- The MSCI AC Asia ex Japan Index, which measures the performance of Asian equities (excluding Japan), recorded an underwhelming year-to-date return of 0.5%.

- We continue to stay cautious on China and India which are heavyweights in the region (collectively representing 50% of the index), implying a challenging outlook for Asian equities.

- While we hold a more optimistic view on Taiwan and South Korea on the back of a rebound in the global semiconductor sector, these markets have less hold on the overall outlook for Asia ex Japan due to their combined weightage of around 30% in the index.

- Moreover, we see further scope for earnings growth to decline as China’s economic malaise continues, presenting downside risks for Asian equities.

- Based on our fair PE ratio of 13.5X, we project a target price of USD 602 for the MSCI AC Asia ex Japan Index, translating to an upside potential of 14% by 2025. We maintain our 2.5 Stars “Neutral” view for the region, with a preference for selected markets like South Korea, Singapore, Taiwan, and Malaysia.

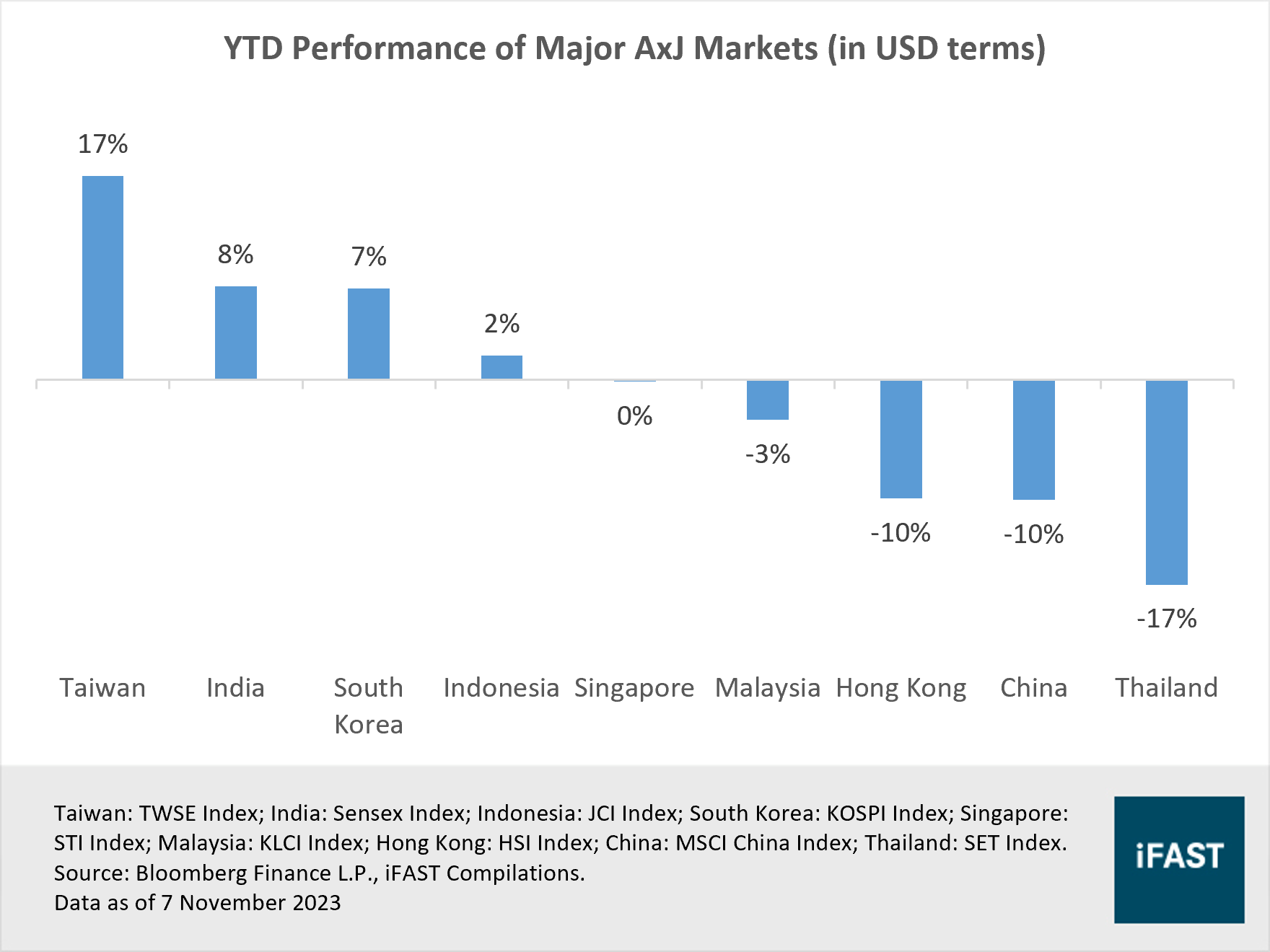

The MSCI AC Asia ex Japan Index, which measures the performance of Asian equities (excluding Japan), delivered returns of 0.5% in USD terms year-to-date (YTD) as of 7 November 2023. This performance lags behind broader global equities and emerging market (EM) benchmarks which reported returns of 11.9% and 3.1% respectively during the same period.

Asian equities, which holds a significant 35% weightage to China, have faced pressure due to lacklustre Chinese macroeconomic data which signalled that the reopening rebound has largely faded. In contrast, Taiwan has fared relatively better within the region, with leaders like TSMC benefitting from the optimism surrounding artificial intelligence (AI).

As the Chinese government prepares to implement a new round of stimulus to lift its economy, a question arises: will Asian equities see brighter prospects moving forward? We believe there are reasons to maintain our neutral stance on the region, and highlight the reasons behind it in this article.

