approach may prevent further escalation of local debt issues, it will not resolve them without new revenue sources.

China as a tactical investment in your portfolio

China’s current low valuations present an opportunity for potential gains. Based on our fair P/E ratio of 10X, we project a target price of approximately HKD 63.1 for the MSCI China Index by 2026 (Table 1), suggesting an upside potential of around 11.5% from the closing price on 31 July 2024. We have adjusted China’s star rating from 2.0 stars “negative” to 2.5 stars “neutral”, factoring in both the stabilising trend and ongoing long-term structural issues.

Table 1: China’s cheap valuation allows some room for upside

|

MSCI China Index |

FY23 |

FY24E |

FY25E |

FY26E |

|

PE Ratio (X) |

11.7 |

11.0 |

10.1 |

9.0 |

|

Expected Earnings Growth (YoY%) |

4.8% |

6.4% |

8.9% |

12.5% |

|

Earnings Per Share (EPS) |

4.8 |

5.1 |

5.6 |

6.3 |

|

Projected Fair Price (based on a fair PE ratio of 10.0X) |

63.1 |

|||

|

Potential Upside |

11.5% |

|||

|

Source: Bloomberg Finance L.P., iFAST Compilations |

|

|||

Although China’s equity valuations are currently low and the property market is likely to bottom out, structural issues will remain. The absence of concrete plans to solve existing economic challenges means China’s economy will trend toward a more stable, albeit slower, growth trajectory in the coming years. Persistent low inflation, escalating tensions with Western economies, and increased export pressures due to trade tariffs all contribute to a protracted recovery period for China.

In June, we revised our portfolio management approach, transitioning from a GDP-weighted to a market-cap-weighted strategy. This adjustment has led to the elimination of our direct allocation to China while maintaining exposure through Asia ex-Japan and emerging markets investments. We now view China as better suited for tactical rather than core allocation within an investor's portfolio. A tactical strategy entails higher risk and necessitates more frequent monitoring but provides opportunities for investors who are bullish about China to capitalise on valuation gaps by adjusting their positions accordingly.

Related article: Transitioning from GDP-weighting: Our new portfolio strategy revealed

For investors who have long waited to increase their allocation to Chinese equities, now is an opportune time to make such an adjustment. We recommend unit trust products such as Schroder China Opportunities Acc SGD and Fidelity China Focus A-ACC USD for active investments. For those who prefer passive investment options, we recommend the iShares Core MSCI China ETF (HKEX.2801).

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report holds a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.