- Japan is finally getting out of deflation, a longstanding challenge that had hindered its economy. In the long term, the expectations of broader price pressures are likely to result in positive shifts in consumption and investment patterns, helping to spur growth.

- Change is also on the horizon in terms of corporate governance, with many companies motivated to enhance shareholder returns. Long-term corporate profitability will also be boosted as companies can enhance their capital efficiency through investments.

- Japan, with its highly educated and skilled workforce, has excelled in advanced manufacturing, especially in critical sectors like semiconductors. With government support and global collaboration, we believe Japan is set to regain its lost status as a semiconductor powerhouse.

- Using a fair PE ratio of 18X, we have projected a target price of 41,300 for the Nikkei 225 Index by 2025. This projection implies an upside potential of 33% as of 23 October 2023.

The Nikkei 225 has embarked on a remarkable rally, boasting returns exceeding 20% year-to-date (as of 23 October 2023, in local currency terms). The last time the index reached a price level of over 32,000 was more than three decades ago, before the “Lost Decades” – a period marked by prolonged economic stagnation and deflation since the 1990s (Figure 1).

Clearly, a new narrative is unfolding. The Japanese economy recorded robust annualised growth of 4.8% from April to June 2023, while core inflation was up 2.8% year-on-year in September. Japan now stands on the brink of significant structural changes, which we believe will serve as the catalyst for the Japanese equity market to reclaim its lost decades of performance.

Figure 1: The Nikkei 225 remains at a three-decade high

A shift from deflation to inflation

Japan is finally getting out of deflation, a longstanding challenge that had hindered its economy throughout the “Lost Decades”. Inflation is looking stickier with the core consumer price index (CPI), which excludes volatile fresh food costs, staying above the central bank’s 2% target for the 17th consecutive month. Furthermore, core-core CPI, which omits fresh food and energy prices, surged by 4.2% year-on-year in September due to mounting price pressures in the service sector (Figure 2).

Figure 2: Service prices tend to reflect wage growth

An uptick in service prices, which tend to reflect domestic

wage trends, hints at the potential for broader price pressures in Japan. Meanwhile,

we believe that calls for stronger wage growth, coupled with the shrinking

working age population in Japan, will exert upward pressure on wages (Figure 3).

As we look ahead, the annual shunto – which are wage negotiations between major

corporations and unions that take place during spring – is anticipated to sustain

this year’s robust growth, and remain higher compared to long-term historical

levels.

Figure 3: Japan is facing a shrinking labour pool

Historically, falling prices in Japan provided an incentive to delay consumption and investments, which restrained economic growth. It is also worth highlighting that cash holdings represent over 50% of household assets as consumers have held on tightly to their savings over the years in response to deflation. However, in the long term, the expectations of broader price pressures are likely to result in positive shifts in consumption and investment patterns from both consumers and businesses, helping to spur growth. Inflation would also motivate domestic investors explore riskier investments in order to protect their asset values, channelling inflows into the capital markets.

Furthermore, we reckon that sustained inflation would compel the Bank of Japan (BOJ) to review its yield curve control (YCC) policy. Officials are paying close attention to next year’s shunto wage negotiations, where strong data would bolster the BOJ’s confidence that inflationary pressures are sustainable.

Efforts to boost shareholder returns

The “Lost Decades” had also instilled a culture of heavy capital accumulation among corporations. Unfortunately, this approach often came at the expense of shareholders’ returns. Over 30% of non-financial companies in the Nikkei 225 Index maintain net cash positions, a figure significantly higher compared to their counterparts in developed markets (DMs) (Figure 4). This accumulation of cash on corporate balance sheets has, in many instances, resulted in low return on equity (ROE) figures and price-to-book (PB) ratios below one (Figure 5).

Figure 4: Japanese corporates (ex-financials) are cash heavy

Figure 5: Japan lags DM peers in capital efficiency ratios like ROE

Change is on the horizon. The Tokyo Stock Exchange (TSE) issued a mandate in March 2023, calling most listed companies, especially those trading below book value, to account for their cost and efficiency of capital. Supported by robust earnings, many companies have been motivated to enhance shareholder returns through share buybacks and dividend hikes. According to Nikkei forecasts, dividends to be paid by Japanese companies during the fiscal year ending March 2024 will reach a new record of JPY 15.2 trillion.

In this wave of transformation, corporate giants like Mitsubishi Corp and Toyota Motor Corp have been stepping into the spotlight. Mitsubishi Corp has pledged to repurchase up to 6% of its shares, amounting to JPY 300 billion, from May 2023 to the end of the year. Simultaneously, Toyota Motor Corp disclosed plans to buy back shares worth up to JPY 150 billion.

