- China, a key player in the emerging markets (EM) space, the economy is showing signs of stabilisation. Additionally, secular trends such as the semiconductor upcycle, supply chain diversification, and commodity growth driven by decarbonisation are expected to boost the overall EM space.

- The JPM Emerging Markets Dividend A (mth) USD fund focuses on high-yielding stocks with strong dividend growth potential in emerging markets. Over the past year, it has delivered an annualised dividend yield between 4.22% and 5.09%.

- With a strong emphasis on quality, the fund has demonstrated solid performance and favourable risk metrics, outperforming both its benchmark and peers.

- This fund offers an attractive diversification option for investors seeking opportunities beyond the US or developed markets.

Emerging Markets: Investment Opportunities on the Horizon

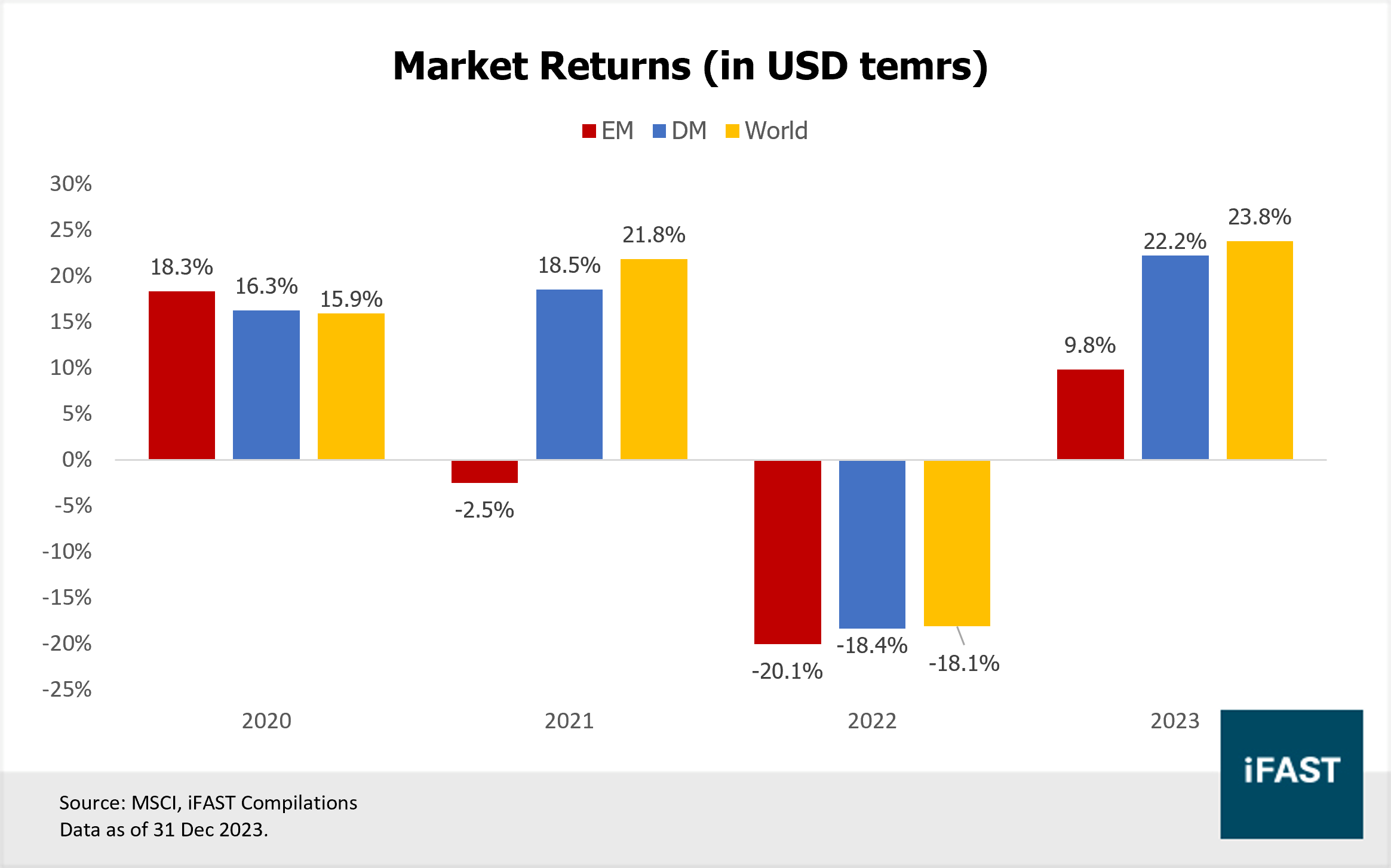

Emerging market stocks have consistently underperformed compared to developed markets and the globe since 2021. Despite a slight recovery, as of 12 August 2024, the MSCI Emerging Markets Index remains 25.3% below its peak reached in February 2021.

