- On 27 February 2024, the Nikkei 225 closed at 39,239.52 to set a new all-time high for the third consecutive trading day.

- We have published extensive research on Japanese equities before the substantial market rally, and have previously projected that the index will surpass its 1989 peak. We were right.

- The market rally underpins our confidence that Japan is heading towards firmer grounds. Long-term structural drivers for the market remain in place.

- Using a fair PE ratio of 20X, we project a 2026 target price of 48,000 for the Nikkei 225 Index. This represents an upside potential of 22% as of 27 February 2024.

- There’s still a long runway for Japan’s growth as much of the story is structural rather than cyclical. If you’ve missed the first leg of what is likely to be a multi-year rally, you should not miss your second chance. Seize the opportunities.

After 34 years of pain, the long-awaited resurgence of Japanese stocks is finally here.

On 22 February 2024, the Nikkei 225 Index reached a new record, surpassing its previous peak of 38,915.87 from December 1989 (Figure 1). The upward trend continued on 27 February, closing at 39,239.52 to set a new all-time high for the third consecutive trading day.

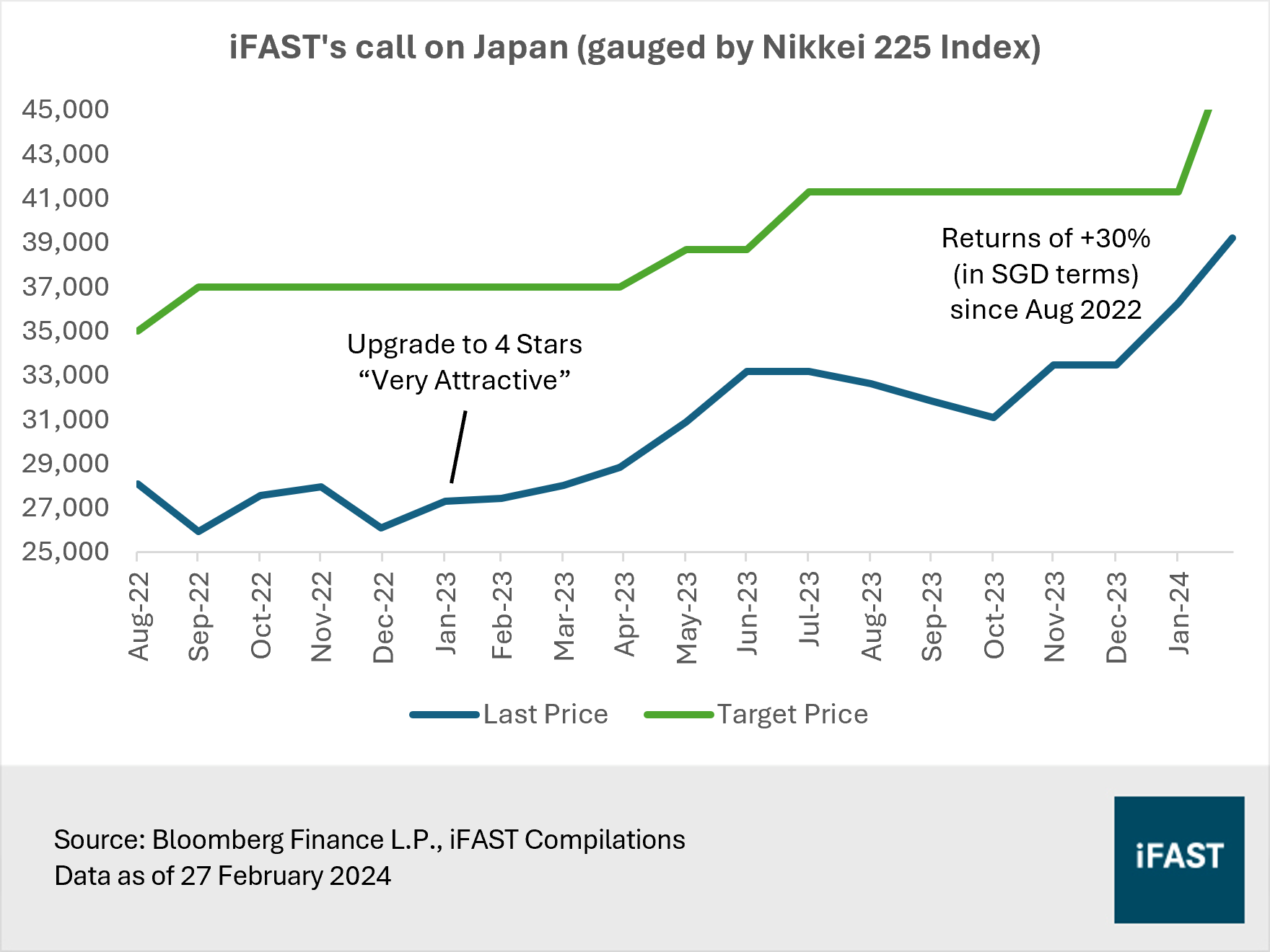

Figure 1: The Nikkei 225 Index recently set a new record

We were right about Japanese equities

We have published extensive research on Japanese equities before the substantial market rally. In fact, we have been bullish on Japan since August 2022, following an improved outlook fuelled by robust corporate earnings from strong pricing power and a weak yen.

Notably, we upgraded the market from 3.5 Stars “Attractive” to 4.0 Stars “Very Attractive” in January 2023. The upgrade was based on our thesis that Japan is one of the few markets still supported by positive factors like a re-opening tailwind and balance sheet strength. In addition, our analysis revealed that at that time, Japanese equities were trading at very cheap valuations.

In July 2023, we included Japan as one of the markets that make up the New Asian Tigers – a group of Asian economies that show significant economic growth and development potential.

As per our last macro update in October 2023, we reiterated our positive view on Japan. Our target price for the Nikkei 225 stood at 41,300 – above the 1989 peak. We emphasised that Japan stands on the brink of significant structural changes, which will serve as the catalyst for the market to reclaim its lost decades of performance. Factors such as the shift towards inflation, corporate governance reforms, and the country’s revival as a semiconductor powerhouse serve as forces propelling share prices to new heights.

