- China is encountering an increasingly hostile environment, with the US imposing significantly higher tariffs targeting key Chinese growth industries, including a fourfold increase in tariffs on electric vehicles (EVs). Despite this, we believe the trade restrictions will have limited impacts on China's exports due to its minimal reliance on the US for EV exports.

- China's new property policy, particularly the government purchase program, aims to enhance liquidity for real estate developers. However, the addition of underperforming assets may further strain already indebted local governments and pose vacancy issues when these properties are repurposed for affordable housing in the future.

- South Korea's economy has demonstrated robust expansion this year, driven by strong demand for chips. The government is launching new support packages to fuel growth in the non-memory segment, including chip design and foundry. We anticipate that this program will further drive South Korea's technology innovation and bolster its economic growth.

- Quality stocks have outperformed growth and value stocks as of 31 May 2024. We recommend investors maintain their equity positions focused on quality, as these companies are poised to maintain financial strength amidst persistent high inflation and lead innovation in the technology frontier driven by AI.

Geopolitical Tensions: From 'De-risking' to 'Re-risking’

US Escalates Tariffs on Chinese Products

In early April, Chinese President Xi Jinping and US President Joe Biden held their first telephone conversation in nearly two years, signalling a potential thaw in relations between the two countries. However, just a month later, on 14 May, Biden instructed the Office of the U.S. Trade Representative (USTR) to increase tariffs on approximately USD 18 billion worth of Chinese imports. The new tariffs target China's key growth industries, including electric vehicles (EVs), semiconductors, new energy equipment, and medical products (Table 1).

The most substantial tariff increase was imposed on EVs, with the rate quadrupling from 25% to 100%. Additionally, batteries and key materials used in battery production will face a new tariff rate of 25%.

Table 1: US’s new tariff rates on Chinese products

|

Product Category |

Old Rate |

New Rate |

Effective Year |

|

Electric vehicles |

25% |

100% |

2024 |

|

Batteries, Battery Components and Parts, and Critical Minerals |

|||

|

Battery parts (non-lithium-ion batteries) |

7.50% |

25% |

2024 |

|

Lithium-ion electrical vehicle batteries |

7.50% |

25% |

2024 |

|

Natural graphite |

0% |

25% |

2026 |

|

Permanent magnets |

0% |

25% |

2026 |

|

Other critical minerals |

0% |

25% |

2024 |

|

Medical Products |

|||

|

Facemasks |

0-7.5% |

25% |

2024 |

|

Syringes and needles |

0% |

50% |

2024 |

|

Medical gloves |

7.50% |

25% |

2026 |

|

Semiconductors |

25% |

50% |

2025 |

|

Ship to shore cranes |

0% |

25% |

2024 |

|

Solar cells (whether or not assembled into modules) |

25% |

50% |

2024 |

|

Steel and aluminum products (including steel- and aluminum-intensive products) |

0-7.5% |

25% |

2024 |

|

Source: Section 301, Covington & Burling LLP. iFAST

Compilations. |

|||

Although the tariff increase appears significant, we believe its impact on China's trade, particularly on EV exports, will be limited. According to Chinese customs data, in 2023, China exported approximately 12,400 EVs to the US, representing less than 1% of China's total EV export volume and value. As China's EV industry is not reliant on the American market, the additional tariffs imposed by the U.S. are unlikely to have a significant economic impact on Chinese enterprises or constrain China’s economic growth through trade restrictions.

While the US tariffs on Chinese products may have a limited impact, their effects could be far-reaching if Europe follows suit. In 2023, 38.7% of China's total EV exports by volume went to the Eurozone, and another 9.45% went to the UK. The European Commission’s ongoing anti-subsidy investigation has led Italian Industry Minister Adolfo Urso to urge the EU to impose tariffs on EVs, similar to the US. However, opponents, including German Chancellor Olaf Scholz, have cautioned against such measures, warning that China could retaliate with anti-dumping investigations into key EU exports, such as polyoxymethylene copolymer - a chemical widely used in automotive engineering and large-engine vehicles. These trade restrictions could ultimately harm the trade relationships and economic interests of both regions.

We view the current US trade policy as having broader political implications rather than being solely economically driven. Biden's decision to increase tariffs follows Trump's claim of a 60% tariff on Chinese imports should he be re-elected. Regardless of the outcome of the upcoming election, whether Biden or Trump assumes office, we anticipate more aggressive policies throughout the year as both candidates seek to bolster their political support by applying increased pressure on China.

