- Inflation and interest rates will remain elevated for an extended period. Disinflation in the US has been slow and challenging, while in the EU, the rate-cutting process is expected to be very gradual.

- The Bank of Japan expects long-term inflation to gradually reach its 2% target, driven by rising wages and prices. Along with structural drivers like improved corporate governance, Japan’s equity market likely has strong growth potential.

- We've warned that China's rally isn't sustainable. Chinese equities are faltering amid rising trade tensions and a worsening property market slump.

- Beijing plans retaliatory tariffs on EU sectors like agriculture and automotive, risking supply chain disruptions and complicating global inflation control efforts.

Central bank decisions: Cutting rates or holding steady?

Once again, we stress that inflation and interest rates will remain higher for longer.

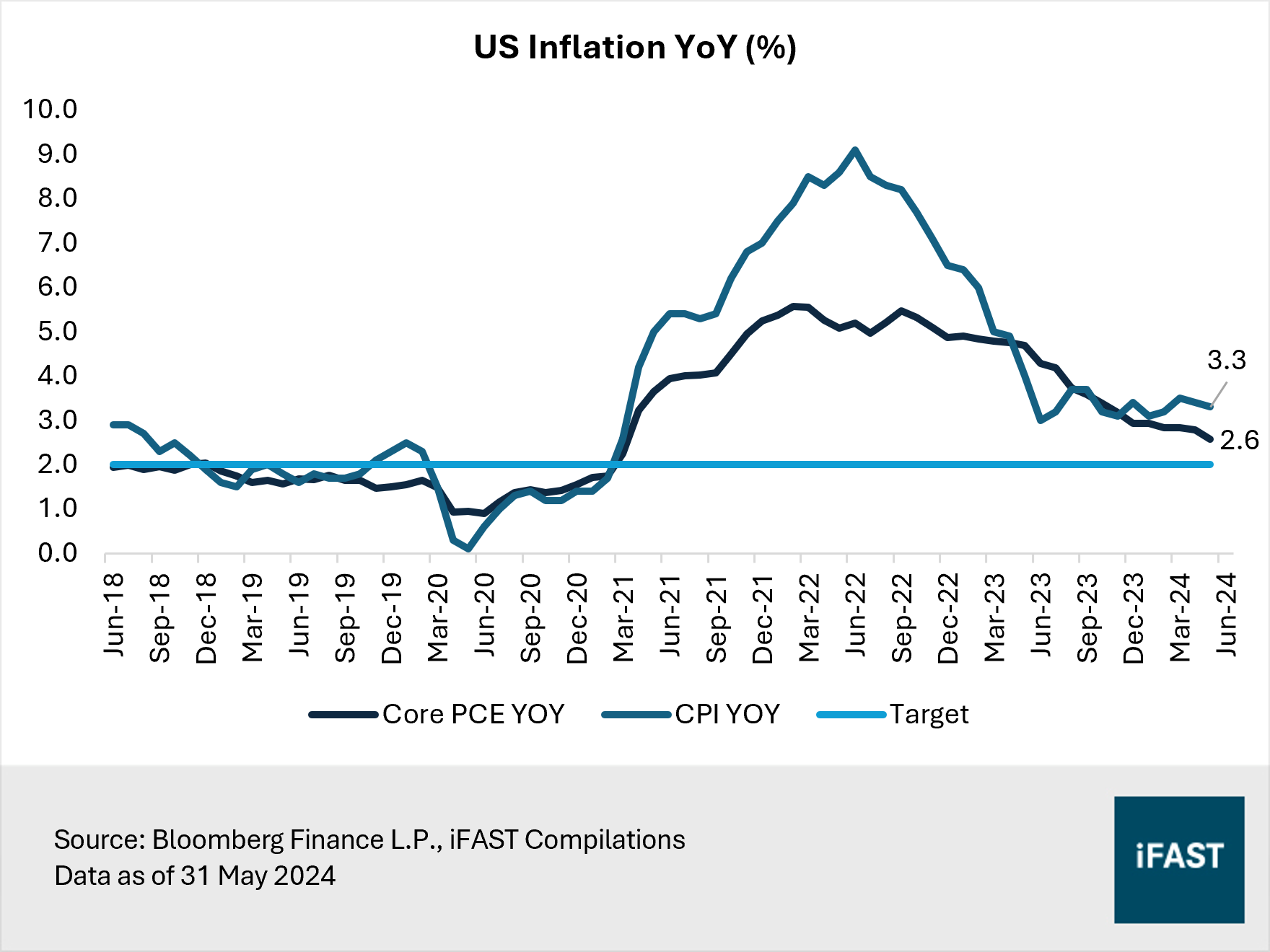

Disinflation in the US has proven to be a long and challenging process. Despite the slightly cooler CPI and core PCE in May, the broader trend remains a concern as inflation prints are still significantly above the Fed’s 2% target (Figure 1). The main culprits of these persistent inflationary pressures are high shelter costs and the tight labour market.

Figure 1: US core PCE, currently at 2.6%, remains well above target

The shelter component accounts for approximately one-third of the CPI basket. With low housing inventory, the US housing market is expected to remain firm, thus keeping inflation elevated. It is also important to note that CPI shelter tends to lag industry data by around one year or so. Meanwhile, the US labour market has shown resilience. Annual wage growth has picked up speed again, and the number of payroll jobs added in May significantly exceeded expectations.

A strong US economy, underscored by the resilient housing and labour market, does not support the case for the Fed to ease monetary policy any time soon. We reiterate our view since the beginning of 2024: there will be no Fed rate cuts this year.

We also observed a shift in the expectations for interest rate cuts. At the start of the year, the market was expecting around six rate cuts, as indicated by CME FedWatch. This expectation has since moderated to just two rate cuts. Also, the Fed has reduced its rate cut forecasts at the June policy meeting. The Fed’s dot plot now suggests only one cut in 2024, down from the previous projection of three cuts in March.