Figure 1: EM’s returns have lagged behind DM and the world since 2021

The poor performance of emerging market stocks can largely be attributed to China’s troubled property market, persistent deflationary pressures, and escalating tensions with the West. These factors have led to investor pessimism about China, which significantly impacted other emerging markets given China's status as a major trading partner. Additionally, with China comprising about a quarter of the MSCI Emerging Markets Index, its economic outlook heavily influences investor sentiment toward the broader emerging markets.

While we do not foresee a strong catalyst to drive a full rebound in China, there are signs of stabilisation. The property market seems to have bottomed out, as evidenced by a deceleration in the decline of sales. Additionally, the government has begun adopting a more pragmatic approach to policymaking, with an emphasis on enhancing entrepreneurial confidence and stimulating economic growth. Furthermore, China’s current valuation is notably low, indicating potential for a correction. Consequently, we have revised our outlook on China from “negative” to “neutral” and raised its star rating from 2.0 to 2.5 stars.

Related article: Revising Our Stance on China: From Negative to Neutral

More importantly, we have seen several secular growth drivers that could significantly boost emerging markets' expansion beyond China:

Semiconductor Upcycle: The recovery in the semiconductor industry has been particularly beneficial for countries like South Korea and Taiwan. South Korea's semiconductor exports have risen for nine consecutive months, driven by its strong position in memory chips, with a notable 13.9% year-on-year increase in July. Similarly, Taiwan's robust position in the foundry businesses has led to significant gains. We believe the sustained demand for AI chips and the growing digitalisation of the world will provide long-term growth opportunities for semiconductors and benefit these two markets.

Supply Chain Diversification: As geopolitical tensions between China and Western countries escalate, there is a growing push for supply chain diversification, encapsulated in the “China plus one” strategy. Many companies are relocating factories to other emerging markets that offer a skilled labour force at relatively low wages. Countries such as India, Indonesia, Vietnam, and Mexico are benefiting from this shift, positioning themselves as key players in the evolving global supply chain.

Decarbonisation-driven Commodity Growth: The global transition to a greener economy has heightened demand for minerals essential for clean energy technologies. The production of solar panels and electric vehicle batteries requires raw materials like copper, cobalt, and lithium. Latin American and ASEAN countries with significant mineral reserves, including Chile, Brazil, Mexico, Indonesia, and Thailand, stand to gain substantially from these decarbonisation trends.

JPM Emerging Markets Dividend Fund: Leveraging a Dividend Strategy to Capture Growth Opportunities

To help investors seize growth opportunities in emerging markets, we highlight the JPM Emerging Markets Dividend A (mth) USD, co-managed by Omar Negyal and Isaac Thong. Omar Negyal offers 14 years of extensive experience in global emerging markets income strategies, while Isaac Thong has served as a portfolio manager for the fund since June 2020.

The JPM Emerging Markets Dividend A (mth) USD focuses on identifying high-yielding stocks with strong dividend growth potential in emerging markets. Due to the inherent inefficiencies and volatility of these markets compared to developed ones, the fund manager views dividends as a reliable indicator of corporate health and high-quality governance.

The managers employ several strategies to mitigate higher volatility while capitalising on growth opportunities in emerging markets.

Firstly, the fund utilises a bottom-up research methodology with a strong emphasis on quality. The investment team performs comprehensive fundamental analysis to identify high-quality businesses that offer an optimal blend of income and growth potential. They evaluate a company's current dividend-paying capacity, its sustainability, and the anticipated growth of dividends over the next five years. Beyond dividends, the fund also invests more heavily in companies with robust balance sheets to mitigate the risk of forced sales during economic downturns or periods of financial stress.

Secondly, the fund is designed to hold investments for over five years, allowing the investment team to develop a deep understanding of its target companies through extensive engagement with their management teams. This approach aims for a low turnover strategy, targeting an annual turnover ratio of 20% to 35%. By maintaining a long-term portfolio, the fund is positioned to benefit from the compound growth in emerging markets and, more specifically, from the compounded growth of dividends.

Thirdly, the fund places a strong emphasis on liquidity. It invests exclusively in stocks with an average daily trading value of at least USD 7 million, reducing the challenge of liquidating positions during periods of low liquidity.

Fourthly, diversification is a key consideration. The fund limits its holdings in any single company to no more than 10% of the portfolio, regardless of the company's management quality. As a result, the fund aims to maintain a relatively diversified portfolio between 50 to 80 stocks.