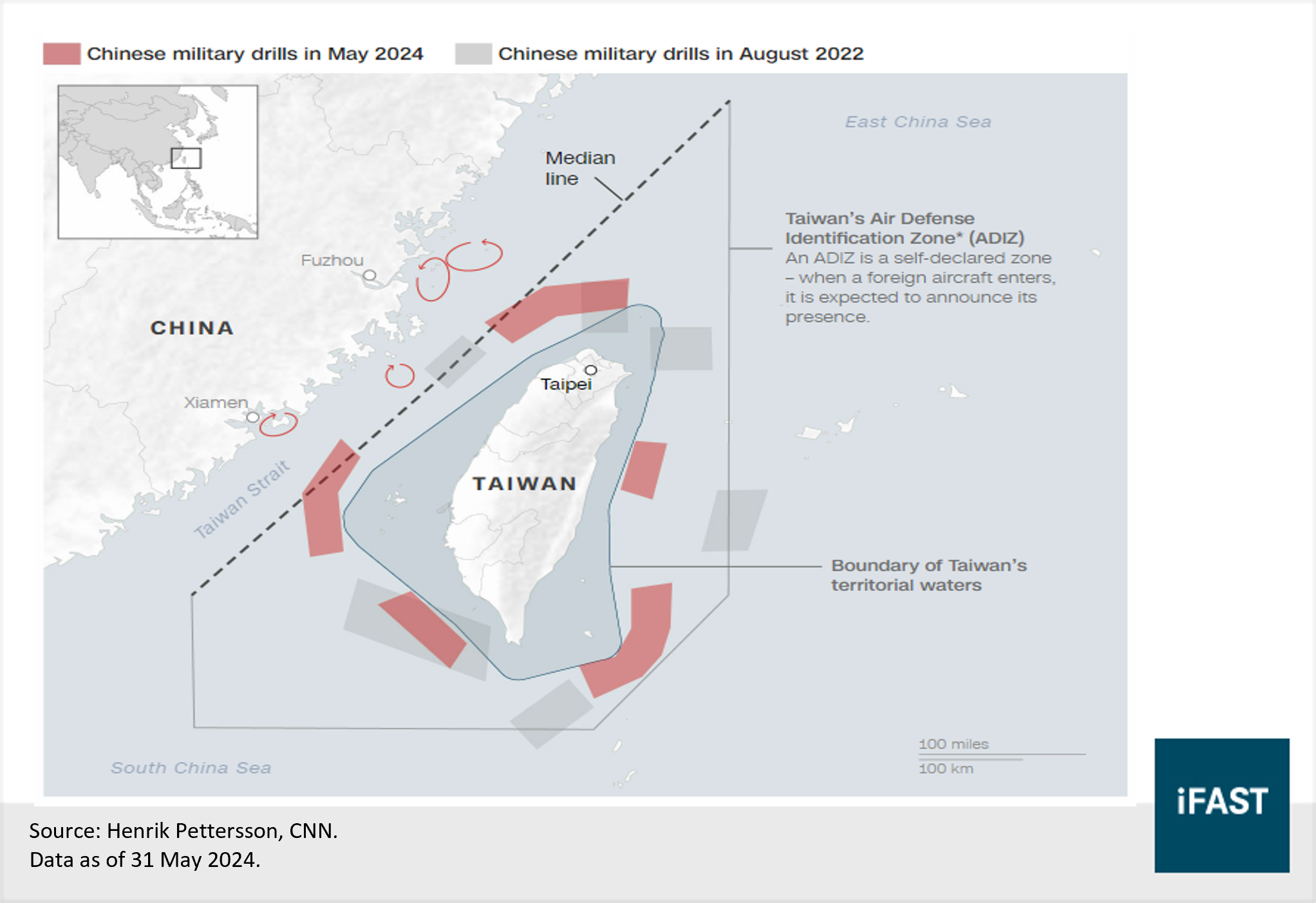

Rising Tensions Between China and Taiwan

Beyond the US-China rivalry, tensions between China and Taiwan have also escalated, with Taiwan's new president, Lai Ching-te, adopting a more assertive stance than his predecessors. In his inauguration speech on 20 May 2024, Lai declared that Taiwan is not subordinate to China and urged Beijing to cease military and political threats. In retaliation for Lai's "separatist acts," the People’s Liberation Army (PLA) conducted two days of military drills around Taiwan on 23 and 24 May 2024. These exercises aimed to practice cutting off the island’s energy imports, escape routes for "Taiwan independence" forces, and support lines from the US and its allies.

We believe the likelihood of a war across the Taiwan Strait remains low at present, particularly as China grapples with domestic economic challenges. However, China’s stance on Taiwan is expected to become increasingly rigid. Under Lai's leadership, Taiwan is likely to strengthen its ties with Western nations and further distance itself from China.