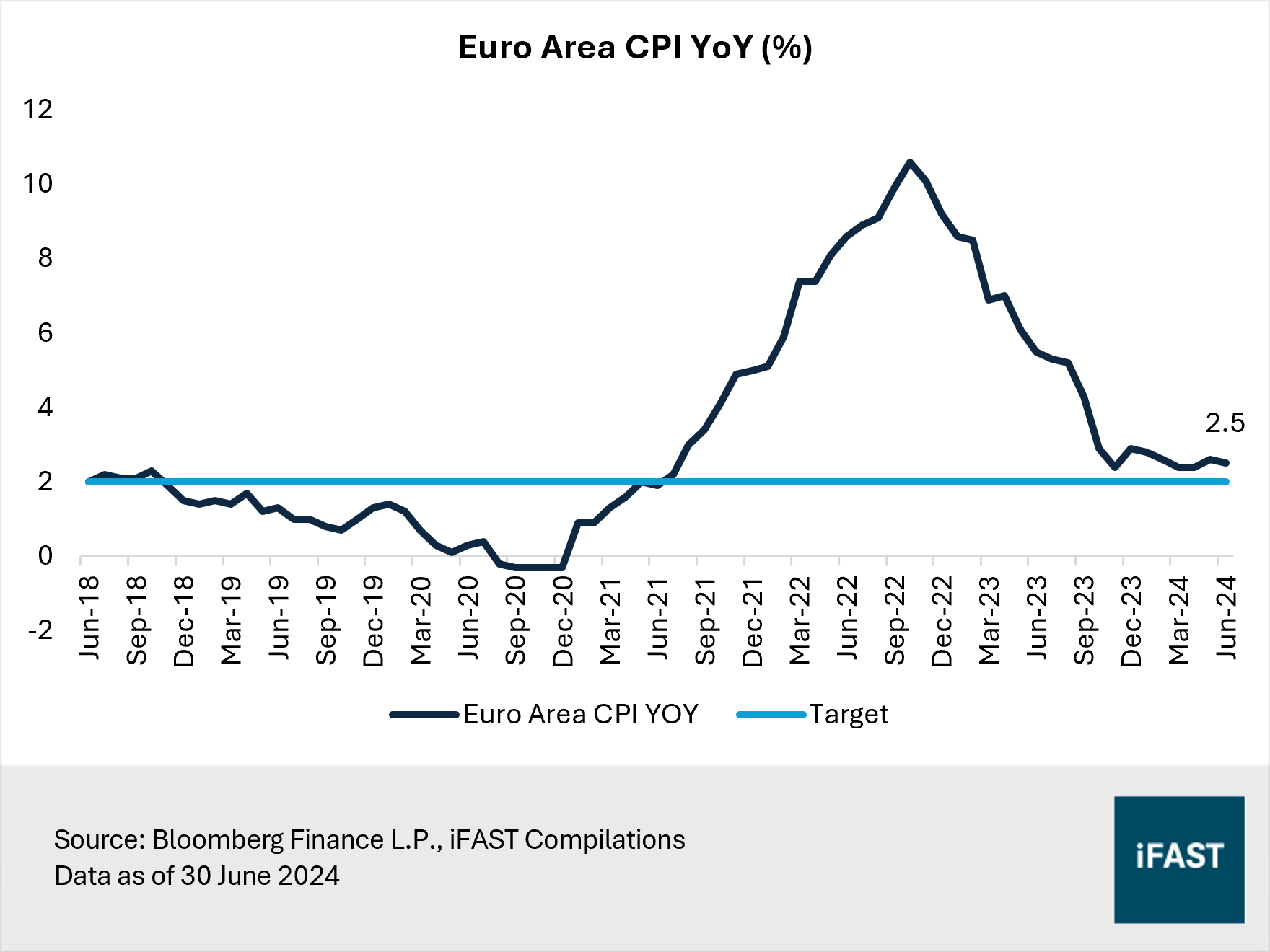

On the other hand, the European Central Bank (ECB) delivered its first interest rate cut since 2019 on 6 June 2024. This decision was driven by the substantial reduction in prices. We note that inflation rate in the euro area stood at 2.6% in May 2024, far lower than the 6.1% recorded one year earlier. June’s inflation cooled slightly to 2.5% (Figure 2). Additionally, the economy had a mild recession in the second half of 2023, showing the impact of elevated rates.

Figure 2: Inflation in the euro area currently stands at 2.6%

That said, ECB President Christine Lagarde emphasised that the central bank will remain data dependent, and stopped short of acknowledging that June’s cut marks the beginning of an ongoing reduction in interest rates. Moreover, the ECB raised its inflation projections for 2024 and 2025, forecasting that they will stay above the 2% target, citing strong domestic price pressures as wage growth is elevated.

As such, we think the rate-cutting process in the EU is likely to be very gradual. This creates a risk of correction in European equities, represented by the STOXX 600 Index, which have hit fresh record highs due to investor enthusiasm over potential rate cuts. Currently, the market expects two more cuts from the ECB this year.

To position for an environment of higher for longer inflation and interest rates, we recommend investors to focus on high-quality companies with strong balance sheets and resilient earnings. For fixed income investments, we prefer short duration bonds due to their lower sensitivity to interest rate fluctuations.

Table 1: Recommended products for a higher-for-longer environment

|

