• Heavily reliant on exports, Taiwan’s economy is set to see tepid growth in the near-term as trade continues to slow amidst a cooling global economy.

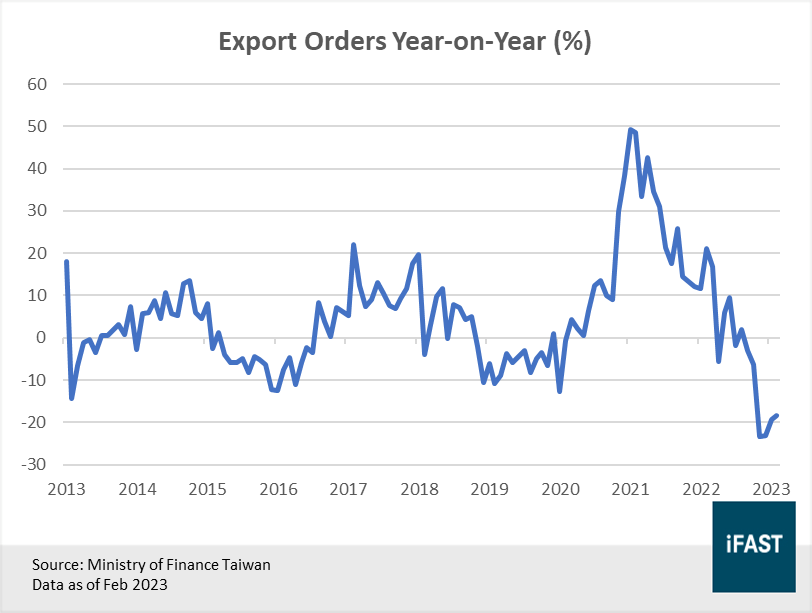

• New export orders have fallen rapidly by -18.3% year-on-year in Feb 2023, one of the lowest points in over a decade. Export orders for electronics fell by -22%.

• Taiwan’s significant exposure to the semiconductor industry, which is undergoing a down-cycle, has also added to its trade woes.

• As inflation in Taiwan is relatively benign compared to other major economies, the central bank can afford to keep monetary policy loose, helping to support consumption.

• The estimated upside potential for Taiwan is 31%. We have downgraded our rating by one notch to 3.5 Stars “Attractive” from the previous rating of 4.0 Stars “Very Attractive”.

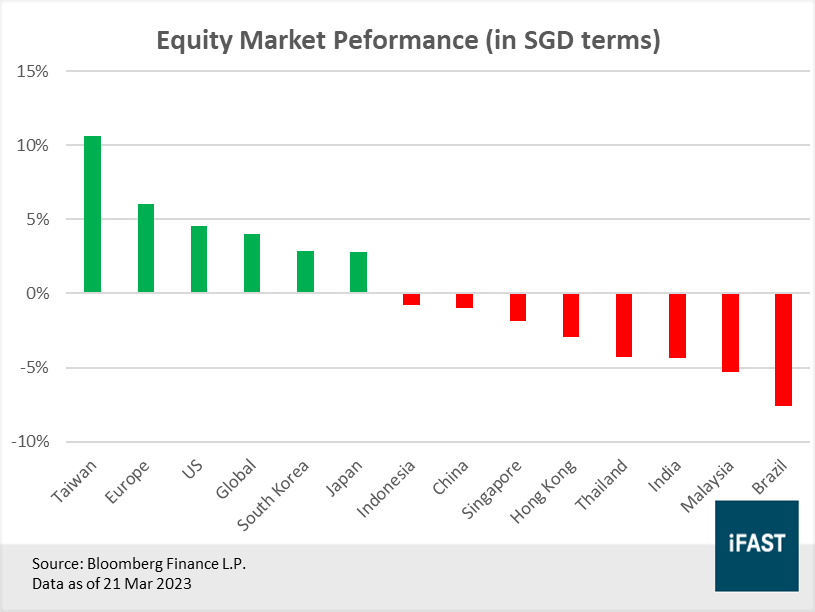

Despite a choppy 2022 for global equities, Taiwan has bounced back to become one of the top performing equity markets this year. As of 21 Mar 2023, the benchmark TWSE Index has risen by more than 10% year-to-date, more than double the returns of the MSCI AC World Index (Figure 1). But with the global economy cooling rapidly, Taiwanese companies, many of which are heavily dependent on trade, will likely face greater headwinds in the near-term.