Figure 1: China's May military drills encircled Taiwan

China’s New Property Policy: Government Purchase Program

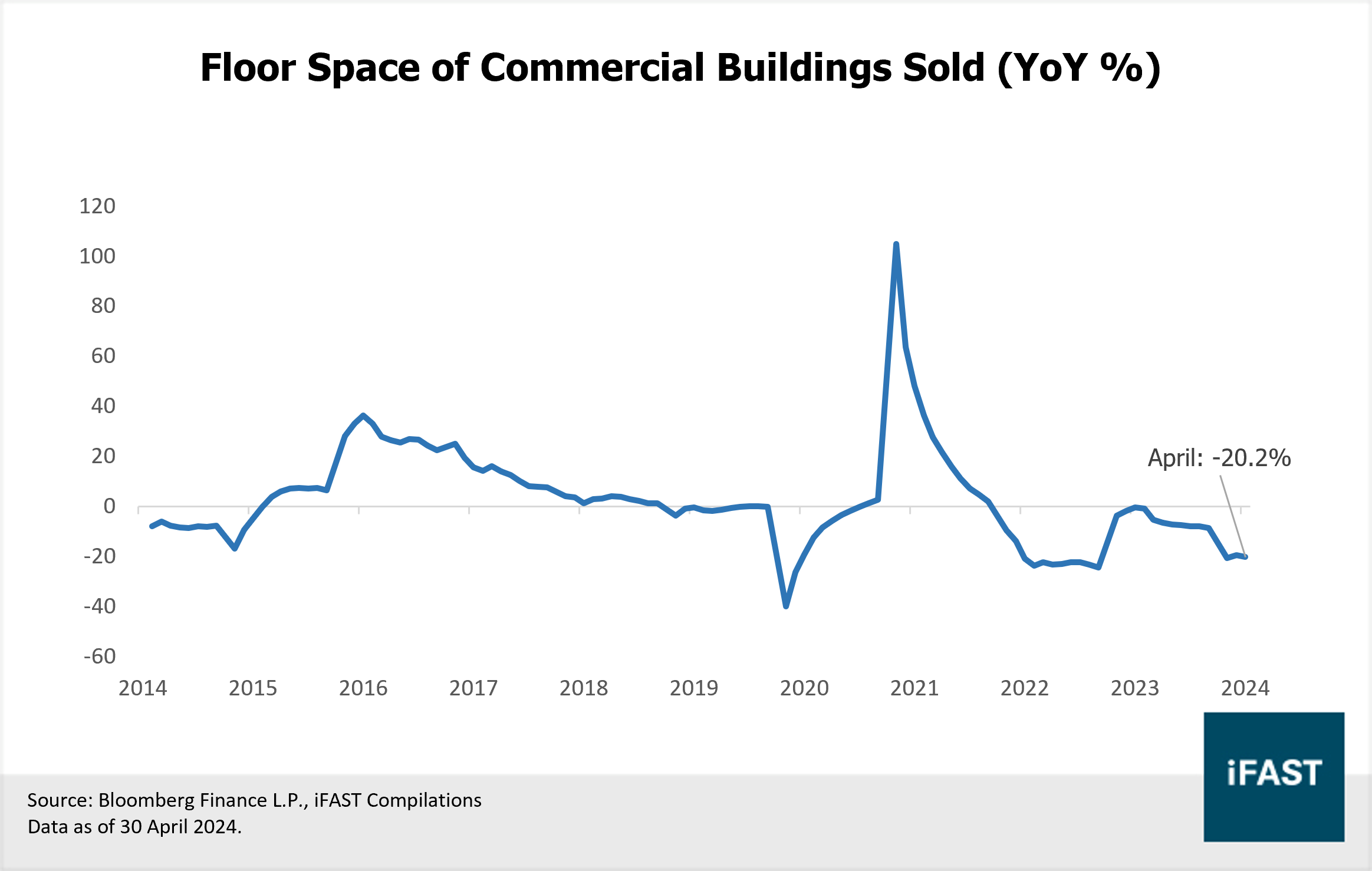

In addition to escalating external risks, China's internal property market continues to struggle, showing no signs of recovery after years of decline. As of 30 April 2024, the floor space of commercial property sold in China had decreased by 20.2% year-over-year, marking one of the steepest declines over the past year (Figure 2).

Figure 2: Floor space of commercial buildings sold decreased by 20.2% in April 2024

After two years of economic challenges, on 17 May 2024, China introduced a new policy package aimed at stimulating demand while reducing housing supply:

(1) Downpayment requirements were further reduced to historical lows, with first-time buyers now required to put down 15% (down from 20%) and second-time buyers 25% (down from 30%).

(2) Interest rates on loans tied to individual housing provident funds were lowered by 0.25%.

(3) The People's Bank of China (PBOC) established a 300 billion yuan relending facility at a 1.75% interest rate for state-owned companies to purchase excess housing inventory at affordable prices. These houses will be repurposed for affordable housing.

While the first two policies are relatively standard, the Chinese markets have rallied in response to the government purchase program. The CSI 300 Real Estate Index closed 9.1% higher on 17 May 2024.

Although buying inventory will improve cash flow for developers and stabilise their financial conditions, state-owned enterprises tasked with these purchases could face vacancy risks once the units are repurposed for affordable housing. Local governments, already burdened with significant local government financing vehicle (LGFV) debts, will be further strained if these underperforming assets are added to their balance sheets. Ultimately, the core issue remains weak demand, which has yet to show signs of a meaningful rebound.

We advise investors to maintain an underweight position in China within their portfolio and instead allocate capital to markets with more promising returns, such as the 'New Asian Tigers' - Japan, South Korea, and Singapore.