Market |

Product |

|

US Quality |

|

|

Short Duration Bond |

Japan: An opportunity not to be missed

With a divergent monetary policy stance compared to the rest of the world, the Bank of Japan (BOJ) held rates in June but struck a relatively hawkish tone. The central bank reaffirmed its expectation that the long-term inflation is likely to gradually accelerate towards its 2% target, as rising wages and prices heighten inflation expectations.

The BOJ is expected to reduce bond purchases sizably as early as July – its first step towards quantitative tightening. Additionally, Governor Kazuo Ueda indicated the central bank could potentially raise interest rates in July, depending on economic data available at the time.

Before the next policy meeting on 30-31 July, Japan will release key economic data, including the consumer confidence index, the BOJ Tankan index of large manufacturers' sentiment, and June's inflation rate.

The core-core inflation index, which excludes fresh food and energy prices and is a key measure for the BOJ, has been at or above the 2% target for around two years. Tokyo’s CPI excluding food and energy, a leading indicator of inflation nationwide, saw an uptick in the month of June. An acceleration in the nation’s core-core gauge could justify further rate increases in the coming months.

Meanwhile, rising wages is expected to positively impact consumer confidence which can signal increased consumer spending. Also, the BOJ’s closely-watched Tankan survey showed that confidence among large Japanese manufacturers have improved in the March-June quarter. Consequently, big firms should raise capital expenditure substantially, boosting the economy.