As such, we have downgraded Taiwan from its current rating of 4.0 Stars “Very Attractive” to 3.5 Stars “Attractive”. In this article, we lay out our rationale for doing so.

Figure 1: Taiwan is one of the top performing equity markets year-to-date

Economy to face challenges as trade headwinds mount

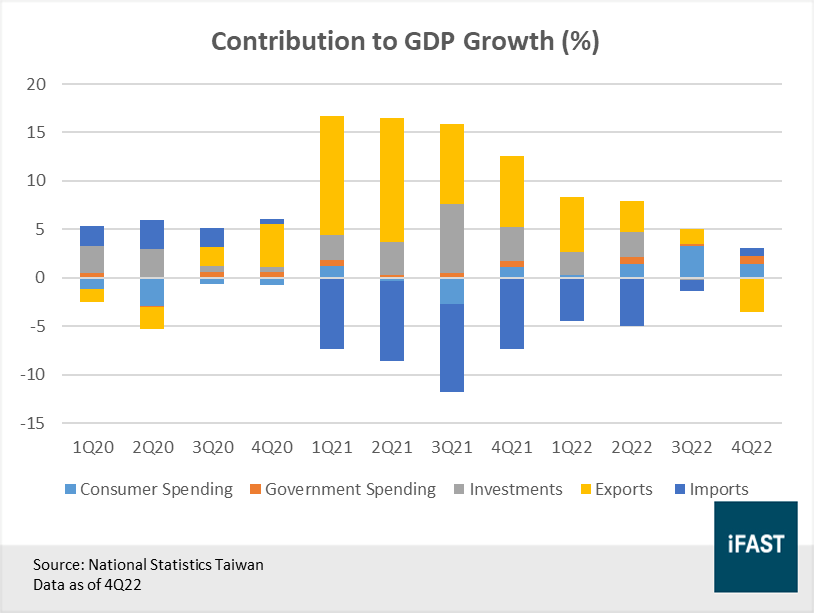

According to data released by the Taiwanese government, Taiwan’s GDP fell by -0.41% year-on-year in the final quarter of 2022, compared to a growth of 3.64% in the previous quarter. This brings the island’s 2022 full year GDP growth rate to 2.45% year-on-year, down substantially from 6.57% in 2021.

The fourth quarter decline was largely driven by a significant slowdown in exports, which took away -3.43% from the overall growth rate. Even though private consumption and government spending added 1.44% and 0.83% to growth respectively, it was not enough to offset the sizeable negative contribution by exports.

Figure 2: Negative contribution by exports weighed heavily on Taiwan’s 4Q 2022 GDP numbers.