Table 2: Recommended products for “New Asian Tigers”

|

Countries |

Unit Trusts |

ETFs |

|

Singapore |

||

|

Japan |

||

|

South Korea |

Related articles:

Should you follow the rally in Asian equities?

Interpreting China's 5.3% GDP Growth in 1Q24: A Positive Sign?

South Korea: Capitalising on Chip-Driven Growth

Robust Economy Bolstered by Recovery in Chip Sales

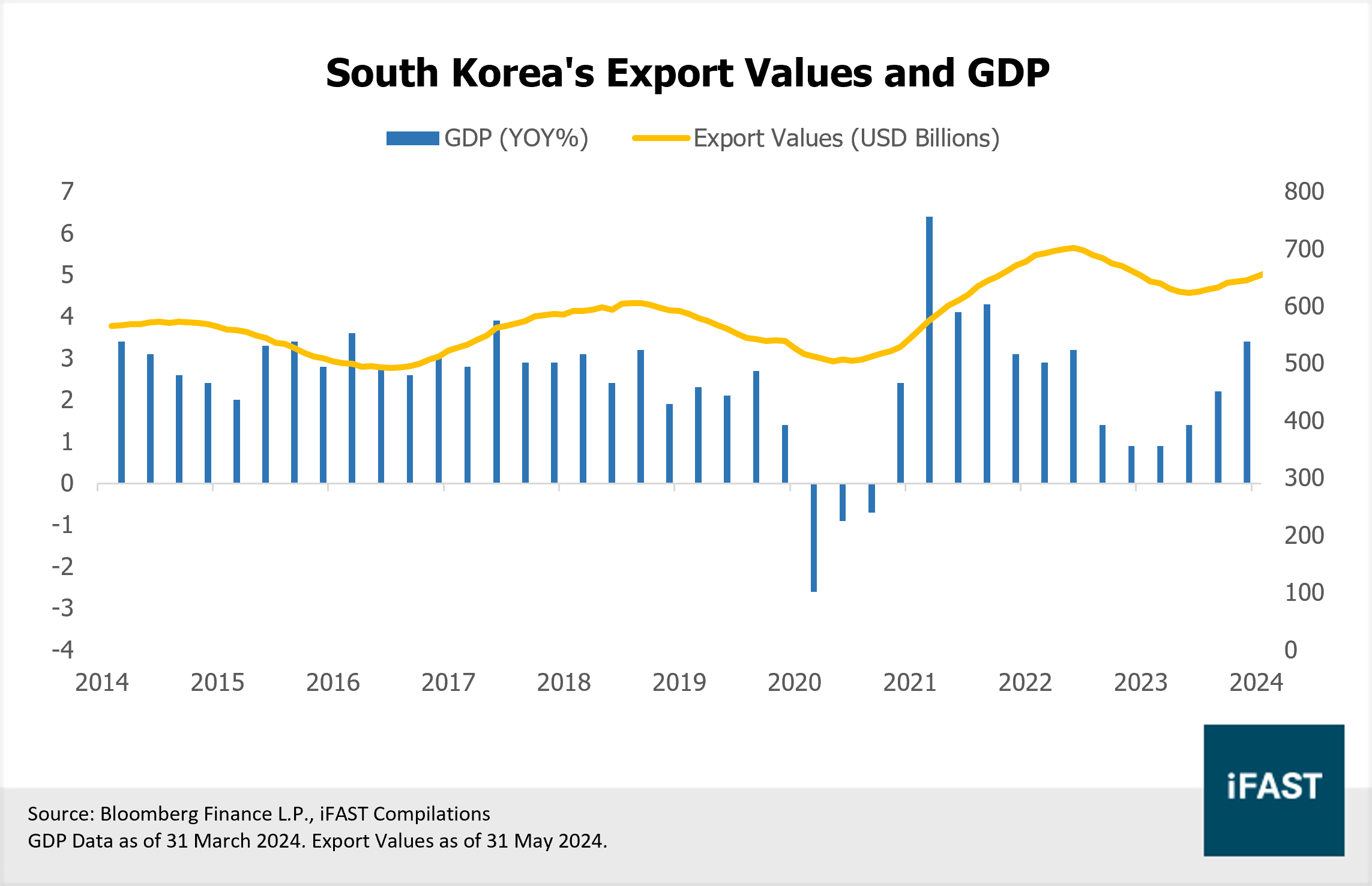

South Korea’s exports rose for the eighth consecutive month in May, driven by robust demand for semiconductors. Overseas sales of semiconductors surged 54.5% year-over-year to USD 11.4 billion. Exports of other IT products, including display panels, computers, and automobiles, also contributed to this growth. This strong export performance resulted in a trade surplus of USD 4.96 billion in May, the highest since December 2020. We anticipate that these strong export figures will significantly bolster South Korea’s economic growth this year.

