-

The -20% correction in China equities after Chinese New Year was largely sentiment-driven; fears of (i) the possible tightening of financial conditions in China and (ii) the rising regulatory scrutiny (both domestic and external) on the Chinese Technology sector unnerved investors.

We argue that the recent correction in Chinese equities is a positive development for the market over the longer term – a healthy way of skimming some of the froth in the property and financial markets.

Despite mounting risks, we believe they are easily offset by the robust drivers of China equities. The first set of economic prints this year have been promising, signifying the V-shaped recovery in economic activities within China remains well underway.

The market rout has knocked valuations back towards our fair value level of 14.5X. We believe that valuation has now reset to a healthy level, coupled with robust double-digit earnings growth ahead, setting set the stage for outperformance in Chinese equities ahead.

In light of the emerging risks, we reduced our star rating for China equity market to 4.0 stars (from 4.5 stars) but continue to reiterate our 'Highly Attractive' recommendation.

What caused the rout in China equities? Should our investors sell their holdings?

Like many other major equity markets, China equities market was not spared from the global stocks rout that arose from the rising US Treasury bond yields. Both onshore and offshore China equities tumbled after the Lunar New Year, erasing the impressive run-up in prices since the start of the year.

The MSCI China Index, our representative benchmark for China, fell by almost 20% from its peak in mid-February, thanks to the outsized presence of growth stocks (i.e. Alibaba and Tencent) within the index. Growth-oriented sectors – Consumer Discretionary and Technology – saw the biggest drawdown amidst the correction, partly due to their heady valuations and profit-taking by investors, given growth stocks’ stellar performance since 2nd quarter last year.

(Read more: Key reasons for the sell-off in Chinese equities and why you should stay the course)

Arguably, the sharp correction in China equities was largely sentiment-driven; fears of (i) the possible tightening of financial conditions in China and (ii) the rising regulatory scrutiny (both domestic and external) on the Chinese Technology sector weighed heavily on investors’ confidence, shattering the exuberance for Chinese equities at the start of the year.

Despite piling headlong into Chinese equities just three months ago (MSCI China Index surge close to 20% in mere weeks) – leading to a crowded positioning – the emergence of the Tech regulatory and monetary policy risks factors has clearly unnerved investors, sending them scrambling for an exit.

Chart 1: China equity indices plunged after the Lunar New Year

Has China equities lost its lustre in face of such mounting risks? We think not.

In our view, investors’ fears are overblown.

While we recognise the possible impacts of mounting regulatory and monetary policy risks ahead, particularly the regulatory overhang on China’s tech sector, we also believe the risk factors are easily offset by the robust drivers of China equities.

For one, China’s economic growth outlook remains bright ahead. After all, China started the year on stronger economic footing than the rest of the world. Demand for Chinese goods is also set to benefit from the stronger global economic backdrop and faster-than-expected re-openings globally due to mass vaccination programs. Secondly, we believe Chinese policymakers will take a moderate policy stance to support a sustained recovery in consumer spending, which entails holding policy rates at current level but gradually tighten credit growth. Lastly, while Beijing’s tightening leash on its Internet titans (i.e. Alibaba, Tencent, Baidu) is indeed troubling, this is not unprecedented – these tech players have emerged stronger each time.

Earnings growth will be a major driver for China equities ahead. Despite GDP growth being over 2% last year, corporate earnings lagged the recovery, registering a minor contraction of -7% in 2020. Low base effect coupled with robust economic outlook mean that we can expect earnings growth to be robust ahead – FY21 (+25.3% YoY) and FY22 (+19.0% YoY).

At the same time, we argue that the recent correction in Chinese equities is a positive development for the market over the longer term. We see the sell-off as a healthy way of skimming some of the froth in the property and financial markets, paving the way for the growth catalysts to drive momentum in the Chinese market ahead.

China’s Economic Growth Outlook Remains Bright Ahead

China has had a strong start to the year, on the back of robust export growth momentum in 2nd half of 2020. Export strength has been resilient in the first quarter this year, enabling industrial production to accelerate to above pre-Covid growth rate, while consumer health is also on track for solid rebound.

The first set of economic prints have been promising: the cumulative Jan-Feb growth of Industrial Production, Retail Spending and Fixed Asset Investments have risen by more than 30% compared to last year – albeit due to the extreme low base effect in early 2020 when the Covid-19 pandemic struck China most badly. PMI remains within the expansionary territory, despite showing sign of moderating across recent months (Chart 2 and 3).

While the readings are likely to moderate towards more reasonable levels, we still think recovery in economic activities within China remains well underway; the economy is on track to meet our GDP growth expectation of 8.5% this year.

