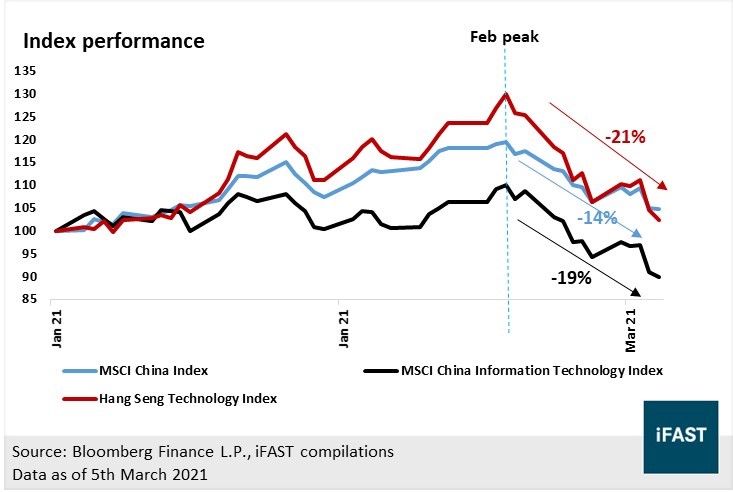

Amid the meltdown in global markets witnessed lately, Chinese equities were not spared. The MSCI China Index, a representative benchmark for both onshore and offshore Chinese equities, saw a significant monthly decline in February. Like other major equity markets, growth oriented sectors such as Consumer Discretionary & Technology saw the biggest drawdowns. The peak-to-trough for Chinese equity indices as well as some of the growth-oriented funds does not look pretty. So what’s next for Chinese equities? Will the selling continue?

Chart 1: Chinese equities suffer a major setback as the tech sell off echoes around the world

In the following sections, we will delve deeper into some of the likely reasons triggering the violent de-risking seen, as well as our view on Chinese equities for the year ahead.

Anatomy of the sell-off

Valuations are not often the catalyst for major moves in financial markets. Expensive assets may become even more so, and vice versa. Rather, frothy valuations were the metaphorical tinder-dry that set up the conditions for the sell-off. Many investors were expecting 2021 to be a big year for China (due to their effective handling of the coronavirus situation), as they piled onto the Chinese equities, which consequently became a crowded positioning.

One probable catalyst, aside from the selling momentum experienced globally, could have been due to investors’ realisation of Chinese policymakers’ desire to keep its house in order. Reducing leverage, and improving the use of capital within its economy and the financial system, remains one of the country’s top priority. Since the start of the year, the nation’s top policymakers have issued statements and actions that have done little to assuage market participants.

[See: China 'worried' about bubbles in property, foreign markets, says bank regulator (Straits Times), China's benchmark overnight repo rate jumps to highest since Nov 2019 (Reuters), & Hong Kong raises stock-trading tax for first time since 1993 (Asia Nikkei)]

The series of events highlighted in the articles above suggest that policymakers are pre-empting to remove some of the froth that is forming around its property and financial markets. When taken all into account (property tightening measures, peaking growth of broad money supply growth, and rising interbank bank repo rate), it does not provide confidence to investors regarding the timeline of which China’s policymakers plan on tightening its monetary policy.

Why growth oriented stocks saw the largest drawdown

Firstly, valuations of the tech sector have become extremely expensive as a result of the massive run up in stock prices since March last year. Even after accounting for the sell-off, the MSCI China Information Technology index continues to trade at a forward P/E of 29x, implying that it would take approximately 29 years for the company to earn back the amount paid for each share. Such long duration growth assets are naturally more sensitive to changes in interest rate expectations, making it a prime target for a sell-off.

(See: Growth opportunities are growing scarcer. Thematic investing can help alleviate that problem)

Secondly, with the current economic recovery resilience, we opine that market participants are rotating out of growth oriented names into cyclical and cheaper sectors such as financials as the reflation trade narrative shifts a gear higher.