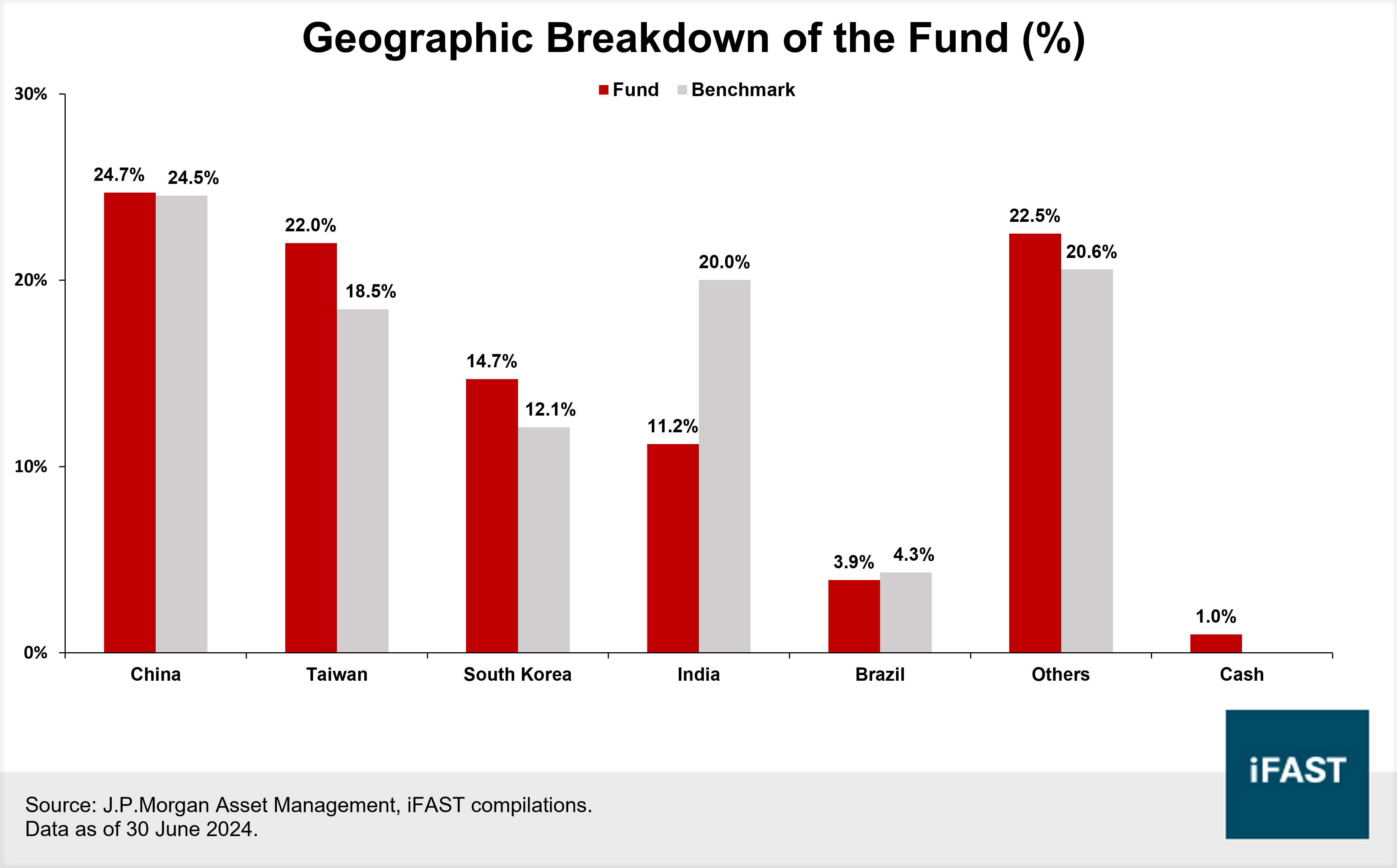

While the fund primarily emphasises bottom-up research, it also incorporates a top-down approach to give the investment team a broader understanding of the global context. The fund's most significant underweight is in India (8.8%) (Figure 2), where companies generally offer less attractive dividend yields compared to other emerging markets. The fund's position in China is aligned with the benchmark MSCI Emerging Market Index. Despite the challenging environment in China, the fund managers remain optimistic about stock opportunities, particularly in sectors such as home appliances, consumer staples, and defensive industries.