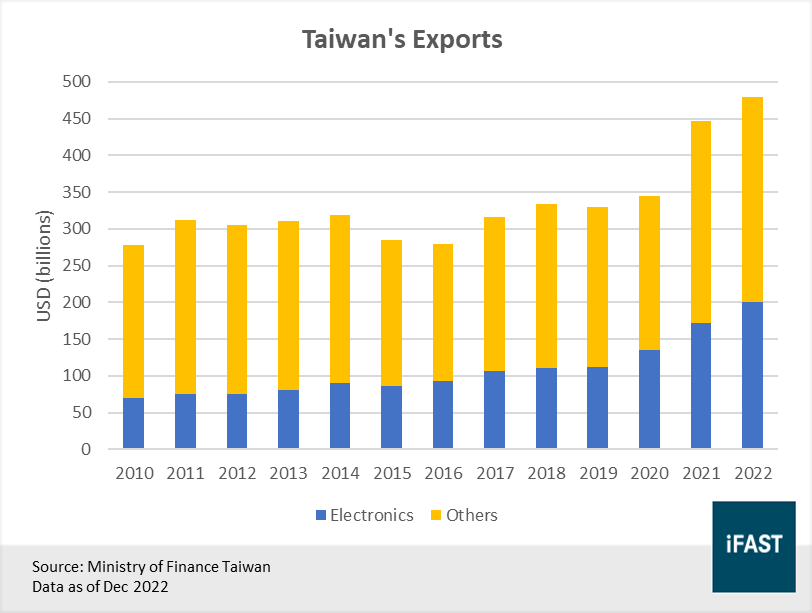

As a relatively small and open economy, Taiwan is heavily dependent on global trade, with exports making up roughly 70% of its GDP. Depending on the prevailing economic conditions, this can either be Taiwan’s greatest strength or its greatest weakness. During the early days of the pandemic, Taiwan’s heavy exposure to exports was certainly one of its greatest strengths as it benefitted immensely from soaring demand for its goods, particularly semiconductors and other electronic products (Figure 3).

Figure 3: Electronic exports make up more than 40% of Taiwan’s total exports

With much of the world stuck at home due to the pandemic and trends such as remote working gaining traction, consumer electronics were in hot demand. On the business front, the pandemic was also a catalyst that sparked a wave of digitalisation across multiple industries, with many companies adopting and investing heavily in digital solutions to cater to remote working and also to remain competitive in the post-pandemic era.

The surge in consumer and business spending were partly helped by easy monetary policies and the massive pandemic stimulus packages handed out by world governments. As a result, Taiwan’s total exports saw significant growth (CAGR +13.3%) over the past three years, rising from USD 329 billion in 2019 to USD 479 billion by the end of last year. Electronic exports did even better, achieving a CAGR of 21% over the same period.

But as we head further into 2023, there are unmistakable signs that things have already started to head in the opposite direction. Since early last year, new export orders have fallen rapidly, with February’s -18.3% year-on-year decline being one of the lowest points in over a decade (Figure 4). Most notably, export orders for electronics fell by -22% in Feb 2023. At a country/regional level, Taiwan’s three largest trading partners (China, ASEAN, and the US) saw export orders declining by -30%, -11% and -14% respectively.

Figure 4: New export orders in Feb fell by close to -20%, one of the lowest points in over a decade

While the massive amount of pandemic stimulus has helped the global economy get back on its feet, it has also created an unintended consequence – inflation. Throughout 2022, inflation across most major economies has surged to multi-decade highs, forcing central banks to respond by raising interest rates. As a matter of fact, policy has never tilted so overwhelmingly towards rate rises in the past five decades, with nearly every major economy having tightened monetary policy.

With inflation still well above the central bank target rate in most places, we expect interest rates to stay higher for longer. Furthermore, as the impact of higher interest rates have yet to be fully felt, the drag on economic activity will intensify in the quarters ahead. Global trade is expected to remain sluggish. Following the slump in exports, the Taiwanese government has cut its GDP forecast for 2023 down to 2.12%, from the previous estimate of 2.75% back in November 2022.