Lo and behold, the Nikkei 225 Index soon achieved a new all-time high. The index has also gone up by nearly 30% in SGD terms since the beginning of our call.

Table 1: We have consistently talked about Japan

|

Date |

Title |

|

10 August 2022 |

Japan: Attractive upside with a potential turnaround in 2H22 |

|

5 September 2022 |

|

|

27 December 2022 |

|

|

21 January 2023 |

|

|

21 April 2023 |

|

|

24 May 2023 |

Japanese equities hit a record high. Here’s why it remains our top equity pick |

|

7 July 2023 |

|

|

8 July 2023 |

Who Will Be The Next Asian Tigers? (iFAST Mid-Year Review 2023) |

|

8 July 2023 |

|

|

11 August 2023 |

Don’t miss out on our top investment ideas following Japan’s latest policy tweak |

|

23 October 2023 |

The resurgence of Japan: A new era of multi-year tailwinds with upside potential of 30% by 2025 |

|

21 December 2023 |

Where to put your money? Here are three equity funds you shouldn’t overlook in 2024. |

|

6 January 2024 |

After a 25-year battle with deflation, this time is different for Japan (FSM Invest Expo 2024) |

|

30 January 2024 |

Japanese equities are entering a new era. Here are some stock ideas you can bank on. |

|

13 February 2024 |

Amidst China’s market rout, ride on the rise of the New Asian Tigers with these roaring funds. |

Figure 2: We have been bullish on Japanese equities for some time

Goodbye “Lost Decades”

The market rally reinforces our confidence that Japan is heading towards firmer grounds. Even news that a technical recession occurred in 4Q23 did not stop the momentum. To date, Japanese equities have thrived on further buying from foreign investors and a weak yen. The growing optimism is further driven by corporate governance reforms.

Another reason for Japan’s solid performance is a group of seven companies dubbed by Goldman Sachs as the “Seven Samurai”. Drawing a parallel to the influence of the "Magnificent Seven" on the US stock market, Japan boasts its own version in the form of the "Seven Samurai".

The “Seven Samurai” comprises of semiconductor companies, automakers, and Japan’s largest “sogo shosa” (otherwise known as a trading company). They include Tokyo Electron, Advantest, Screen Holdings, Toyota Motor, Mitsubishi Corporation, Subaru, and Disco. These companies make up a combined weight of 15% in the Nikkei 225 Index as of 31 January 2024. On average, they have returned around 200% in JPY terms (170% in SGD terms) since the beginning of last year due to robust earnings growth.