Figure 2: The fund holds the largest underweight position in India

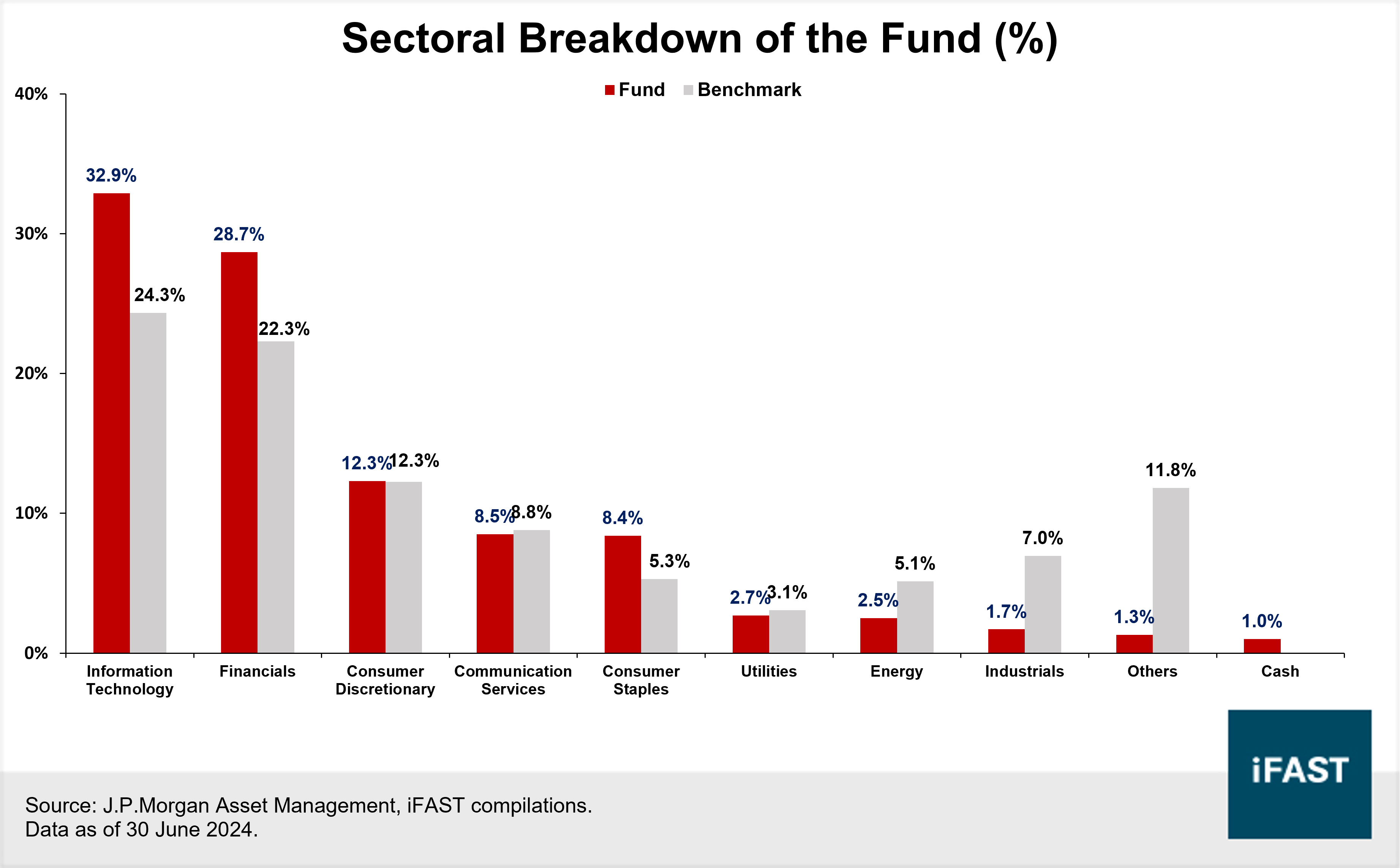

From a sectoral perspective, the manager identifies the most promising income opportunities within the technology and financials sectors. This is reflected in the fund’s absolute allocations, with 32.9% of the portfolio dedicated to information technology and 28.7% to financials. Additionally, these allocations represent the fund's largest overweight exposure compared to the benchmark MSCI Emerging Markets Index (Figure 3).

Figure 3: The fund finds the most appealing income opportunities in infotech and financials

Within the information technology sector, the fund focuses on stocks benefiting from continued strength in high-performance computing. Given the current semiconductor upcycle, the fund manager anticipates significant gains for high-bandwidth memory (HBM) manufacturer Samsung Electronics, which makes up 5.3% of the portfolio. The fund also has substantial exposure to Taiwan Semiconductor Manufacturing Company, with a 9.7% allocation, and computer and electronics hardware manufacturer Quanta Computer, with a 2.6% allocation.

Additionally, the fund is optimistic about Indian information technology services companies, including Infosys, TCS, and HCL Technologies. Infosys, in particular, stands out as the third-largest allocation in the fund at 3.6%.

In the financials sector, the portfolio targets companies that offer both structural growth opportunities and attractive yields, focusing on markets such as Hong Kong, China, and Indonesia. As a result, the fund's top ten holdings feature Bank Rakyat Indonesia (BRI), a leading bank in Indonesia, with a 2.1% allocation. In addition to the previously mentioned markets, the fund also has a modest allocation to Saudi Arabia. It has invested 2.3% in the Saudi National Bank, the largest commercial bank in the country, which is anticipated to offer an annualised dividend yield of approximately 5.1% in 2024.