With the normalisation of Japan’s economy, we remain optimistic on Japanese equities.

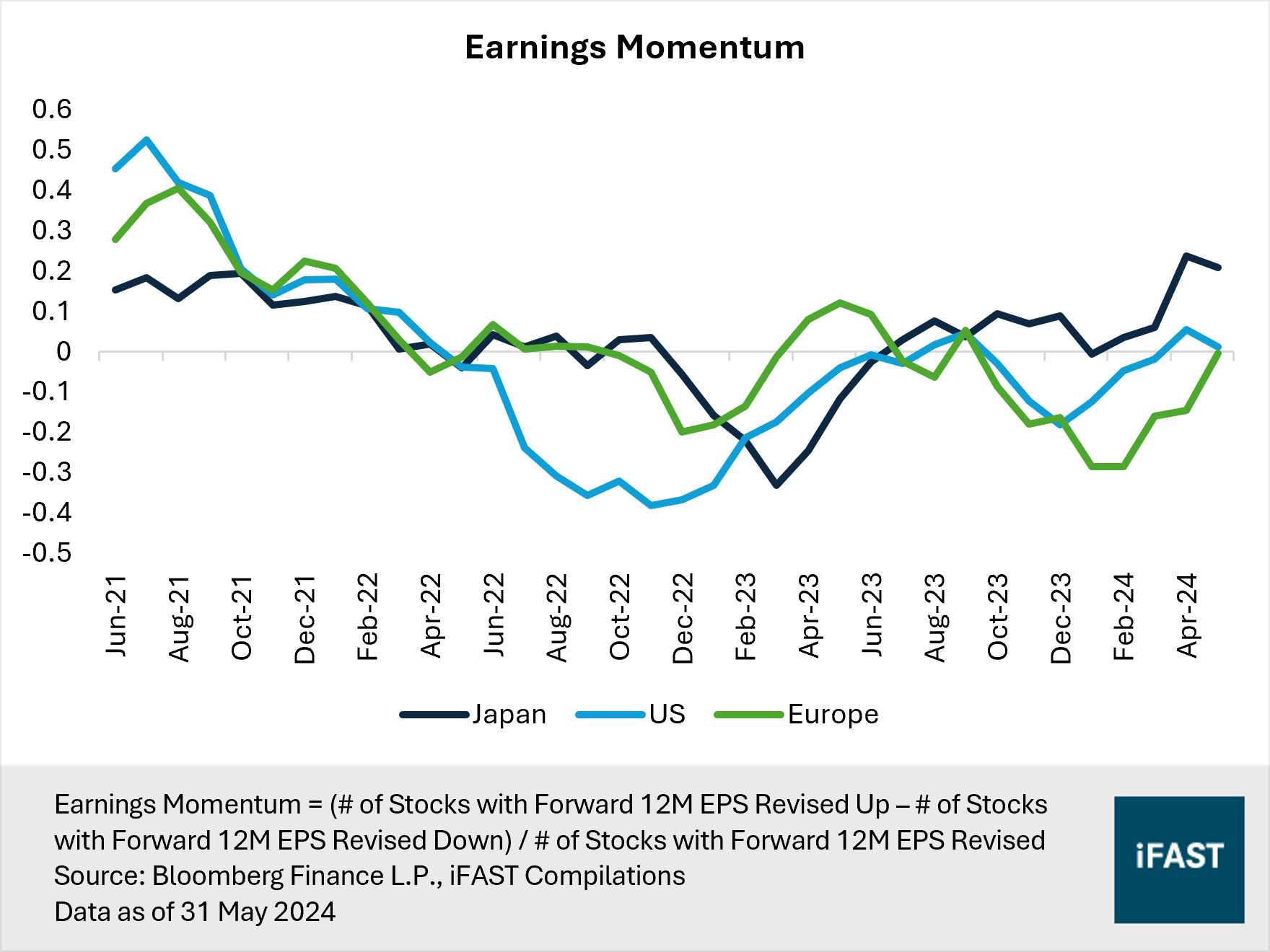

Corporate earnings are likely to strengthen against this backdrop. We found that Japan has outpaced its developed market peers like the US and Europe in terms of earnings momentum (Figure 3). A significant proportion of Japanese stocks have experienced upward EPS (earnings per share) revisions, signalling a broad-based improvement in earnings fundamentals. As these upward revisions continue, driven by an improving economy and heightened expectations of future profitability, they are poised to serve as a strong catalyst for driving up share prices.