This time is different for Japan

What lies ahead after this rally? We remain optimistic as long-term structural drivers for Japan remain in place.

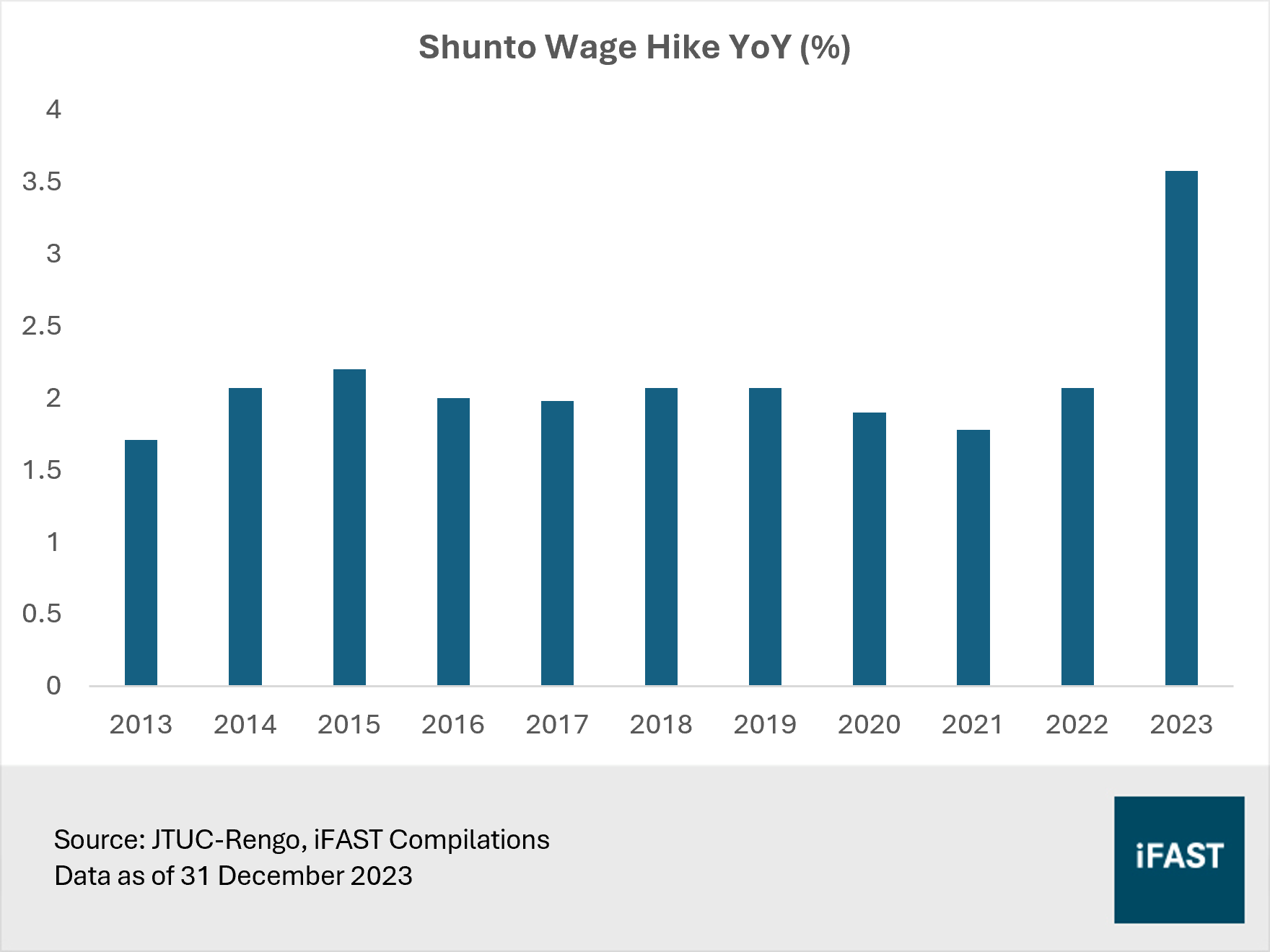

The labour market remains tight compared to historical standards, placing upward pressure on wages. At the same time, annual wage negotiations have kicked off, with companies aiming for wage hikes exceeding last year’s historic gains (Figure 3). The Bank of Japan (BOJ) believes such wage increments would translate into a more meaningful economic spiral, boosting consumer spending. This could help to lift Japan out of a recession.