Figure 1: China is one of the underperformers

Staying cautious on the Asian heavyweights

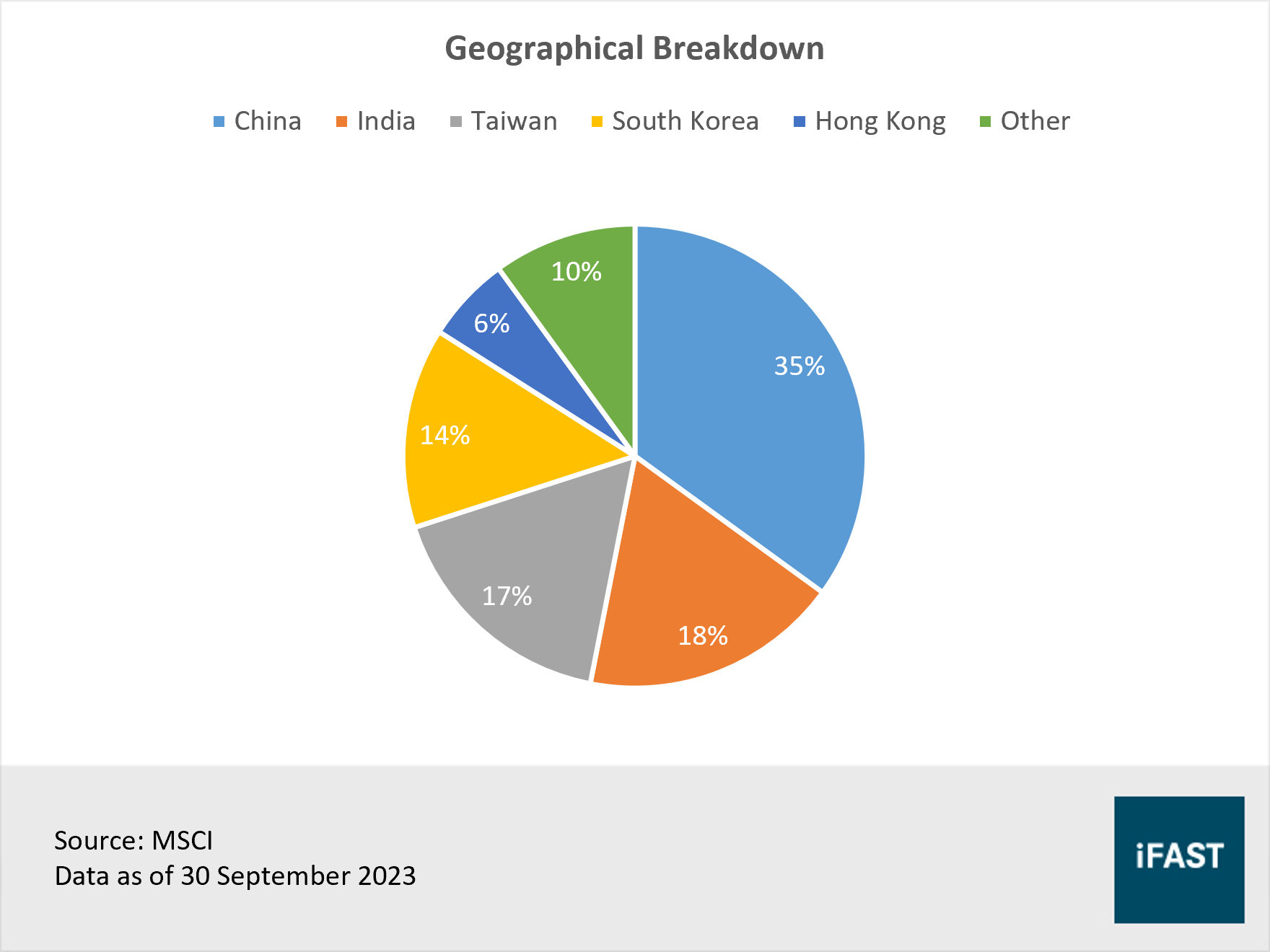

The two largest markets in Asia ex Japan are China and India, collectively representing 50% in the MSCI AC Asia ex Japan Index (Figure 2). Consequently, their outlooks would significantly influence the prospects of the region.

Figure 2: The Asian heavyweights are China and India

China:

After the slower-than-expected recovery in domestic consumption during the Golden Week holiday, traditionally a peak season for local spending, China is reportedly thinking about increasing its budget deficit for 2023 with a fresh round of stimulus. This plan entails issuing at least CNY 1 trillion in extra government debt, which will be allocated towards infrastructure projects.

We believe that such measures are unsustainable, and reinstate our view that policymakers have limited options to rejuvenate its faltering economy. China remains overly dependent on infrastructure spending to stimulate growth. Besides, the measures fail to address the root cause of the economic malaise; consumer confidence remains fragile due to a deepening property crisis, and youth unemployment has reached record levels.

The property sector continues to present challenges to the economic outlook. The default of Country Garden, which comes two years after the fall of Evergrande, undermines confidence that China can recover from its property-related issues. Meanwhile, developers who are still not yet in a default would likely find staying afloat an increasingly challenging prospect due to the continued decline in home sales (Figure 3).

Figure 3: China’s property market remains in the doldrums

We also have concerns regarding the long-term structural issues in China. We expect China to accelerate its shift to a top-down state-controlled economy, and as the balance of priorities shifts toward self-sufficiency, China may enter a low-growth period. Additionally, the long-term profitability of private companies, especially those that are not aligned with the government’s policy direction, is at risk. Meanwhile, with concerns about geopolitics, China is becoming an increasingly challenging place to do business in. As a result, more multinational companies are likely to relocate their production facilities away from China to diversify business risks.

In summary, we maintain our negative view on Chinese equities. We are also cautious on Hong Kong, which occupies around 6% of the MSCI AC Asia ex Japan Index, for reasons similar to China since Chinese companies make up majority of the Hang Seng Index.

(Related article: Is China’s stock market finally too cheap to be ignored?)

India:

While we recognise that India could be considered a viable alternative as investors shift away from China, it is important to note that there are some key factors that may hinder India’s continued growth.