Table 1: The top ten holdings include six IT companies

|

Name of Holding |

GICS Sectors |

Portfolio Weight (%) |

|

Taiwan Semiconductor |

Information Technology |

9.7% |

|

Samsung Electronics |

Information Technology |

5.3% |

|

Infosys |

Information Technology |

3.6% |

|

Quanta Computer |

Information Technology |

2.6% |

|

NetEase |

Communication Services |

2.5% |

|

Tencent |

Communication Services |

2.5% |

|

ASE Technology |

Information Technology |

2.4% |

|

Saudi National Bank |

Financials |

2.3% |

|

Realtek Semiconductor |

Information Technology |

2.3% |

|

Bank Rakyat Indonesia |

Financials |

2.1% |

|

Total |

35.3% |

|

|

Source: J.P.Morgan Asset Management, iFAST compilations. |

||

Robust performance driven by top-quality stock selection

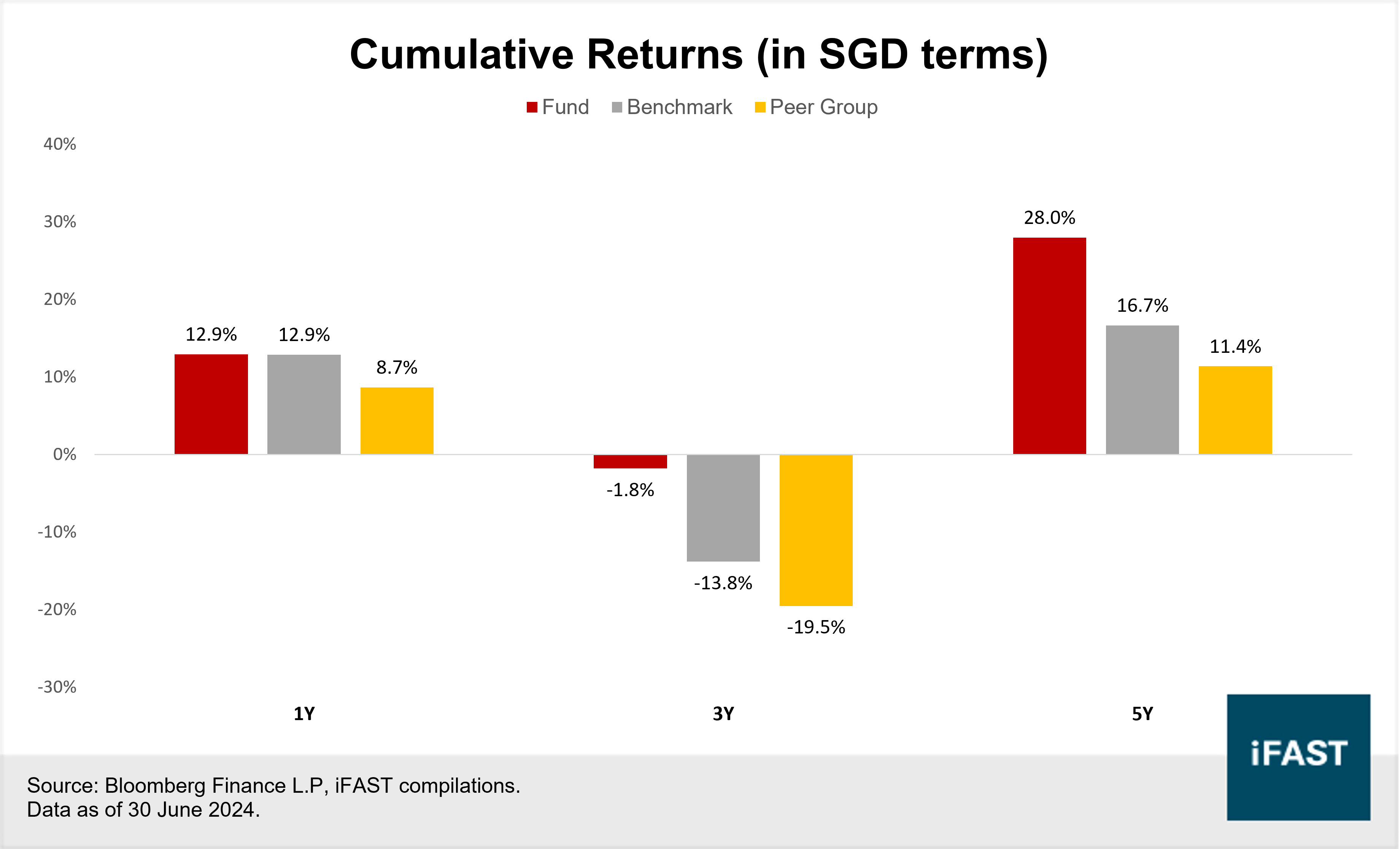

The JPM Emerging Markets Dividend A (mth) USD has delivered strong cumulative returns over one, three, and five-year periods, outperforming both the benchmark and other emerging markets funds available on our platform.