Weak demand for semiconductors adds to Taiwan’s trade woes

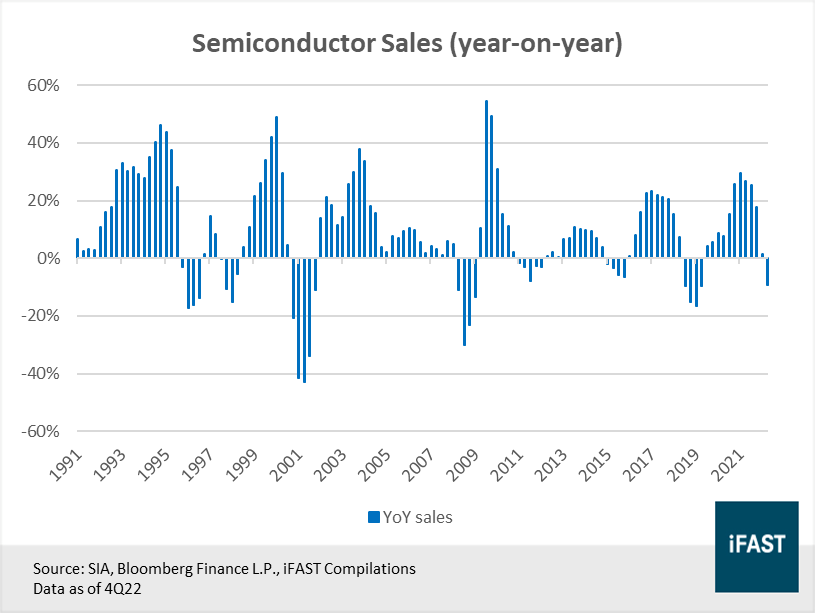

Taiwan is the world’s semiconductor powerhouse. The island is estimated to produce over 60% of the world’s semiconductors, including more than 90% of the most cutting edge chips. As such, the fate of its economy is closely tied to that of the semiconductor industry. Unfortunately for Taiwan, the global semiconductor industry is currently in the midst of a down-cycle.

After hitting a high of 29.5% in 3Q21, global semiconductor sales growth has been sliding, falling as low as -9.4% in 4Q22. This marked the first time sales growth has ventured into negative territory since the beginning of 2020 (Figure 5). According to data published by IDC, shipments of PCs, smartphones, and wearables have all declined in 2022. With the pandemic boom behind us and a global recession looming, shipments of consumer electronics are likely to remain weak in the months ahead as suppliers halt new orders and slash prices to get rid of excess inventory.

Figure 5: Semiconductor sales fell by nearly -10% in the final quarter of 2022

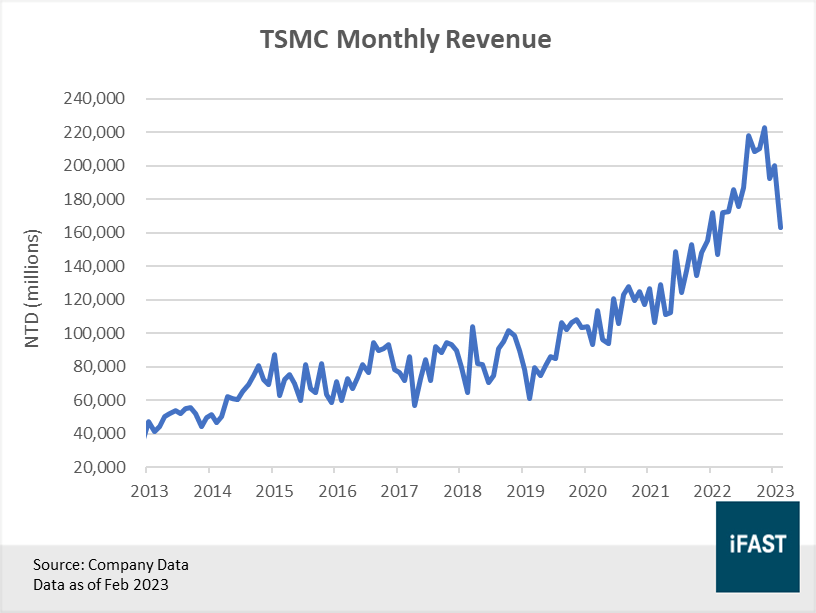

The latest earnings results of Taiwanese foundries corroborates this. In a recent earnings call, the CEO of TSMC said that demand for the consumer end market segment continues to remain soft, while enterprise-driven end market segments (e.g. data centres), which were more resilient at the beginning of 2022, have softened as well. Capacity utilisation rates have also fallen to lower levels than previously anticipated. Sentiment from UMC, the second largest foundry in Taiwan, is more or less similar, with management warning of weaker demand ahead.