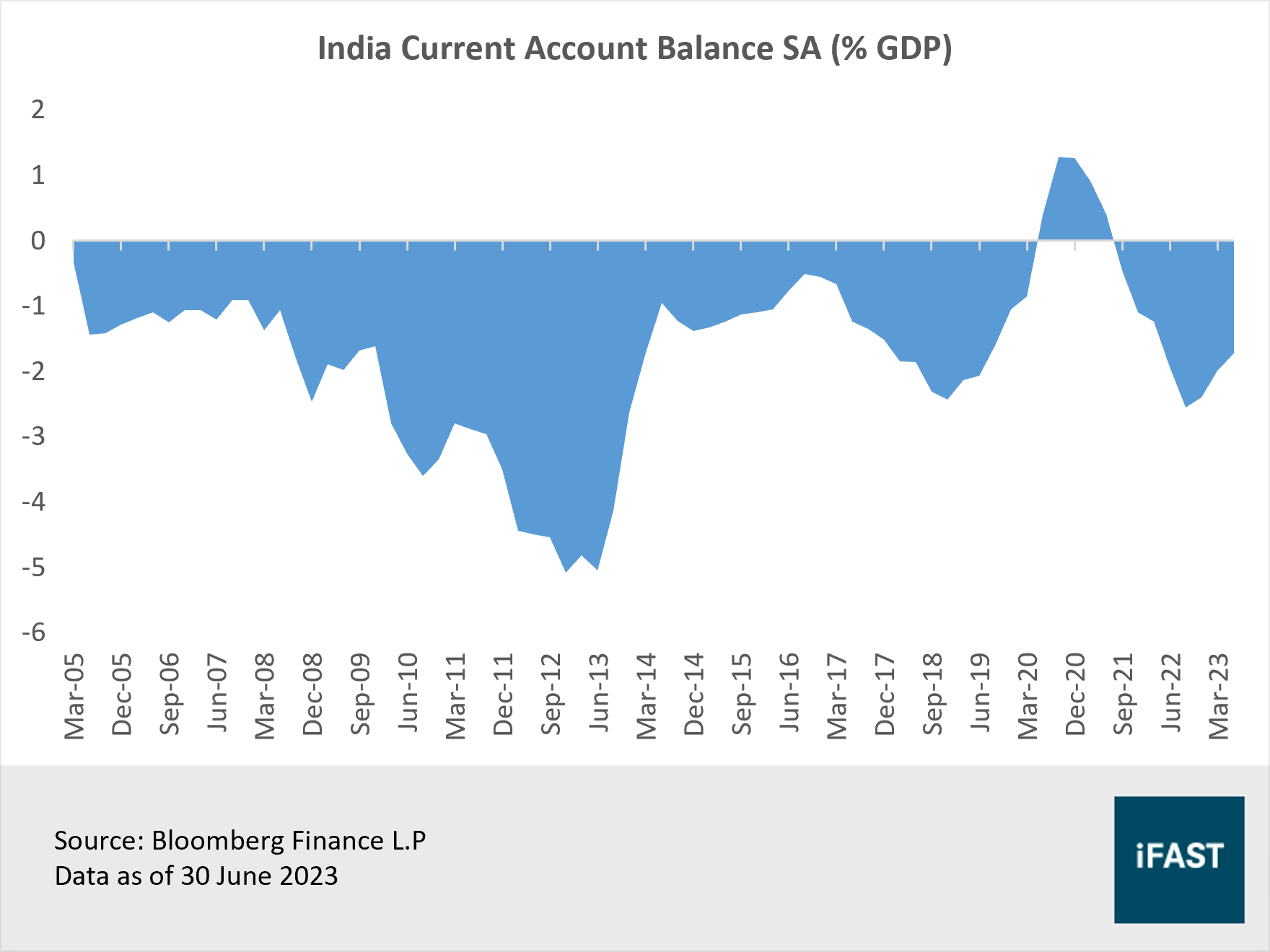

India has a chronic negative current account as a percentage of GDP (Figure 4). The persistent trade deficit has resulted in a consistent depreciation of the Indian rupee, at a rate of 3% per year over the past two decades, making imports more expensive. Coupled with a high commodity bill, a weaker currency contributes to imported inflation, suggesting potential for further deterioration in the country’s trade balance. Such imbalances can impact economic stability and impede overall growth.

Figure 4: India has a persistent negative current account

Another factor holding India back is that of low literacy rates, which impacts productivity growth. India’s literacy remains at 74%, with almost 26% of India’s population lacking any formal education, and this pales in comparison to global literacy rates of 86.3%.

Moreover, India grapples with corporate governance and corruption issues, as exemplified by the Adani scandal. This incident, marked by its political implications due to ties between Adani and Prime Minister Modi, can severely reduce confidence in India’s political system and equity market.

In addition, Indian equities appear relatively expensive compared to the rest of the region. We are hesitant to pay a big premium for Indian equities, especially when considering the challenges that lie on India’s path to becoming a global powerhouse.

(Related article: The Global Economy Needs a New Powerhouse. Can India Step Up?)

More positive on smaller markets

Meanwhile, we hold a more optimistic view on the relatively smaller Asian markets like Taiwan and South Korea, whose economies rely heavily on the global semiconductor demand. Singapore and Malaysia, both integral to global semiconductor supply chain, should also perform well.