Figure 3: South Korea's export growth fuels GDP expansion

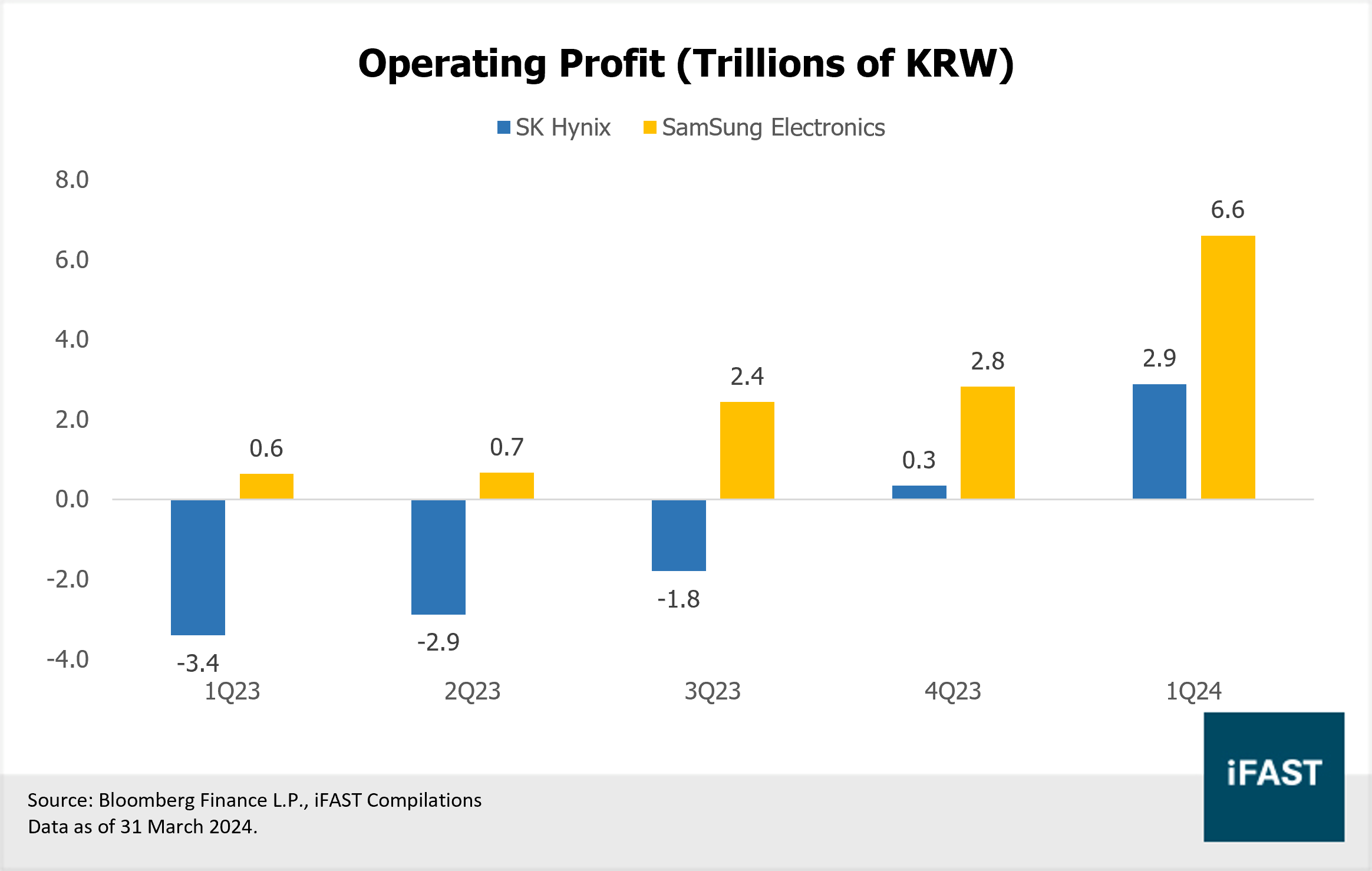

The robust demand recovery in chips, particularly the advanced High Bandwidth Memory (HBM) varieties essential for complex AI applications, has propelled the rebound in memory chip prices and sales. South Korea’s leading memory chip manufacturers, Samsung Electronics Co. and SK Hynix Inc., witnessed staggering year-over-year increases in operating profit of 993% and 734%, respectively, in the first quarter of this year (Figure 4).