Looking ahead, TSMC intends to tighten capex spending given the near-term uncertainties. Based on management guidance, 1Q23 revenue is expected to be about -15% lower than the previous quarter, while operating margins should see a significant drop from the current 52% to 42% due to lower capacity utilisation rates and higher expenses associated with overseas fab expansion.

Figure 6: TSMC’s monthly sales have begun to falter as the down-cycle plays out

Even though the outlook for global trade looks rather gloomy at the moment, it should only be a matter of time before things recover. Setting our sights further, we expect the turnaround in the semiconductor industry to benefit Taiwan significantly. With no real competitor in sight, TSMC is still the number one go-to foundry for cutting edge chips. TSMC’s huge weighting of approximately 30% within the TWSE index is also one of the reasons why we continue to remain optimistic on Taiwanese equities in the long run despite the uncertainties in the near-term.

Consumption supported by benign inflation and relatively looser monetary policy

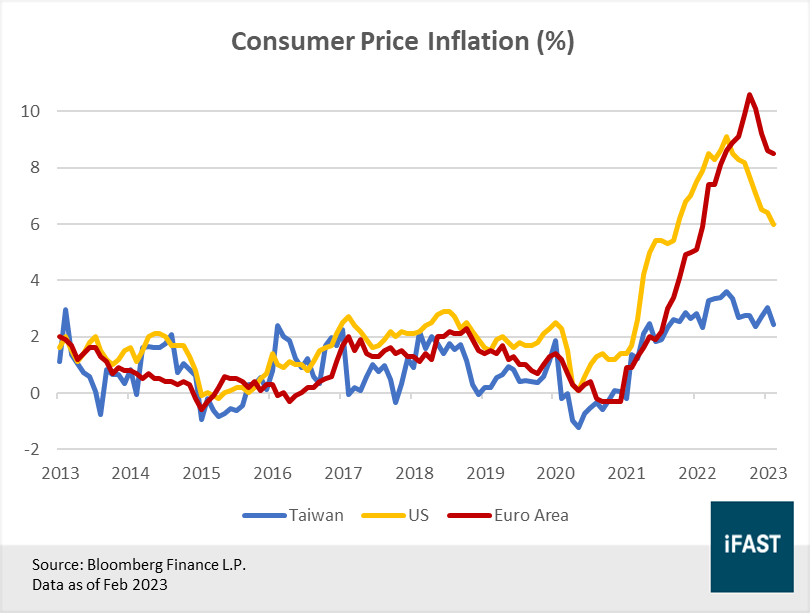

Taiwan’s consumer price inflation eased to 2.43% in Feb 2023, just slightly above the central bank’s unofficial target of below 2%. With global growth slowing and fewer disruptions in supply chains, inflation in Taiwan is projected to reach 1.9% by the end of 2023. Unlike other major economies such as the US and the Eurozone, where inflation is still far from the target rate and proving to be much more stubborn than expected, inflation in Taiwan is still relatively benign (Figure 7).

Figure 7: Taiwan’s inflation is relatively mild compared to other major economies

As such, Taiwan’s central bank will have more leeway to keep monetary policy loose compared to other markets, which should help to support equity valuations. Additionally, lower inflation and looser monetary policy will also help to support consumption in the meantime while exports face headwinds.

After falling throughout the most of 2022, consumer sentiment in Taiwan is showing signs of a rebound, having risen for two consecutive months to reach 62.47 in February, the highest in five months. Lower inflation is also a positive for real wages, adding to the strength of Taiwanese consumers.

Key investment risks

Geopolitical risks: Situated between the US and China (both figuratively and literally) Taiwan is at the epicentre of geopolitical risk. As of late, the US has been pressuring its allies (including Taiwan) to stop supplying China with advanced semiconductors, while the latter seeks to build up its domestic capabilities. Rising tensions, or the outbreak of war, will definitely lead to a steep sell-off in Taiwanese equities.