(See: Inflation risk on the horizon? Strategies for rising inflation)

Our view on the recent sell-off

On the contrary, the drawdown in Chinese equities is a positive development for Chinese equity markets over the longer term. The removal in valuation froth ensures that the bull market in China remains in check. We continue to favour Chinese equities moving ahead as we see 3 main reasons that will drive growth in the country’s equities

1. Strong earnings growth trajectory

China corporates (gauged by the MSCI China index) has a revenue exposure of roughly 87% derived domestically, a staggering concentration when comparing to other major Emerging Markets (Ems) and Developed Markets (DMs). Therefore, we think a robust economic growth for China translates into relatively stronger broad-based improvements in earnings for Chinese companies. In the current environment where growth is healthy, we believe that domestic demand will continue to thrive and consumption should remain strong.

2. Gradual pivot towards an economic model driven more by consumption and tech

With China’s dual circulation strategy, we expect the theme of ‘Consumption Upgrade’ and ‘Technology’ to serve as one of the twin engines for China’s long-term economic growth momentum. Therefore, sectors (i.e. Technology and Consumer Discretionary) providing exposure to these long-term growth themes in China are slated to benefit from China’s long term growth strategy.

3. China remains on track to be the largest economy by the end of this decade

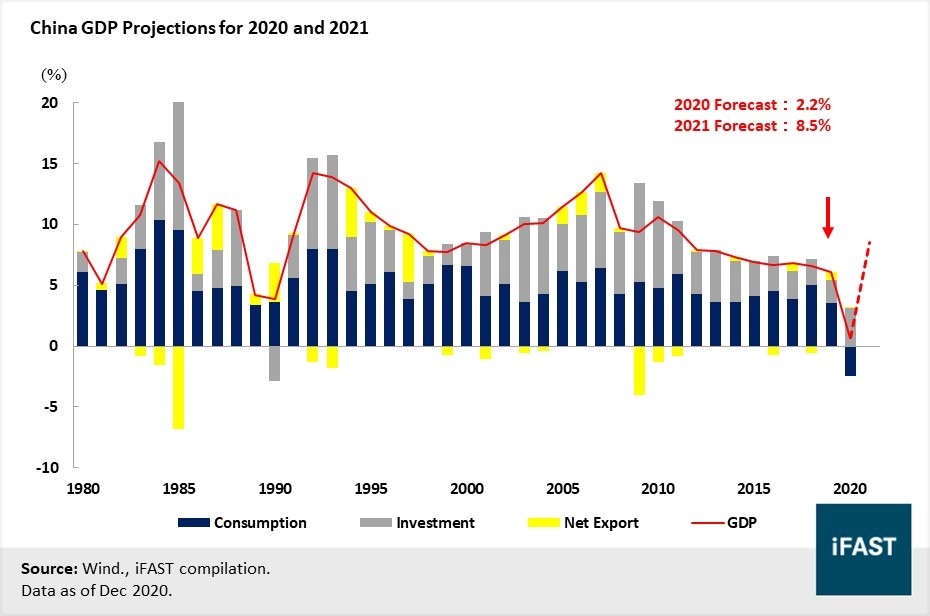

Peering ahead, our team’s forecast for China’s real GDP growth for 2021 is +8.5% – highest among major economies. Such robust growth prospects are stacked on top of over 2% growth in 2020, while the rest of the world contracted due to Covid-19. Based on our calculations, our bold prediction is that China's GDP will surpass the United States in 2026 – potentially taking over the mantle as the world’s largest economy within the next 5 years. This is expected to bode well for corporate earnings in the years ahead.