Taiwan:

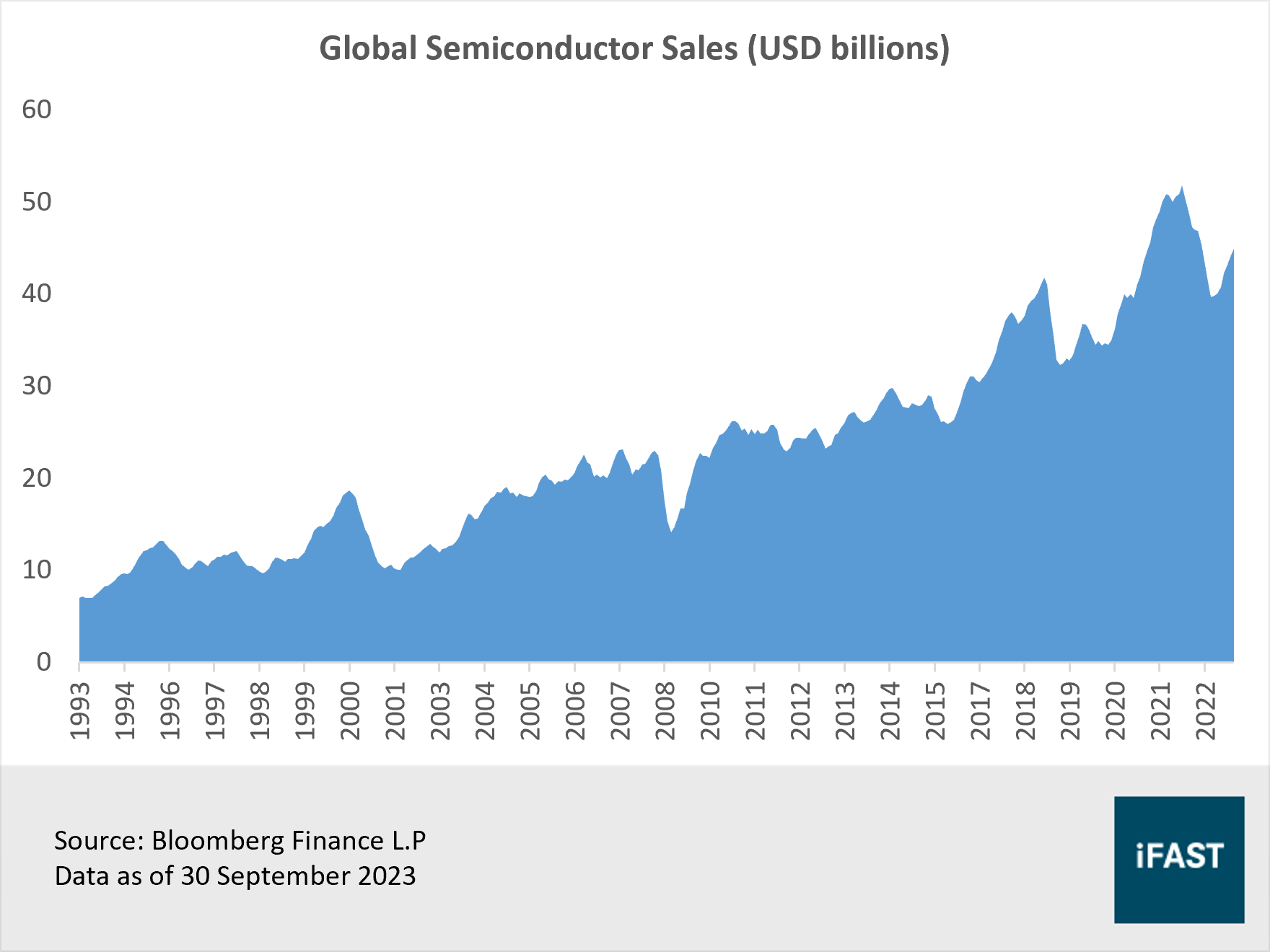

Taiwan’s economy is greatly dependent on the export of semiconductor chips given its status as the global semiconductor powerhouse. After the downturn in semiconductor sales that began in 2022, there are indications of an imminent recovery with monthly semiconductor sales having risen by seven consecutive months (Figure 5). Furthermore, a low base effect is expected to drive higher sales growth going forward.

Figure 5: Monthly semiconductor sales are rising

As the world becomes increasingly tech-driven, the demand for chips is expected to continue to rise. Artificial intelligence (AI) is poised to generate massive demand for semiconductors, following previous technological revolutions like the PC, smartphone, and the internet. We anticipate that the rebound in the semiconductor industry will benefit Taiwan significantly, with companies like TSMC serving as the number one go-to foundry for cutting-edge chips.