Figure 3: Wage negotiations saw a sharp surge in 2023

Stronger wage growth also suggests greater certainty that

Japan could really emerge from deflation. Even BOJ Governor Ueda acknowledged

that the probability of achieving the long-term inflation target of 2% is

rising gradually – that’s good news for growth.

Inflation would also motivate domestic investors explore riskier investments in order to protect their asset values, channelling inflows into markets. After frustrating investors for decades, the roaring comeback of the Japanese stock market provides a compelling incentive for domestic investors to shift towards investments.

The Japanese government has also been encouraging more people to start investing with the revamped Nippon Individual Savings Account (NISA) program. From January this year, the investment limit of the NISA has been increased, while the period for tax exemptions on profits made from stock transactions is extended from a maximum of 20 years to an indefinite term.

Meanwhile, Ueda also said that monetary policy would most likely remain accommodative, even after ending negative interest rates. This should provide greater support for Japanese equities.

Moreover, corporate reforms are making progress. As of end December 2023, the Tokyo Stock Exchange noted that 49% of companies listed on the Prime section of the exchange (i.e. the market division with the highest listing standards) have responded to requests to improve their capital efficiency. This marked a sharp increase from the 31% recorded in mid-July. With the trend of share buybacks and dividend hikes expected to continue, investors have the potential to enjoy greater total returns.

Not to mention, the Japanese government has launched initiatives aimed at fostering the growth of its semiconductor industry and to support domestic players. Japan’s technological prowess in semiconductors presents a competitive edge as global companies diversify supply chains amidst the ongoing geopolitical tensions between the US and China, especially over chips. This resurgence as a semiconductor powerhouse serves to reposition the Japanese economy towards a positive growth cycle.

No more false dawns! We firmly believe that this time represents a transformative era for Japan.

A multi-year growth story

Historically, the Nikkei 225 has traded at an average PE ratio of 18X during the “Lost Decades” (Figure 4). Given that Japan is undergoing a structural transformative era, we believe that upgrading the fair PE from the current 18X to 20X is justified. With a fair PE ratio of 20X, we project a 2026 target price of 48,000 for the Nikkei 225 Index, indicating an upside potential of 22% as of 27 February 2024.

Figure 4: Japanese equities have historically traded at a PE of 18X

Furthermore, more than 30% of companies in the Nikkei 225 Index are currently trading below their book value. In contrast, less than 5% of stocks in the S&P 500 have PB ratios below one. As such, even after the rally, Japanese stocks remain relatively inexpensive compared to their US counterparts.

More importantly, despite recent highs for the Nikkei 225, there’s still a long runway of growth for Japan. Much of Japan's growth narrative is rooted in structural factors rather than cyclical – it won’t fade away anytime soon, and will drive the market from strength to strength.

Besides, we believe investors who opt for an unhedged exposure are poised to unlock greater gains. Despite weakness in the yen, we hold a conviction that the currency is set for a turnaround this year. An appreciation of the yen would be driven by the narrowing of yield differentials from additional policy tweaks (and a potential shift) by the BOJ this year in response to a new era of sustained inflation. This is significant as other major central banks conclude their rate hikes and begin exploring potential cuts.

Read more about the Japanese yen here:

Is the yen weakness coming to an end?

The winter is over for the Japanese yen. A liftoff might be in sight

Japanese Yen will be one of the top performing currencies in 2024

In summary, Japan remains as one of our top equity picks. If you’ve missed the first leg of what is likely to be a multi-year rally, you should not miss your second chance. Seize the opportunities.

Long-term investors may take advantage of short-term corrections to build their positions in Japanese equities. Alternatively, discover the benefits of a dollar-cost averaging strategy by opting for a regular savings plan (RSP). Our recommended products are the Eastspring Investments - Japan Dynamic AS SGD and the iShares MSCI Japan ETF (NYSE:EWJ). For active investors who prefer to receive distributions, they may consider the Nikko AM Japan Dividend Equity JPY or Nikko AM Japan Dividend Equity SGD.

Lastly, investors seeking small-cap exposure can look towards the BNY Mellon Japan Small Cap Equity Focus H Acc SGD-H (note that only hedged share classes are available for this fund).