Chart 2: The promising first set of economic prints signifies that recovery in activities within China remains well underway.

Export outlook in 1H21 continues to be rosy, despite the resurgence in Covid-19 cases in parts of China. Its domestic virus situation remains well-managed, enabling the production of export goods to return to normal production capacity after the festive season. This stands in contrast to rest of the world, where Covid-19 related production disruption in many countries continue to engender the shifting in new orders to Chinese producers in the near-term.

Further ahead, demand is also set to receive a boost from a stronger global economy, especially with the fiscal impulse from the USD 1.9 trillion stimulus package set to invigorate US growth. Overall, we expect to see solid double-digit annual growth in China’s export sector across 1H21, followed by moderation in the 2nd half of the year.

Chart 3: PMI remains within the expansionary territory, despite showing sign of moderating across recent months.

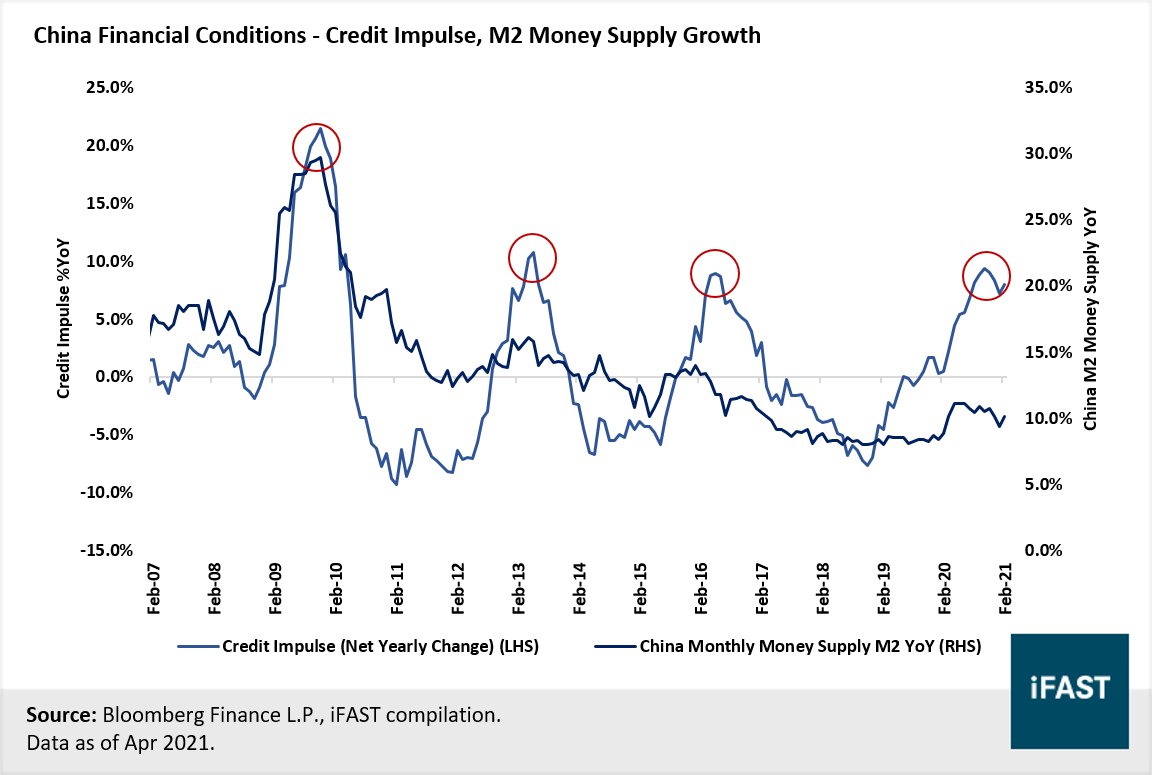

Loose monetary stance days are over, but we expect tapering to be gradual

In recent meetings, Chinese policymakers adopted a more cautionary tone and expressed their intention to rein in risks of over-leveraging and asset bubbles within its financial system and real estate market.

Coupled with a possible infection point in credit impulse (measured via growth in Total Social Financing (TSF) – credit growth driven by fiscal stimulus) and sliding growth in M2 money supply, the days of loose monetary policy are seemingly behind us (Chart 4).

Perhaps the bigger fear of the two (Tech regulatory & monetary policy risks), investors were particularly unnerved by the possible tightening of financial conditions within China. Investors are rightfully concerned; a premature rate hike can weigh on valuation re-ratings and earnings growth trajectory ahead.

However, we believe risks are low for a drastic tightening in monetary conditions, instead China is more likely to approach policy normalisation via gradual tapering of its fiscal and monetary stimulus.