Figure 4: The fund has delivered the best cumulative returns across all time periods

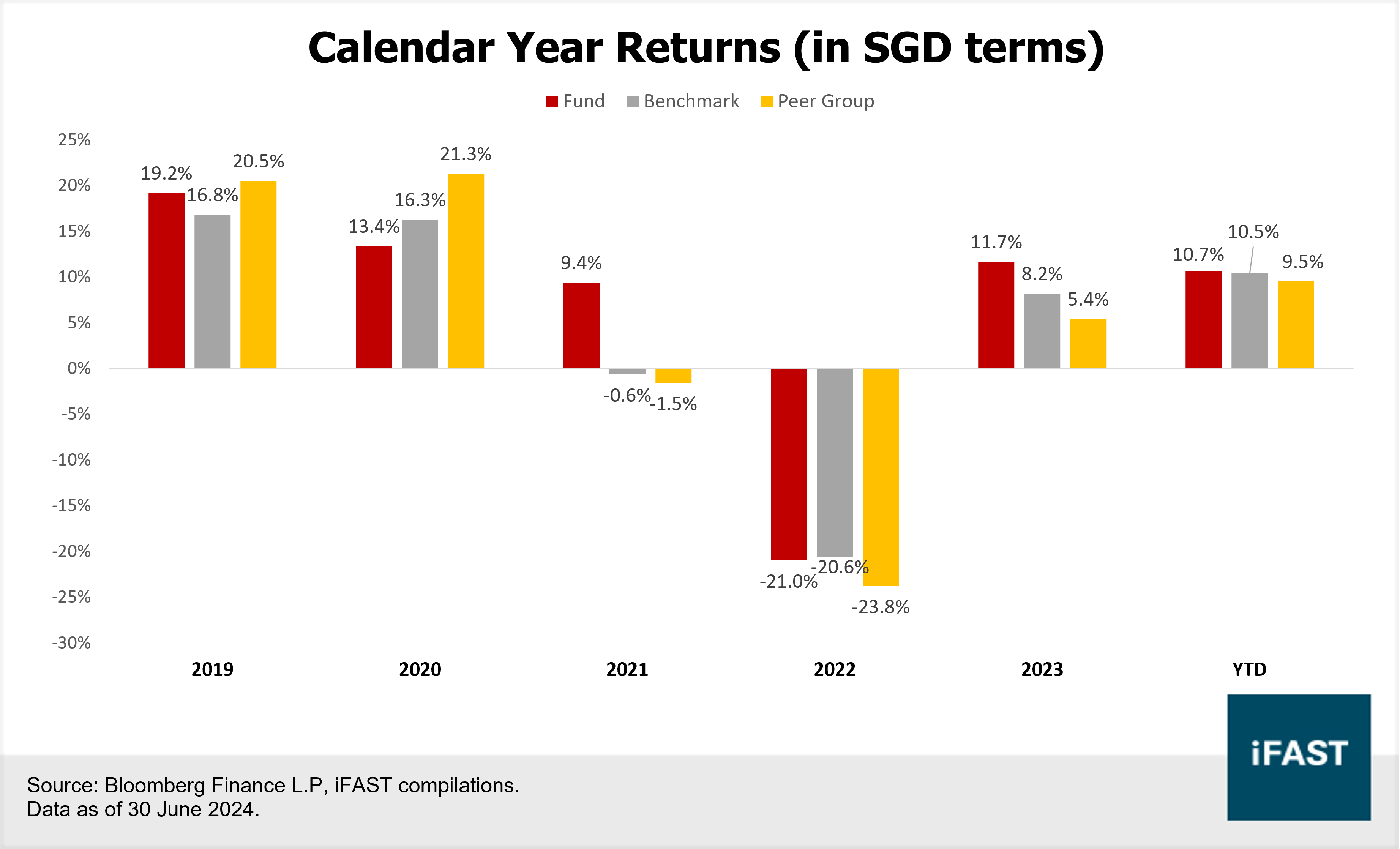

In terms of calendar year performance, the fund has roughly matched the benchmark and peer group in 2019 and 2022, but significantly outperformed them in 2021 and 2023. For instance, while the benchmark posted negative returns in 2021, the fund achieved a robust 9.4% return (Figure 5). The strong performance in these years was largely driven by stock selection.