However, it is important to note that geopolitics presents the most significant risk for investors. Escalating tensions could trigger a sharp sell-off in Taiwanese equities.

South Korea:

In a similar vein, South Korea is well-positioned to reap the benefits of the global semiconductor sales rebound, given its heavy reliance on the semiconductor exports. Moreover, some of the largest constituents of the KOSPI Index include Samsung and SK Hynix which are important players in the semiconductor sector. Both companies collectively dominate the world’s DRAM production, with market shares of 39.6% and 30.1% respectively as of 30 June 2023.

Over the longer term, the technological dominance of South Korean semiconductor companies will provide them a competitive edge in the global market, especially in the face of on-going US-China tensions.

Nevertheless, it is worth noting that the aforementioned markets have a relatively limited influence on the overall outlook for Asia ex Japan. The combined weight of Taiwan and South Korea in the MSCI AC Asia ex Japan Index is approximately 30%, while Singapore and Malaysia occupy only 4% and 2% of the index respectively (Table 1). These figures are significantly lower compared to the 56% represented by China, India, and Hong Kong which are markets that we approach with caution.

Table 1: iFAST views on Singapore and Malaysia

|

Market |

Weightage in Asia ex Japan |

Star Ratings |

|

Taiwan |

17% |

3.5 Stars - Attractive |

|

South Korea |

14% |

3.5 Stars - Attractive |

|

Singapore |

4% |

3.5 Stars - Attractive |

|

Malaysia |

2% |

3.5 Stars - Attractive |

|

Indonesia |

2% |

2.5 Stars - Neutral |