Figure 4: Significant improvement in profit margins for Samsung Electronics and SK Hynix

South Korea's Expansion in the Non-Memory Sector

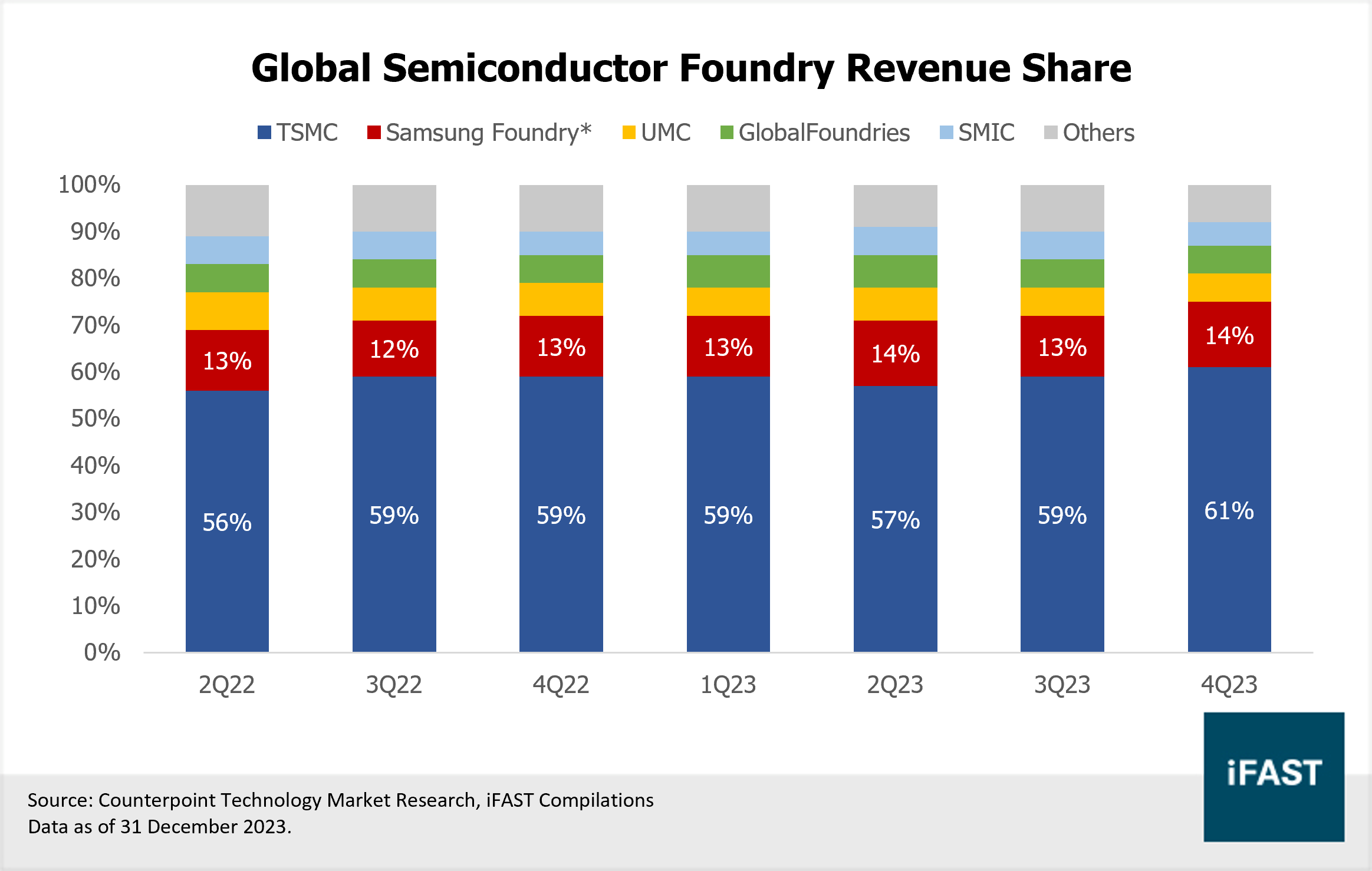

While Samsung Electronics Co. and SK Hynix Inc. dominate the global memory chip market, they lag behind some competitors in the non-memory chip industry. South Korean President Yoon Suk Yeol noted that South Korea’s chip design market share is only 1% globally, significantly trails industry leaders such as Nvidia (55.27%) and Qualcomm (30.91%). Additionally, South Korea’s foundry businesses lag behind TSMC by a considerable margin (Figure 5).

Figure 5: South Korea trails behind Taiwan in foundry business

On 23 May 2024, South Korea unveiled a 26 trillion won (USD 19 billion) support package aimed at addressing weaknesses across the entire semiconductor ecosystem. Under the package, approximately 17 trillion won will be allocated to a loan program administered by the Korea Development Bank, enabling companies to finance large-scale equipment investments at preferential interest rates. Furthermore, the application period for national strategic technology tax credits will be extended, with the scope of research and development (R&D) tax credits expanded to cover expenses such as chip design software purchases.

In the midst of intense competition in the global semiconductor market, South Korea's support packages underscore its commitment to maintaining its competitive edge and closing the gap with leading chip designers and contract manufacturers. We anticipate that this program will further drive South Korea's technology innovation and bolster its economic growth.