Chart 2: A big rebound in GDP growth is expected for China in 2021

Chart 3: Chinese companies have high domestic revenue exposure; its strong domestic growth should keep earnings growth healthy

Stay invested

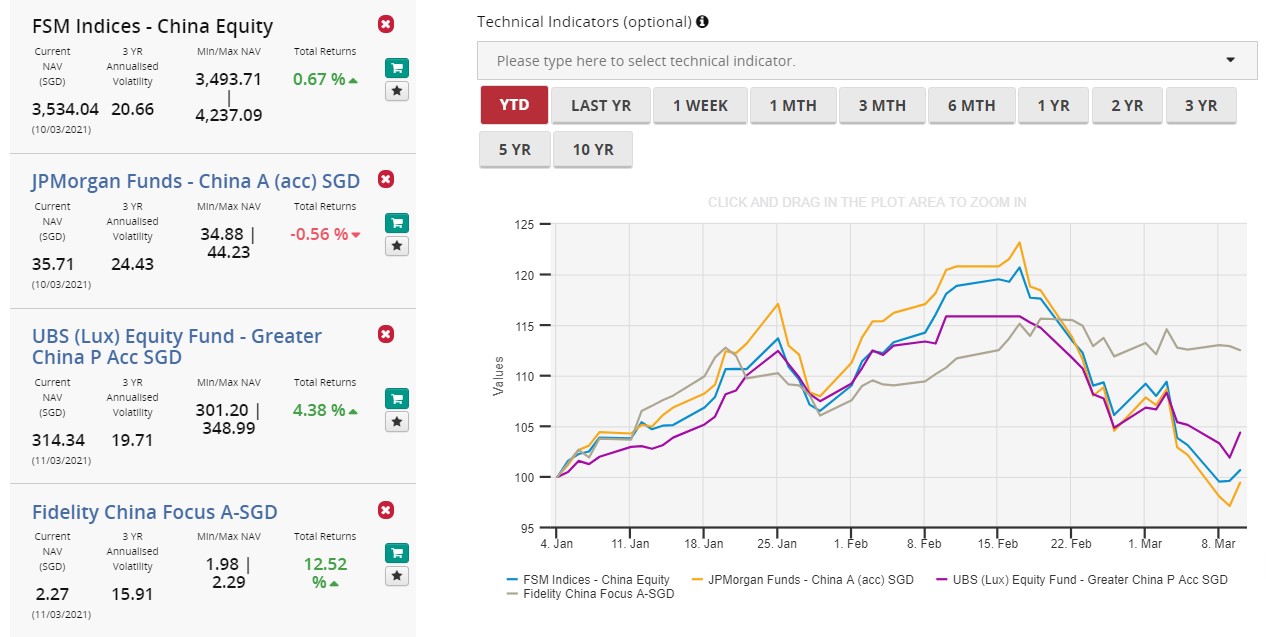

We think new investors are mistaken if they decide to sell and take a loss now. Regardless of what happens in the interim, Chinese equity markets remain a bright spark over the long term given their current economic trajectory. Fidelity China Focus Fund, our previously recommended Chinese equity fund, is a value-oriented strategy that has managed well despite the market sell-off

Its exposure towards old-economy stocks have allowed investors to weather the souring market narrative better, primarily due to the fact that such stocks’ performance tend to be positively correlated with growth & inflation expectations, and that these stocks are also generally cheaper, and thus have less room to fall.

Figure 1: Fidelity China Focus Fund largely escapes a washout in the wider Chinese equity market

Source: iFAST Singapore

Accessed on 11 March 2021

While some of our recommended Chinese equity funds such as the UBS (Lux) Equity Fund - Greater China P Acc SGD, JPMorgan Funds - China A (acc) SGD, and Allianz China A Shares AT Acc SGD have suffered a considerable beating just shortly entering into the new year, we continue to favour these growth-oriented funds given the long term trends they are investing and positioned for.

(See: Fund Friday: Where will China's next leg of growth be? The answer lies in its domestic consumers.)

Through this event, it would be a timely reminder for investors that experiencing losses is part and parcel of investing. Equity markets do not move in a single straight line. Volatility is the cost of admission to building wealth via capital markets.

We always advocate investors to consider a regular-savings-plan (RSP) strategy to smoothen out the volatility that comes with investing in riskier markets like China. RSP helps with removing emotions out of the game and ensuring that investors do not get caught out by investing too much at the wrong time.

What matters is that one continues to make regular contributions to your investment portfolio to increase your odds for investment success. So long as you are not overstretching your day-to-day finances just to invest, then the wisest thing to do would be staying the course and accumulating on dips along the way.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.