We believe People's Bank of China (PBOC) will hold interest rates steady for much of the year; the Loan Prime Rates were kept unchanged in March for the 11th consecutive month. Conditions remain conducive for PBOC to maintain rates at current level: inflation prints continue to display no signs of overheating, amid sluggish household consumption.

More importantly, the shift in financial conditions from accommodative to a more neutral stance does not necessarily mean that China’s growth will slow. After all, the Chinese economy may not need additional stimulus – leading indicators continue to point to the steady economic growth momentum for this year.

Chart 4: Cautionary tone of bank regulators and inflection point in credit impulse suggest that the days of loose monetary policy are behind us.

Robust Earnings Growth The Major Driver For Chinese Equities In 2021

Unlike

last year where the stellar performance in MSCI China Index was driven almost

entirely by valuation expansion, investors will need earnings growth to deliver

in 2021 for any hopes of a sustained rally in China equities (Chart 5).

Thankfully, we expect earnings growth to be robust ahead – FY21 (+25.3% YoY) and FY22 (+19.0% YoY). Despite GDP growth being over 2% last year, corporate earnings have lagged the recovery, registering a minor contraction of -7% in 2020. Thus, we believe the low base effect coupled with robust economic outlook should set the stage for solid earnings in Chinese equities in the next two years.

Chart 5: With MSCI China Index driven almost entirely by valuation expansion last year, investors will need earnings growth to deliver in 2021.

Part of our optimism for a strong earnings growth trajectory in Chinese equities this year is due to its high domestically derived exposure of more than 80%. This is unusually high when compared to other major emerging markets and developed markets. Hence, a robust economic growth for China directly translates into top-line and bottom-line growth for Chinese companies.

With China’s leading market indicators (e.g. new PMI orders, industrial inventories and industrial profit growth) continue to recover sharply in 1st quarter this year, we are optimistic for index EPS to catch up across the year (historically lagging the leading indicators by 6-9 months) (Chart 6).

Sector-wise, the major components – Consumer Discretionary, Technology and Financials – are also displaying robust signs of earnings recovery. For China banks, the easing loan loss provisions and double digit loan growth are expected support a healthy rebound in earnings – high single digit growth of 7-9% of the big four banks in FY21-22. Index heavyweights – the Internet giants Tencent and Alibaba are expected to generate more than 20% growth in EPS for this year and next as well, despite the ongoing regulatory troubles.

(Read More: Earnings recovery and new re-rating catalysts to boost share prices of China’s Big Four banks)

Chart 6: EPS growth to catch up with the impressive ascent of the China’s leading indicators

Upside Potential in excess of 20% after Valuation Reset

While Chinese equities were trading at heady valuations in mid-Feb, the subsequent market rout knocked valuation back towards our fair value level of 14.5X. We believe that valuation has reset to a healthy level, paving the way for stronger price momentum within the Chinese equity market ahead (Chart 7).

Applying our fair PE ratio of 14.5X on FY23E earnings estimates, we derived a target price of 139 for MSCI China Index by end-2023. This represents an upside potential of 25% by end 2023 – one which we think the market could easily achieve earlier than predicted.

Overall, we acknowledge that the attractiveness of China equities has been taken down a notch due to the emergence of regulatory risk and policy risk. But with growth drivers largely intact, China’s robust economic growth, equity earnings growth alongside its reasonable valuation gives us the confidence that this market is well-positioned to outperform global equities this year.

We reduce our star rating for China equity market to 4.0 stars (from 4.5 stars) but continue to reiterate our 'Highly Attractive' recommendation.

We believe that the recent market correction presents an opportunity for investors to accumulate more exposure toward the Chinese equities on the cheap, especially for investors still light on positioning in this market.

Recommended products for exposure to China

|

Category |

Products |

|

Actively Managed Fund |

|

|

Passive Tracking ETF |

Table 1: Upside Potential of China equities by end-2022

|

MSCI China Index |

FY2020 |

FY2021 |

FY2022 |

FY2023 |

|

PE ratio (X) |

19.0 |

15.2 |

12.8 |

11.6 |

|

Expected earnings growth (YoY %) |

-7% |

25% |

19% |

10% |

|

Earnings Per Share (EPS) |

5.8 |

7.3 |

8.7 |

9.6 |

|

Projected fair price (Based on 14.5X Fair PE ratio) |

84.8 |

106.2 |

126.2 |

139.2 |

|

Potential upside (%) |

- |

- |

- |

25% |

|

Source: Bloomberg Finance L.P., iFAST estimates. Data as of Apr 2021. |

||||

Chart 7: Valuation has reset to a healthy level, paving the way for further price momentum ahead

Chart 8: China equities promises 25% upside potential by end-2023

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.