In 2023, the fund benefited from the semiconductor upcycle and the promising developments in the AI industry. Notable contributions came from investments in semiconductor companies such as TSMC, Novatek Microelectronics, and Samsung Electronics, as well as computer hardware manufacturer Wiwynn. Additionally, the recovery in China, Mexico and South Africa further bolstered the fund's positive returns.

Figure 5: The fund’s calendar year performance shows greater consistency

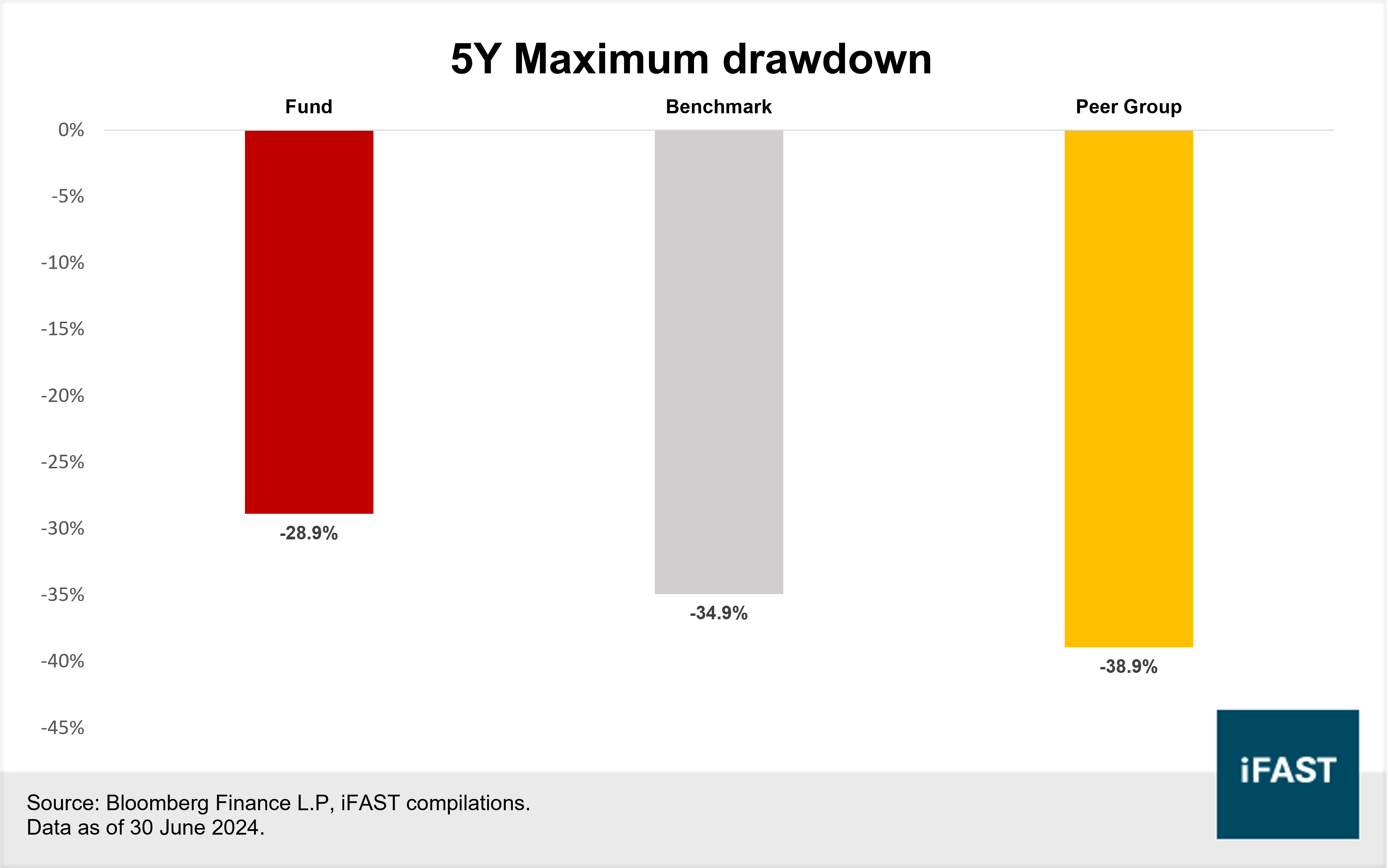

The fund also exhibited a low five-year maximum drawdown of 28.9% (Figure 6), reflecting its effective management of volatility. Overall, its superior performance and reduced drawdown underscore the fund’s strong stock selection and emphasis on high-quality companies.