Prolonged/deep recession: As it stands, the global economy is likely to experience a shallow recession. However, the possibility of a prolonged and deep recession is not out of the question. If this were to occur, Taiwan’s trade-reliant economy will most likely face even greater headwinds ahead and take longer than expected to recover.

Downgrade to 3.5 Stars “Attractive”: Lower upside potential but valuations remain compelling

While the chances of an armed conflict between China and Taiwan are low at this point, it is no longer a remote possibility. Besides, China has increasingly been using “grey-zone tactics” – coercive activities that do not amount to an armed conflict – to blockade Taiwan and disrupt its economy. In order to factor in the greater geopolitical risk for Taiwanese equities, we have lowered out fair PE multiple from 18X to 17X. After applying our new designated fair PE multiple of 17X on 2024E EPS, we arrive at a target price of 20,251 for the TWSE Index – representing an upside potential of approximately 31%.

Table 1: Earnings growth for Taiwanese equities are expected to be hit hard by the weakening trade outlook

|

TWSE Index |

2022 |

2023E |

2024E |

|

EPS |

1381.13 |

1035.85 |

1191.22 |

|

EPS Growth |

13.16% |

-25% |

15% |

|

PE Ratio (X) |

10.24 |

14.89 |

12.94 |

|

Upside Potential (Based on 17X Fair PE) |

- |

- |

31.34% |

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 21 Mar 2023 |

|||

With the weakening trade outlook and a global recession looming, there will be plenty of challenges for Taiwan in the near-term. With this in mind, we have lowered our earnings growth estimates for 2023. In the long run, we expect Taiwan to benefit from the recovery in global trade as well as the turnaround in the semiconductor industry. If all goes well, Taiwan should see a healthy recovery in 2024.

Even after making adjustments to our fair PE multiple and earnings growth estimates, Taiwanese equities still possess decent upside potential of about 31%. Following these adjustments, we have also downgraded Taiwan to 3.5 Stars “Attractive” from the previous rating of 4.0 Stars “Very Attractive”.

Although the upside potential may not be as attractive as before, we still think that investors should keep an eye out for Taiwan, given its potential to outperform during economic expansions. Investors who are interested in Taiwan may want to consider our recommended ETF – the iShares MSCI Taiwan ETF (NYSE:EWT).

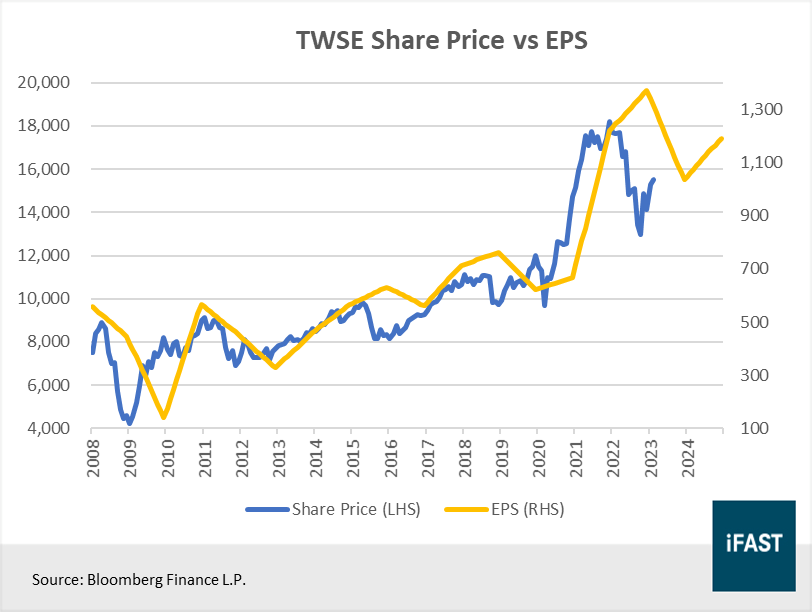

Figure 8: In the long run, share prices are driven by earnings

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.