Figure 3: Japan has seen an ongoing positive earnings revision since last year

On a sectoral level, semiconductor companies are anticipated to produce robust earnings growth underpinned by the AI revolution. Tokyo Electron, one of the largest constituents of the Nikkei 225, has projected double-digit percentage growth in the production of wafer fab equipment (WFE) this fiscal year, helped especially by AI-linked demand. Furthermore, on a national level, Japan is aiming to restore its semiconductor industry to its former glory, an effort that has the potential to propel the economy's long-term growth and enhance its self-sufficiency.

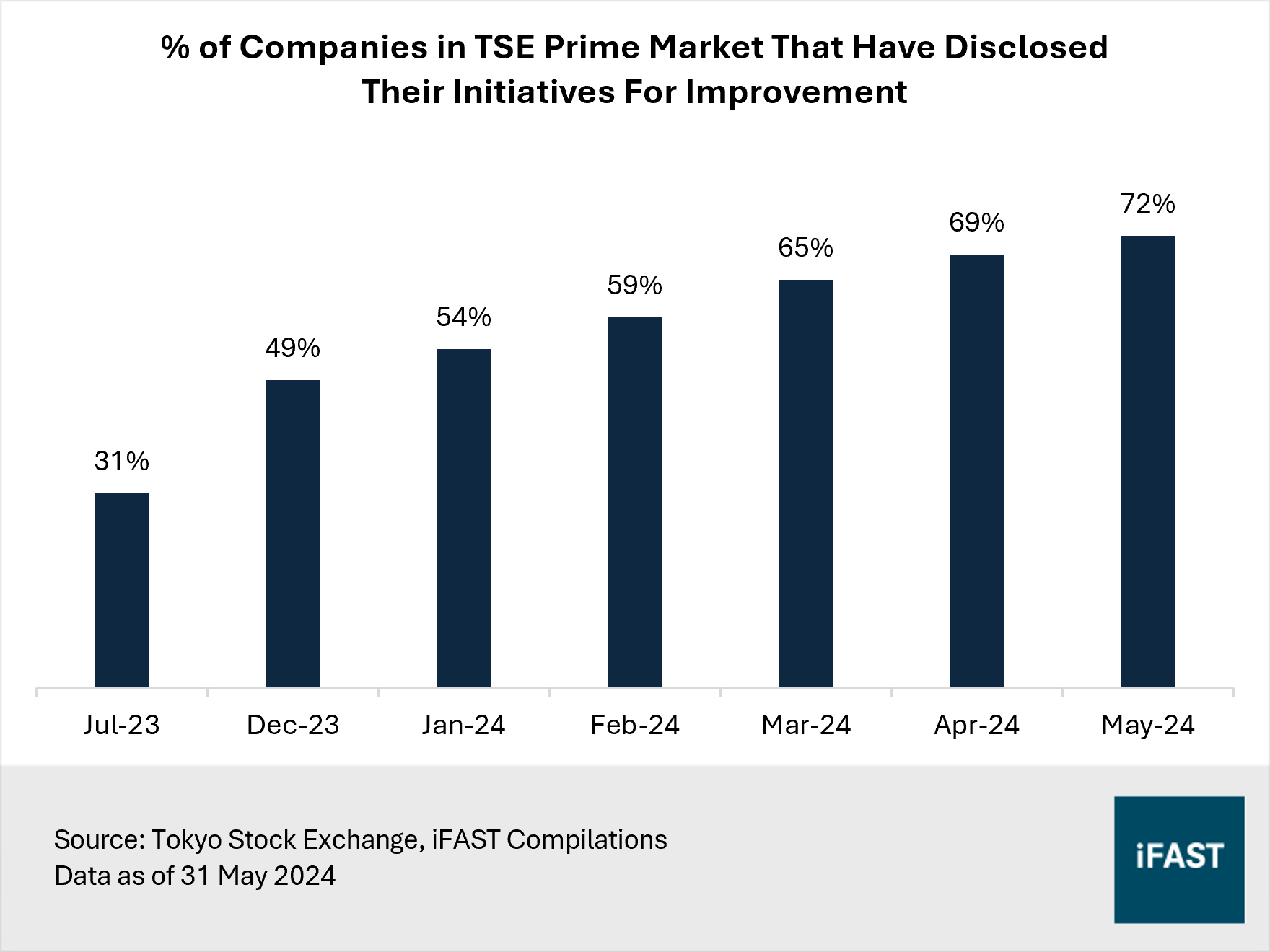

Lastly, corporate governance reforms are set to unlock greater returns for shareholders. Following pressure from the Tokyo Stock Exchange (TSE) last year, a substantial 72% of companies listed on the Prime section (the market division with the highest listing standards) have disclosed long-term plans to improve capital efficiency (Figure 4). This represents a large jump from the 31% recorded in July last year.

Figure 4: Corporate reforms are making progress

A case in point would be Dai-chi Life Holdings, which plans to reallocate capital from mature segments, mainly its domestic life insurance business, to areas with high growth potential, such as asset management. More broadly, Japanese companies are also increasing dividends and share buybacks, both of which have reached record levels. Additionally, the reduction of cross shareholdings is underway, with corporates urged to use the proceeds to enhance shareholder returns.

Given these factors, we believe Japan’s equity market has a long runway of growth. For those who missed the initial rally, the recent pullback in the Nikkei 225 after reaching the 40,000 level is a prime opportunity to capitalise on what could be a multi-year uptrend.

(Related article: This market’s stock rally is likely far from over)