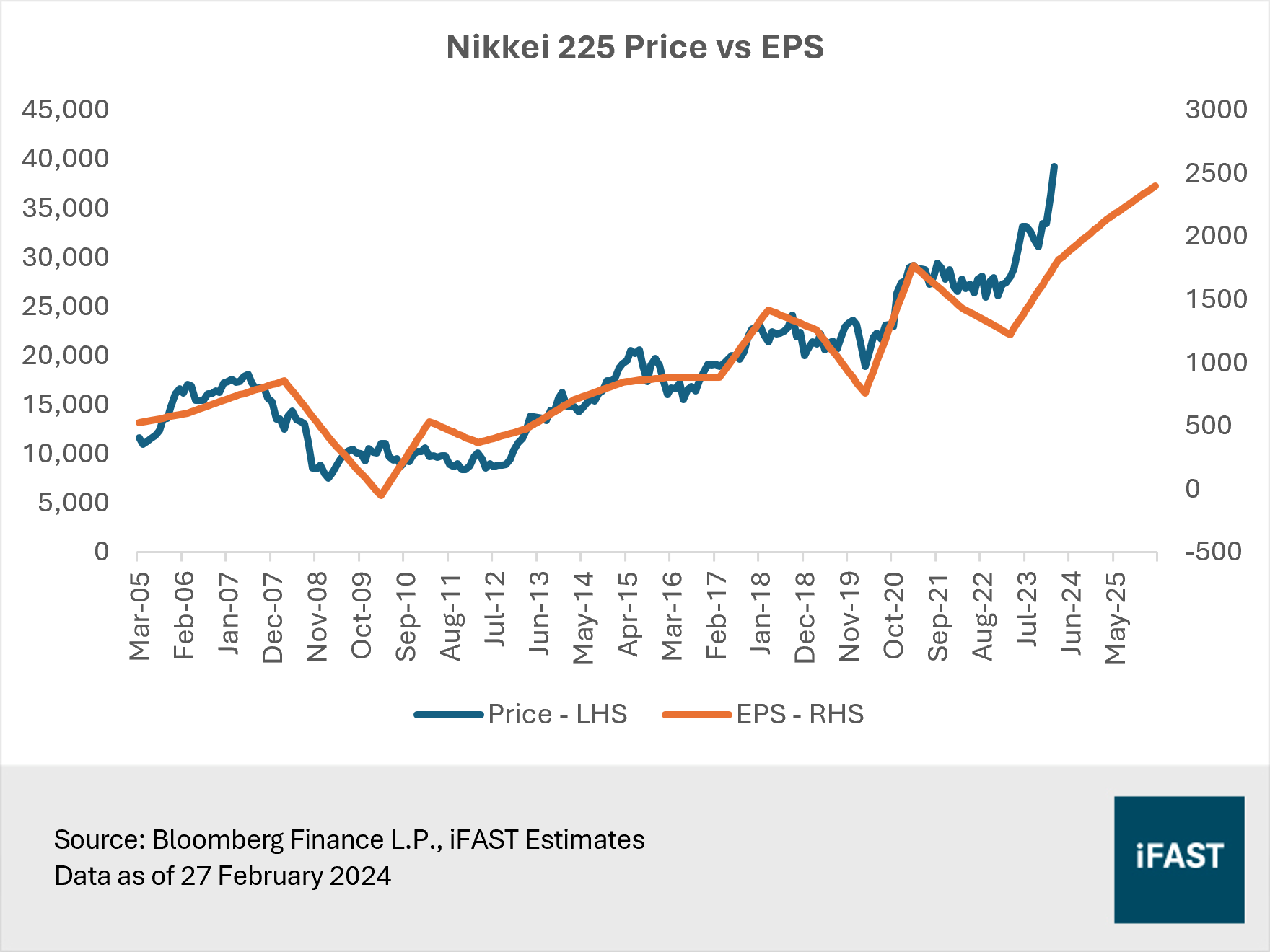

Figure 5: Share prices are driven by earnings

Table 2: Projections for the Nikkei 225 Index

|

Nikkei 225 Index |

2023 |

2024 |

2025 |

2026 |

|

PE Ratio (X) |

27.3 |

21.6 |

18.4 |

16.3 |

|

EPS |

1226 |

1814 |

2135 |

2400 |

|

Earnings Growth |

-14.4% |

48.0% |

17.7% |

12.4% |

|

Target Price (based on 20X fair PE ratio) |

48,000 |

|||

|

Potential Upside |

22% |

|||

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 27 February 2024 |

||||

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.