Table 3: Recommended products for South Korea

|

Market |

UT |

ETF |

|

South Korea |

Continue To Focus On Quality Stocks

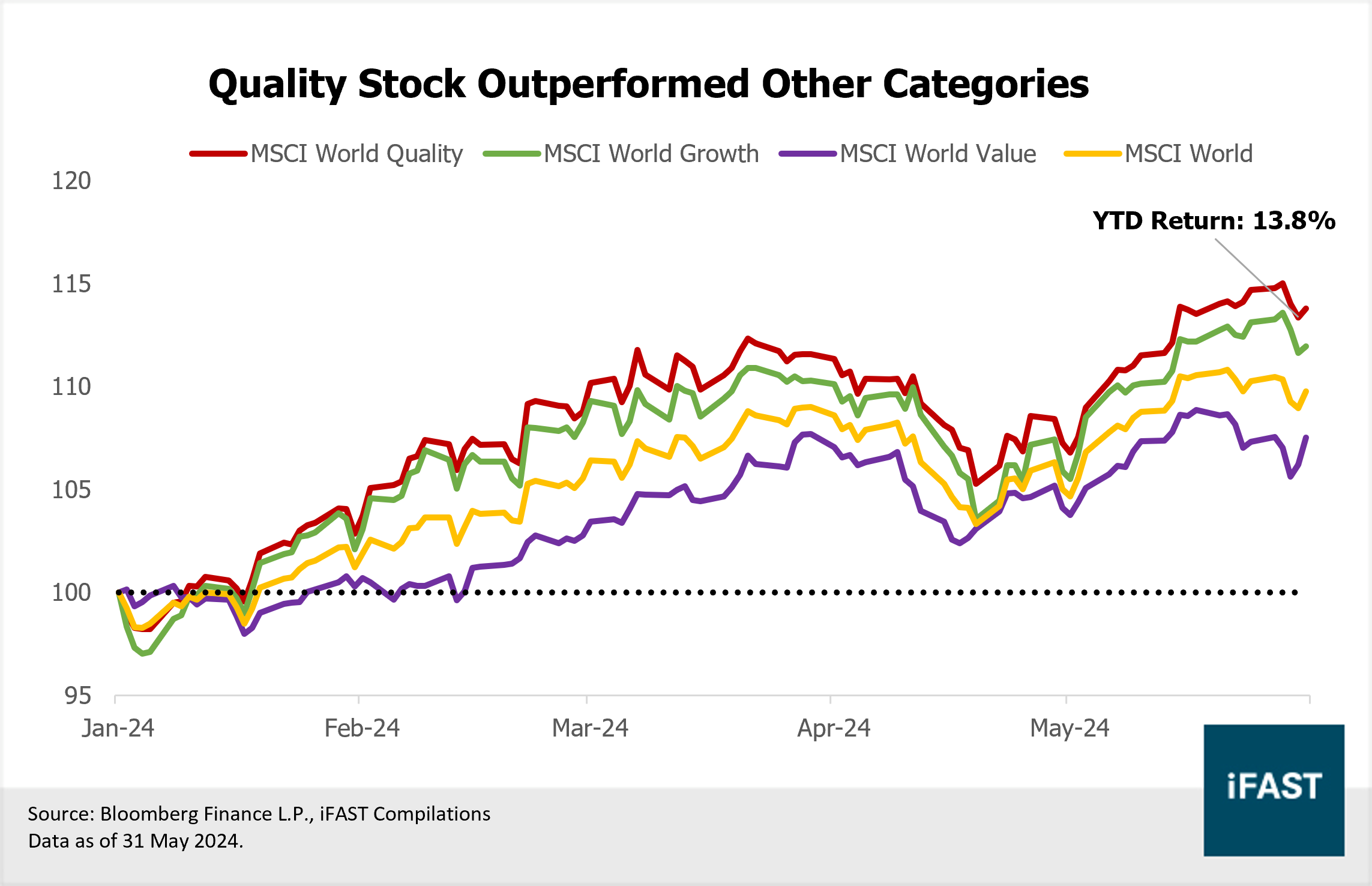

In our 2024 investment outlook, we emphasized the significance of investing in quality stocks amidst the prevailing "higher-for-longer" interest rate environment. As of 31 May 2024, the MSCI World Quality Index have outperformed both their growth and value counterparts, as well as the broader market, registering a 13.8% total return (Figure 6).

Figure 6: Quality stocks outperformed their growth and value peers

Quality companies have developed resilient business models, characterised by robust profit margins, strong balance sheets, and good pricing power. These traits have enabled them to amass substantial cash reserves without resorting to borrowing at high interest rates. Moreover, these companies consistently reinvest in research and development (R&D) to maintain their technological superiority and market leadership.