Table 2: Recommended products for Japan

Market | Product |

Japan | |

Japan (Small Cap) | |

Japan (Dividend Paying) |

China: Risks intensify amidst trade tensions

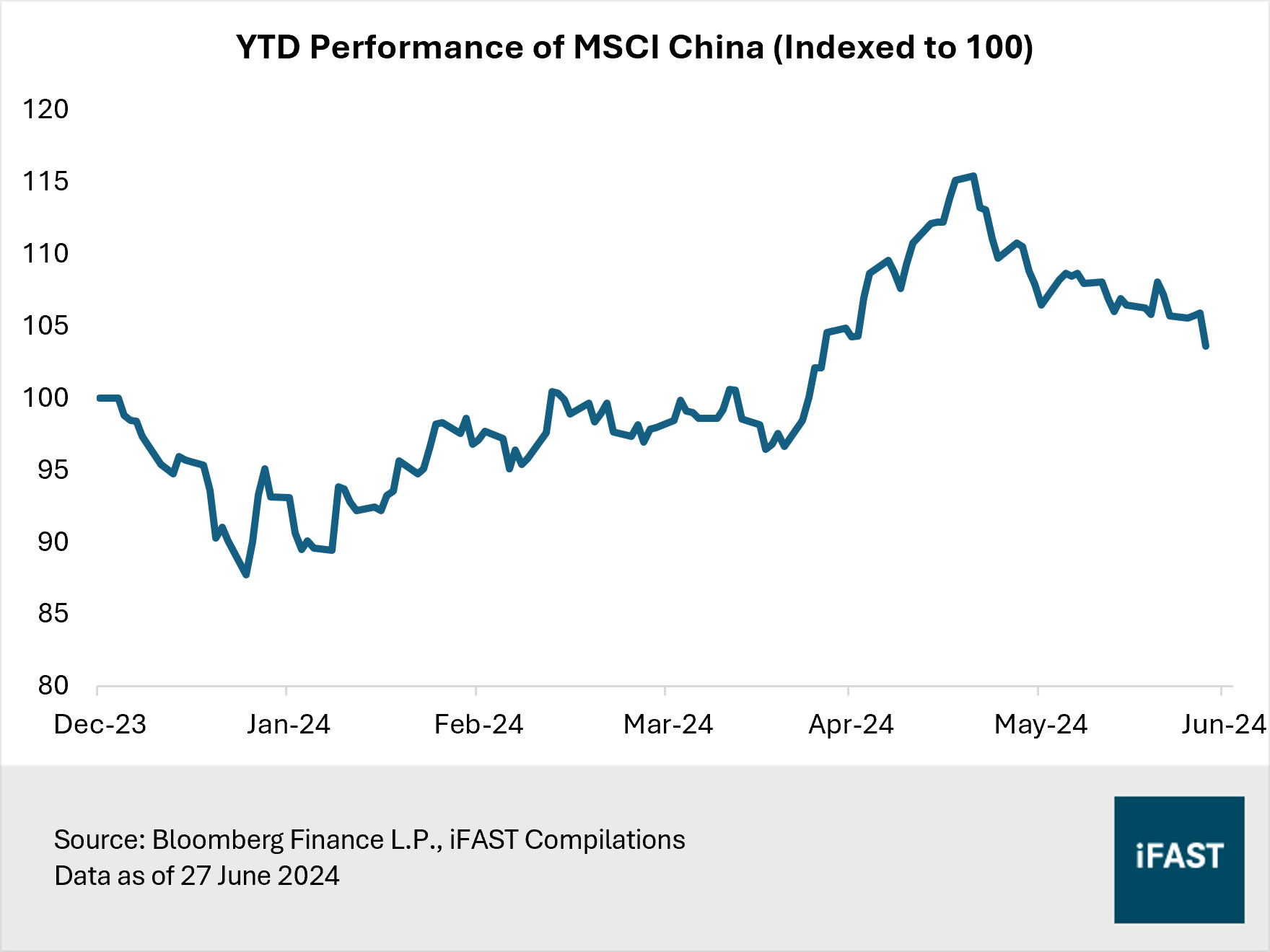

We've cautioned that China's rally isn't built to last. Sure enough, Chinese equities seem to be faltering against intensifying trade tensions and a worsening slump in the property market that remains a heavy drag on the economy. The MSCI China Index is down approximately 9% from this year’s peak (Figure 5).

(Related article: Interpreting China's 5.3% GDP Growth in 1Q24: A Positive Sign?)

Figure 5: China’s rally seems to be faltering

The latest data from the National Bureau of Statistics reveals a concerning trend: new home prices in China dropped by 0.7% in May, marking the steepest decline since October 2014. This suggests that China's measures to rescue the property market are not yet effective.

Meanwhile, tensions between China and the West have escalated significantly. On 14 May, the US announced tariffs for imports from China, including a fourfold increase in tariffs on electric vehicles (EVs) to 100%. Around a month later, the European Commission followed suit with preliminary tariffs of up to 38% on Chinese-made EVs, set to take effect from 4 July 4. Permanent tariffs, subject to a vote in November, are also on the table. More recently, Canada has considered joining in by imposing tariffs on Chinese EVs, aligning itself with allies. These developments come amidst claims that China is intentionally creating oversupply in the global EV market.