Figure 6: The fund shows the lowest maximum drawdown compared to both the benchmark and its peer group

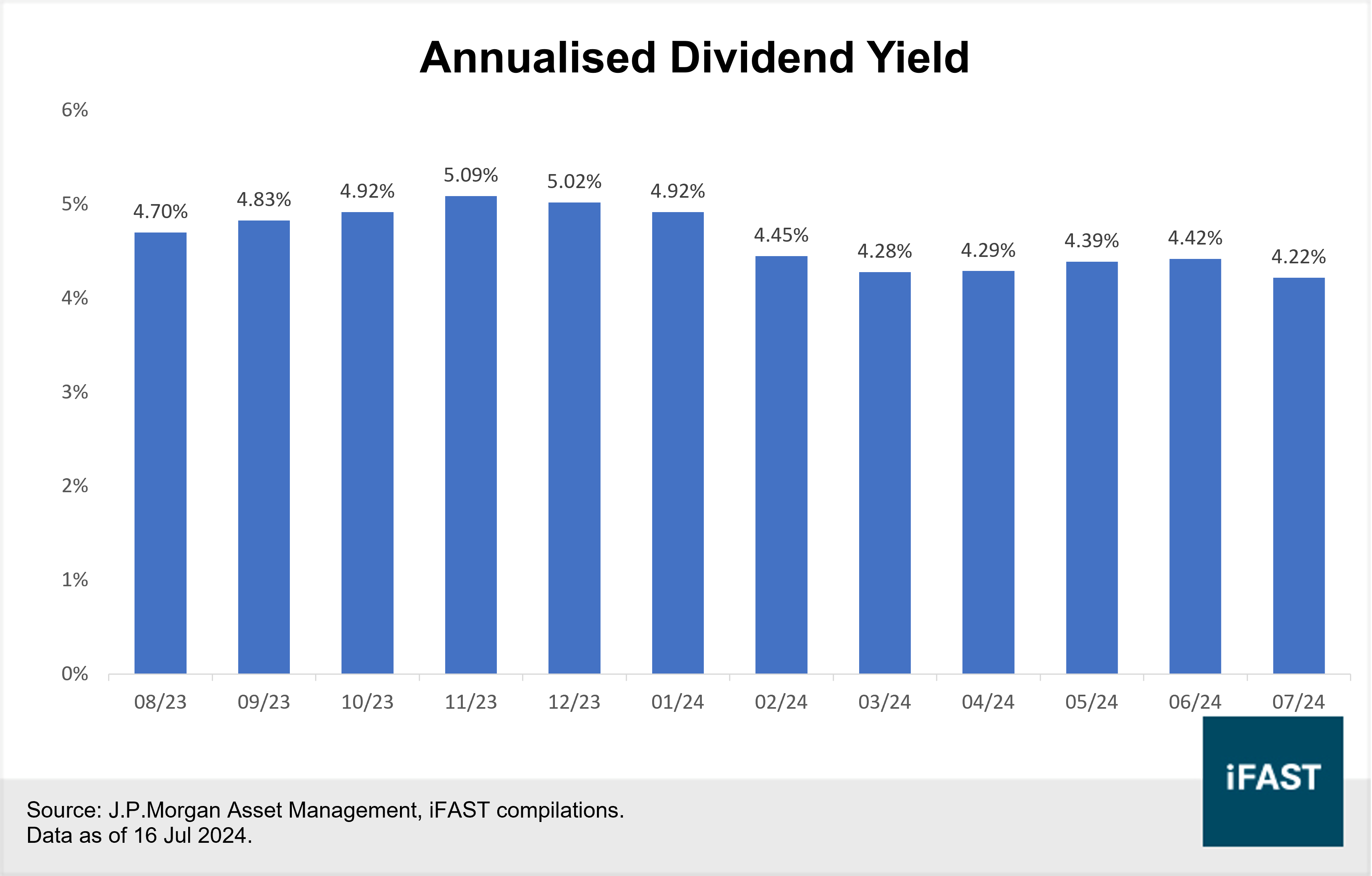

The A (mth) USD share class aims to provide monthly dividend payouts. Over the past year, the fund has delivered an annualised dividend yield ranging from 4.22% to 5.09%. As of 16 July 2024, it paid an annualised dividend yield of 4.22%, significantly outperforming the MSCI Emerging Markets Index, which yielded 2.68%.

Figure 7: The fund offers an annualised dividend yield ranging from 4.22% to 5.09%

Final Thoughts

Investing in volatile markets like emerging markets inherently carries higher risks, which underscores the importance of active management. The JPM Emerging Markets Dividend A (mth) USD has effectively navigated these fluctuations by focusing on high-quality companies, resulting in strong and consistent performance across various timeframes while mitigating volatility. These attributes distinguish the fund from other emerging market funds.

Moreover, the fund’s commitment to delivering regular dividends enhances its appeal by providing investors with a steady income stream and added security in volatile markets. For investors seeking exposure to emerging markets or looking to diversify their portfolios beyond the US and developed markets, we believe the JPM Emerging Markets Dividend A (mth) USD is an appealing choice.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.