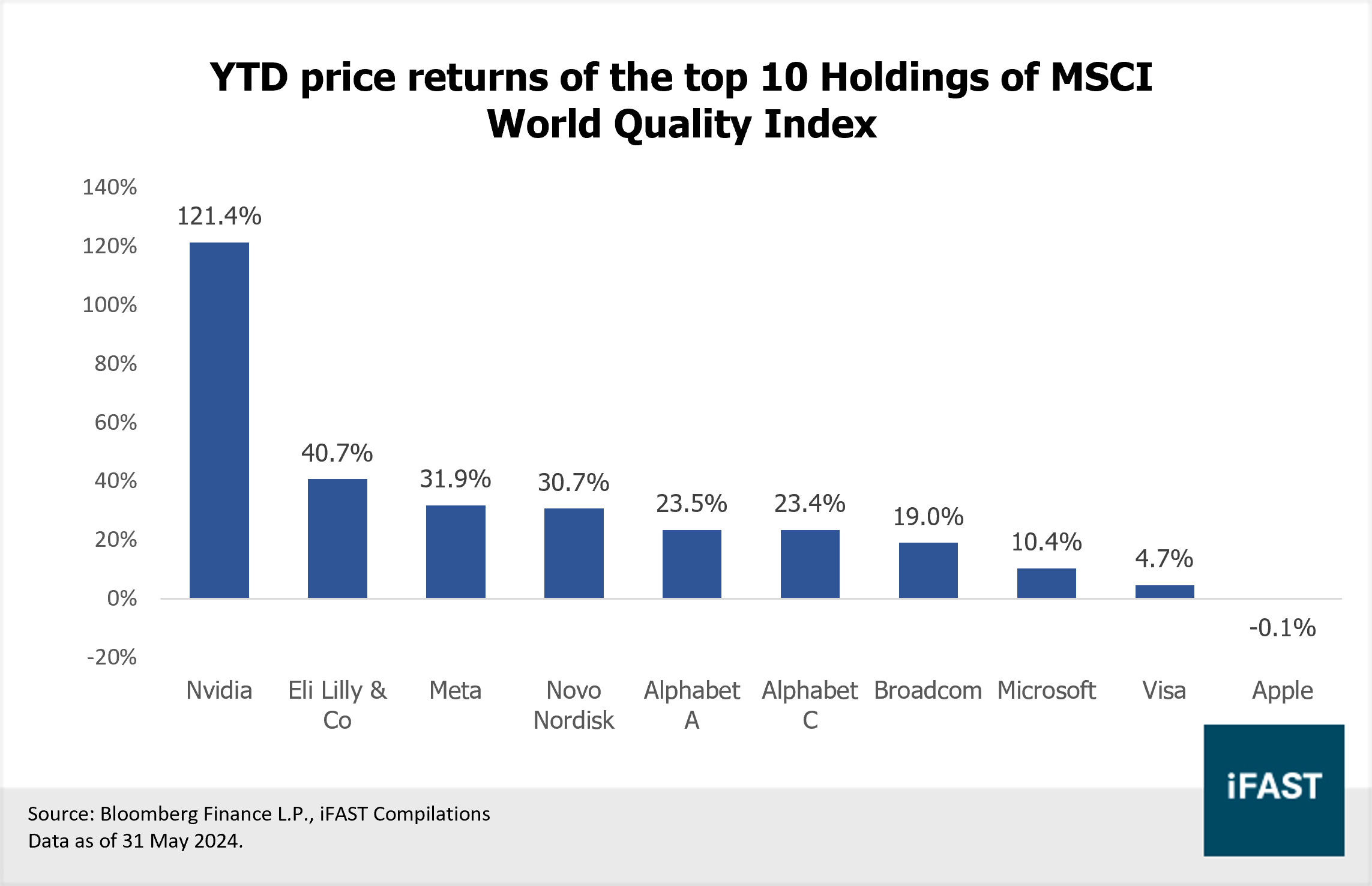

Take Nvidia, for instance, the largest constituent in the MSCI World Quality Index. It is the top performer among quality stocks, with its share price surging by 121.5% YTD as of 31 May 2024. Its first-quarter revenue, ending 28 April 2024, witnessed a remarkable 262% increase year-over-year. Notably, Nvidia allocated 77.8% of its total operating expenses to R&D, leading to the introduction of innovative products like the Blackwell platform in the first quarter.

Similarly, major tech companies that made early investments in and integrated artificial intelligence (AI) into their operations have reaped significant synergistic benefits. Meta and Alphabet, for instance, have witnessed amplified advertisement impressions and revenue growth, fueled by AI-enabled content engagement strategies. Likewise, Microsoft's AI-powered office suite Copilot, infused with OpenAI technology, has played a pivotal role in driving GitHub's revenue growth. The substantial presence of these firms in the AI market has directly contributed to their considerable share price appreciation in the first five months of the year.

Figure 7: Price returns of the top 10 holdings of the MSCI World Quality Index

In addition to AI-driven growth, quality stocks have also benefited from macroeconomic uncertainties. Rising US-China tensions and persistent geopolitical instability in the Middle East have positioned quality stocks favourably. Moreover, the resilient business models of quality stocks are well-positioned to thrive in an environment where the path to rate cuts is unclear. Therefore, we believe that quality investing represents a promising strategy for investors seeking refuge amid a period of economic uncertainty and higher inflation.

For investors interested in quality stocks, we recommend JPMorgan US Quality Factor ETF (NYSE:JQUA).

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.