However, we note that beyond these prominent names, the majority of companies listed on the Prime section of the TSE (the market division with the highest listing standards) have yet to outline concrete strategies. In our view, the TSE’s call for companies to disclose long-term plans to improve capital efficiency represents a pivotal step in the right direction. We recognise that companies are unlikely to hastily formulate strategies overnight in order to avoid making premature decisions.

In addition to share buybacks and dividend hikes, companies possess an array of tools to enhance their capital efficiency, including (i) expanding investments in research and development (R&D), (ii) investing in equipment and facilities, and (iii) restructuring their business portfolios. These strategic measures hold the potential to boost long-term corporate profitability. As a result, we view corporate governance reforms as a sustained long-term tailwind for sustainable growth, rather than a fleeting, short-term catalyst for the Japanese equity market.

Ongoing revival as a semiconductor powerhouse

Japan, with its highly educated and skilled workforce, has long excelled in advanced manufacturing, especially in critical sectors like semiconductors. In the 1980s, Japanese semiconductor manufacturers dominated the global stage, contributing to over 50% of world production. However, during the “Lost Decades”, Japan’s chip industry lost ground to foreign competitors like Taiwan, South Korea, and China. Today, while Japanese chipmakers trail behind global chip giants like TSMC and Samsung, it remains internationally competitive in the production of simpler chips utilised in automobiles, household appliances, and consumer goods.

Recognising the importance of regaining a strong foothold in the global semiconductor marketplace, the Japanese government has launched initiatives aimed at fostering the growth of its semiconductor industry and support domestic players. These efforts also encompass collaborations with the US and Europe, geared toward attracting semiconductor investments on Japanese soil.

One major initiative involves a consortium composed of eight major Japanese companies – Toyota, Denso, Sony, NTT, NEC, SoftBank, MUFG Bank, and Kioxia. We note that Sony and Kioxia are key players in Japan’s semiconductor industry. Kioxia, formerly known as Toshiba Memory Corporation, holds a pivotal position in the global semiconductor arena, particularly in the field of NAND flash memory and solid state drivers (SSDs). Meanwhile, Sony holds a significant presence in the semiconductor industry, producing image sensors which are widely used in cameras and mobile devices. Together with the Japanese government who has committed billions of yen, they established a semiconductor manufacturer called Rapidus (Figure 6).

Rapidus, in partnership with IBM Research in the US, is working towards developing two-nanometre technology by 2027, with plans for fabrication in Japan. Rather than competing directly with global chip giants that produce large volumes of all-purpose chips, this strategic partnership is focusing on pioneering specialised chips, such as artificial intelligence (AI) chips with low power consumption. This approach is set to re-establish Japan’s prominence in the global semiconductor landscape. Besides, this initiative gains even more significance amidst the ongoing geopolitical tensions between the US and China, especially over chips. The partnership between Rapidus and IBM would create a semiconductor supply chain that is less dependent of China.

Figure 6: Rapidus and IBM have formed a strategic partnership

Speaking of which, Japan’s technological prowess in semiconductors presents a competitive edge as global companies diversify supply chains away from China. For instance, Japan is a favoured location for TSMC’s overseas expansion, with the chip giant is considering adding capacity and another fab in the country. Such an expansion by TSMC would not only boost Japan’s efforts to regain its lost status as a semiconductor powerhouse, but also help to strengthen the semiconductor supply chain in Japan. We also note that Japan’s pivotal automotives and electronics industries rely on a stable, long-term supply of chips for growth.

Key investment risks

Ageing population: The shifting demographics in Japan, primarily driven by its ageing population, could impact consumer spending patterns as there is a tendency for older individuals to save more and spend less. Nonetheless, over the long term, we expect to see the export of semiconductors to play an increasingly important role in driving Japan’s economic growth. This also reduces the reliance on private consumption as a main driver of growth.