|

Thailand |

2% |

2.5 Stars - Neutral |

|

China |

35% |

2.0 Stars – Not Attractive |

|

India |

18% |

2.0 Stars – Not Attractive |

|

Hong Kong |

6% |

2.0 Stars – Not Attractive |

|

Source: iFAST Compilations |

||

Consensus earnings estimates for China are too optimistic

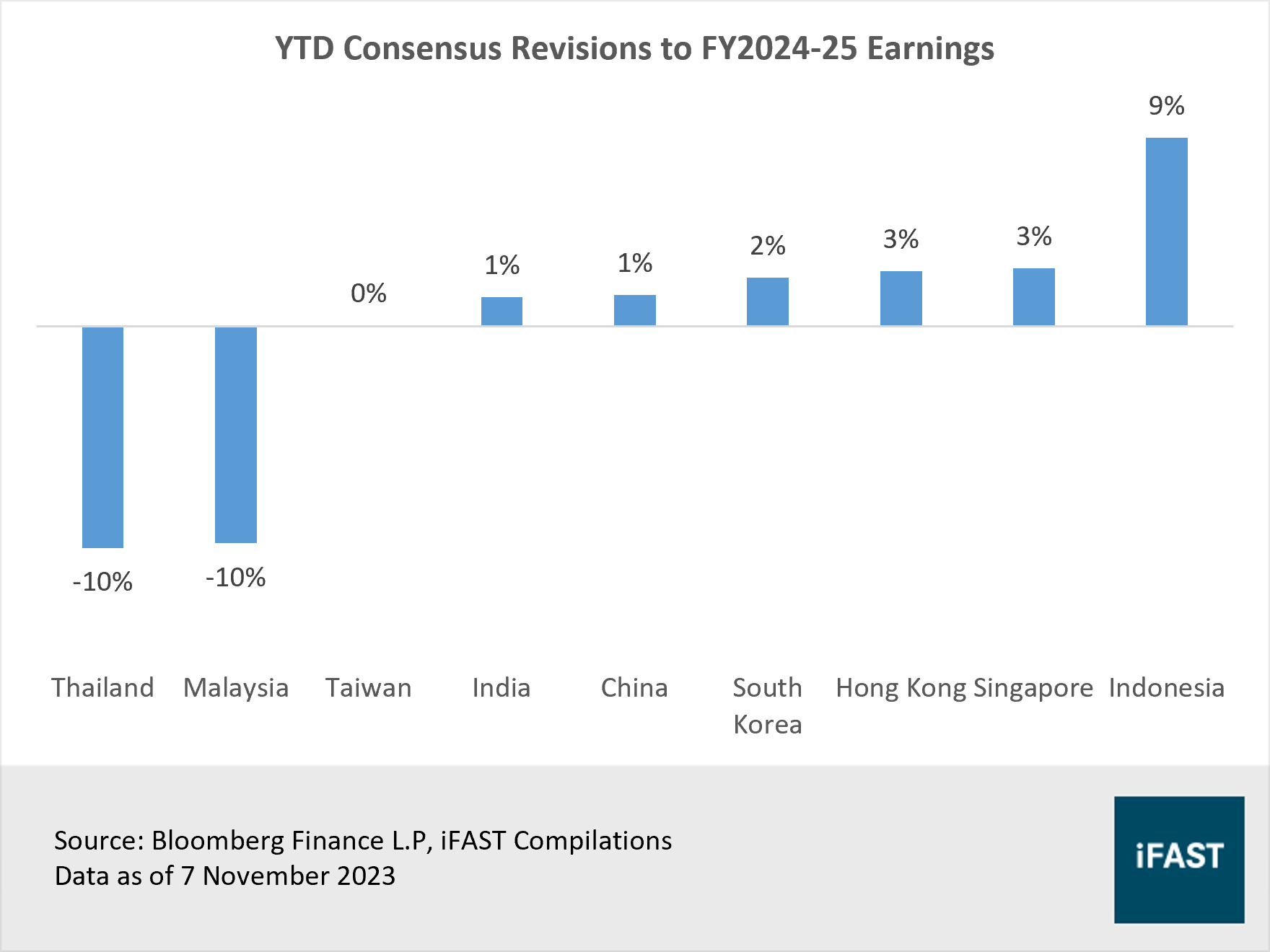

We also observed that both China and Hong Kong have recorded positive consensus EPS revisions YTD, driven by expectations of policy stimulus. Therefore, earnings growth expectations are upbeat, with consensus forecasts indicating double-digit earnings growth of 16% and 15% in China for 2024 and 2025 respectively. However, we believe these estimates are too optimistic.

Given the struggling property market and China’s long-term structural issues, we believe that economic risks in China will persist, thereby dampening the earnings outlook for Chinese corporates. In particular, structural challenges within the property sector will continue to weigh on sectors such as real estate, industrial, and materials, as construction activity remains subdued. This could lead to a reduction in earnings growth expectations, presenting downside risks for Asian equities.

On the other hand, within the Asia ex Japan region, we saw large consensus EPS cuts YTD for Malaysia due to the sluggish external trade activity recovery. Meanwhile, Taiwan saw little to no revisions. Nevertheless, we think the markets are poised for future earnings upgrades, underpinned by the anticipated recovery in the semiconductor industry. Additionally, receding fears of a recession in developed markets are expected to lift export revenues, boosting economic growth.