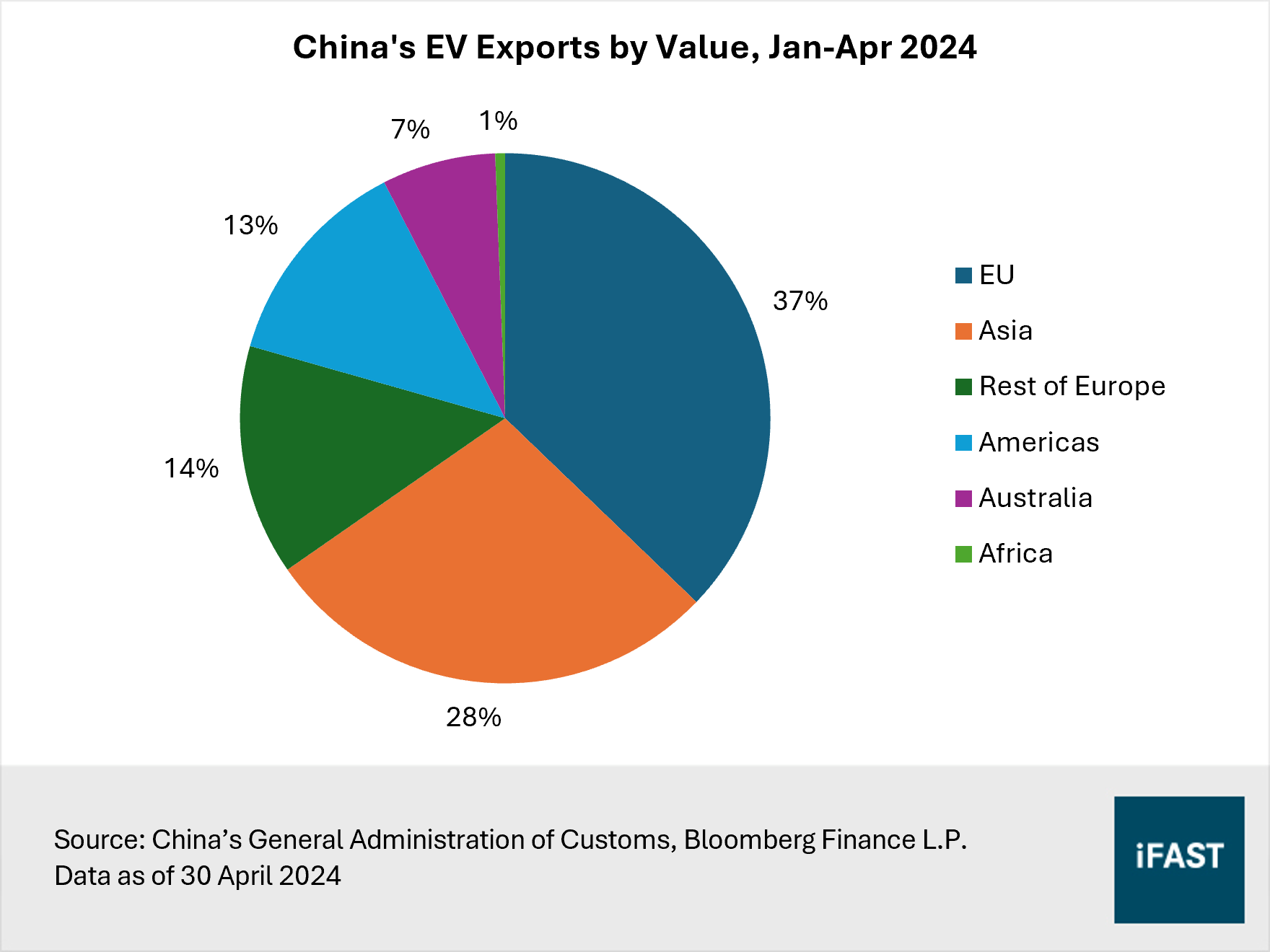

The EU stands as a major hub for Chinese EVs, absorbing nearly 40% of China's EV exports by value in the first four months of this year (Figure 6). High tariffs could directly reduce China’s EV exports and its competitiveness in the global EV market. Moreover, China's EV sector holds immense potential as a driver of economic growth amid the global shift towards a low-carbon economy. Any setbacks in EV production could ripple through the economy, potentially slowing overall growth which has already been weighed down by the ongoing challenges in China's property market.

Figure 6: The EU is a major market for Chinese EVs

Given the threat to China’s technological competitiveness and economic growth, Beijing has responded swiftly by planning retaliatory tariffs in sectors where the EU is vulnerable, particularly agriculture and automotive. This move could adversely affect German automakers such as BMW and Mercedes, which heavily rely on China for sales. China and the EU have agreed to engage in talks to resolve the escalating dispute over tariffs. However, it is unlikely that the latter will drop the tariffs entirely as Beijing would need to persuade a majority of EU members to overrule the European Commission.

In light of the economic uncertainties facing China, we recommend investors to maintain an underweight position in China within their portfolios. We also note that a trade war between China and the West can disrupt supply chains, which could further complicate global efforts to combat inflation. For exposure in Asia, investors can consider our high-conviction markets, such as the ‘New Asian Tigers’ – Japan, South Korea, and Singapore.

(Related article: Quick Take: Why is Europe also blocking the cheap Chinese EVs?)

Table 3: Recommended products for South Korea and Singapore

|

Market |

Product |

|

South Korea |

|

|

Singapore |

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.