Nikkei 225 to reach over 40,000 by 2025

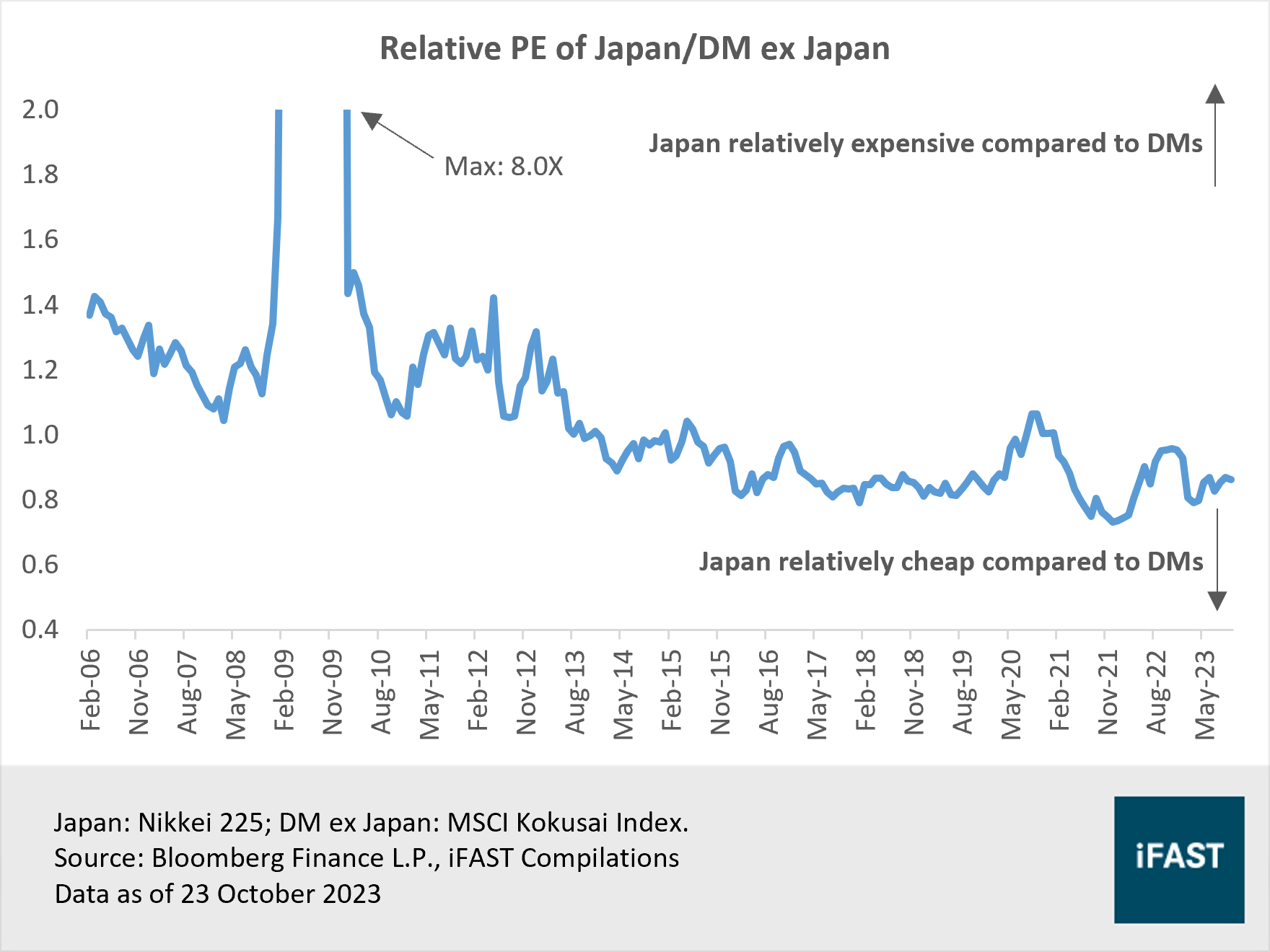

In light of a confluence of factors mentioned above, we anticipate Japanese corporates to deliver promising earnings outlook. Furthermore, the Japanese equity market remains attractive from a valuation standpoint. The forward PE of the Nikkei 225 currently stands at a 10% discount to its long-term average since 2005. Japan also trades at relatively undemanding valuations compared to DM peers (based on the MSCI Kokusai Index which gauges the equity performance of DMs excluding Japan; Figure 7).

Figure 7: Japan’s valuations are undemanding

Using a fair PE ratio of 18X, we have projected a target price of 41,300 for the Nikkei 225 Index by 2025. This projection implies an upside potential of 33% as of 23 October 2023. Our optimism is underpinned by a solid long-term investment case for Japan, driven by several factors like the ongoing shift towards inflation, corporate governance reforms, and Japan’s resurgence as a semiconductor powerhouse. In addition, renewed interest from both domestic and foreign investors would drive capital flows, propelling share prices to new heights. These positive dynamics should also outweigh the impact of a stabilising or strengthening yen on Japanese corporates.

Figure 8: Nikkei 225 Index Price vs EPS

Table 1: Projections for the Nikkei 225 Index

|

Nikkei 225 Index |

FY2022 |

FY2023E |

FY2024E |

FY2025E |

|

PE Ratio (X) |

19.8 |

18.5 |

15.3 |

13.6 |

|

Earnings Per Share |

1,316 |

1,684 |

2,030 |

2,292 |

|

Earnings Growth |

-24.3% |

28.0% |

20.5% |

12.9% |

|

Target Price (based on 18X fair PE ratio) |

41,300 |

|||

|

Potential Upside (%) |

33% |

|||

|

Source: iFAST Estimates, Bloomberg Finance L.P. Data as of 23 October 2023 |

||||

Table 2: Recommended products for Japan

|

|

Unit Trust |

ETF |

|

Japan |

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.