Figure 6: Earnings revisions YTD

Valuations are not cheap

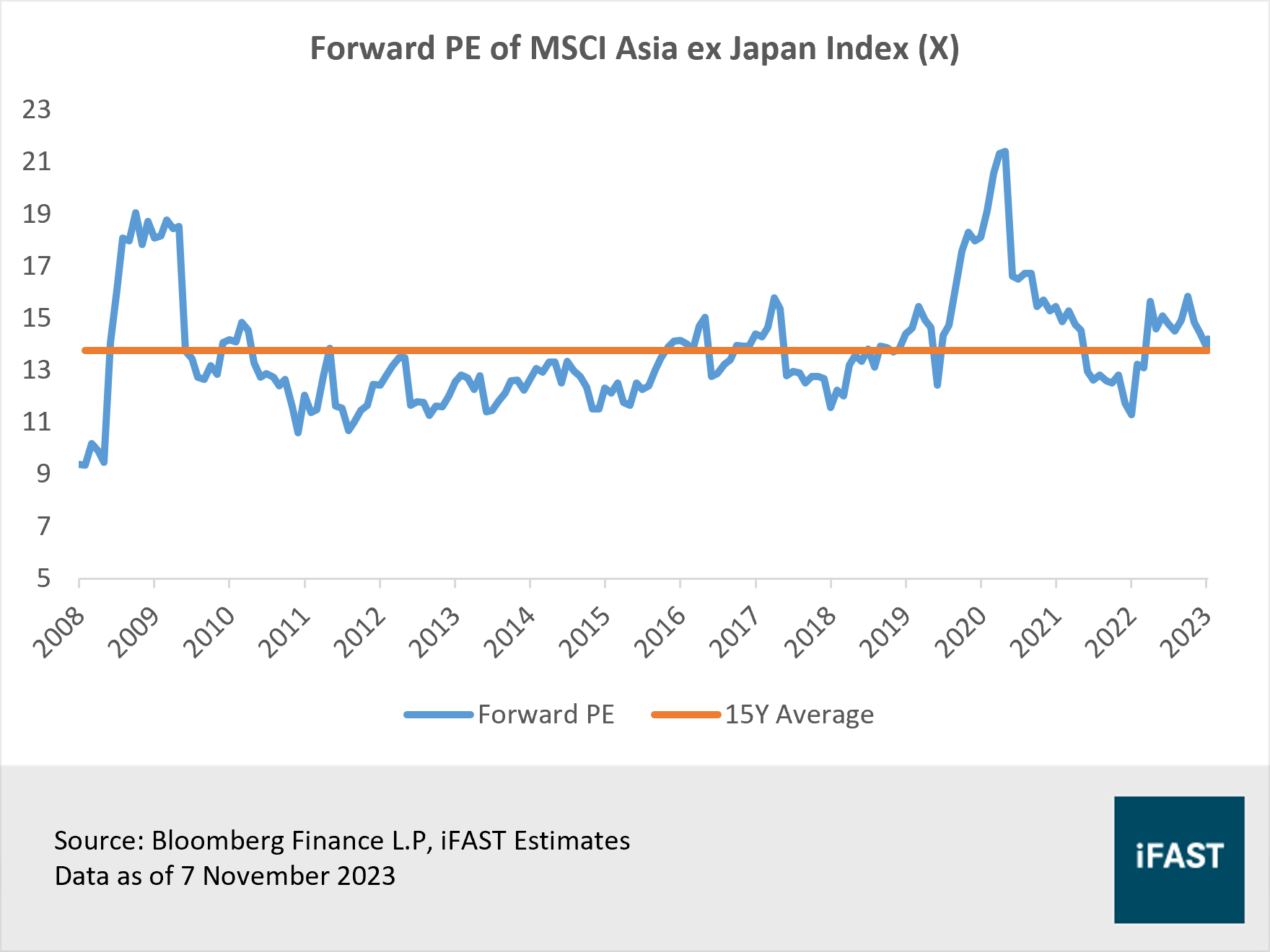

In terms of valuations, despite this year’s underwhelming performance, Asian equities are no longer cheap by historical standards. The region currently trades at a forward PE of 14.2X, representing a slight 3% premium over the 15Y historical average (Figure 7). With the lack of margin of safety for Asian equities, we believe investors are exposed to negative price reactions that could result from a disappointing macro backdrop particularly in China.

Figure 7: Current valuations provide no margin of safety

We anticipate that overall earnings growth for the region will be hampered by the impact from China. Consequently, our earnings estimate for Asian equities are more conservative compared to the consensus. We expect EPS to decline by nearly -5% this year, before experiencing a growth of 11.3% and 7.7% in the next two years respectively, on the back of a semiconductor-driven recovery in Taiwan and South Korea.

Based on our fair PE ratio of 13.5X, we project a target price of 692 for the MSCI AC Asia ex Japan Index, translating to a limited upside potential of 14% by 2025. We maintain our 2.5 Stars “Neutral” view for the region.

Table 2: Earnings projection

|

MSCI AC Asia ex Japan Index |

2022 |

2023E |

2024E |

2025E |

|

PE Ratio (X) |

13.8 |

14.2 |

12.8 |

11.9 |

|

Earnings Per Share |

44.88 |

42.80 |

47.63 |

51.28 |

|

Earnings Growth |

-11.2% |

-4.6% |

11.3% |

7.7% |

|

Target Price (based on 13.5X fair PE ratio) |

692 |

|||

|

Potential Upside |

14% |

|||

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 7 November 2023 |

||||

In a nutshell, we believe the prospects for Asian equities remains cloudy given our cautious stance on key Asian markets like China and India. Alongside unattractive valuations for the region, we think better opportunities could be found at the country/market level. Within the markets in Asia ex Japan, we prefer South Korea, Singapore, Taiwan, and Malaysia.

Table 3: Recommended products

|

Market |

Unit Trust |

ETF |

|

Asia ex Japan |

||

|

South Korea |

||

|

Singapore |

||

|

Taiwan |

- |

|

|

Malaysia |

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.