• South Korea narrowly avoided a recession after it delivered growth of 0.3% in 1Q23. However, it remains to be seen if positive growth can be sustained in such a challenging global environment.

• Manufacturing PMI has remained in contractionary territory for the tenth straight month, following a fall in new orders and output. Korea’s significant exposure to the memory market also adds to its trade woes.

• While the Bank of Korea has dismissed the idea of a rate cut, falling inflation should at least allow the central bank to pause rate hikes, which should lend support to consumption and growth.

• Despite the near-term headwinds, Korean equities are still relatively attractive with an upside potential of approximately 34% for the KOSPI. Maintain rating of 3.5 Stars “Attractive”.

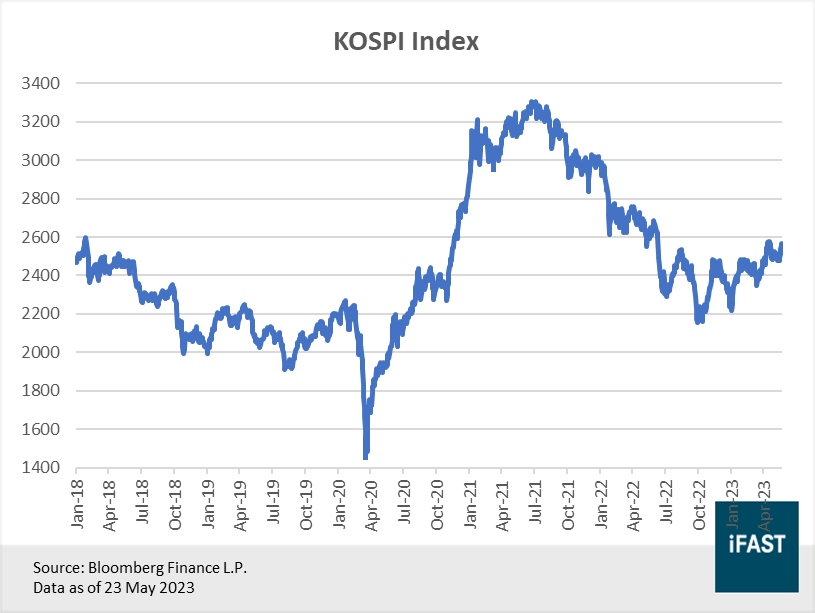

Like most equity markets, South Korea had a tough year in 2022, with the KOSPI falling by nearly -25%. This year, it has managed to recover some of the losses, rising by approximately 13% year-to-date (Figure 1). Despite the positive performance of Korean equities in 2023, we foresee tougher times ahead for Korea’s trade dependent economy as global growth slows. Moreover, with the down cycle in the semiconductor industry adding to the country’s woes, Korean equities should have limited upside in the near-term.

However, in the long run, we continue to remain positive on Korean equities as valuations are still attractive and because the country is well positioned to reap the benefits of the rebound in global trade – especially for semiconductors.

Figure 1: Korean equities are likely to face some headwinds in the near-term

South Korea narrowly avoided a recession, but shrinking exports adds to the near-term uncertainty for trade

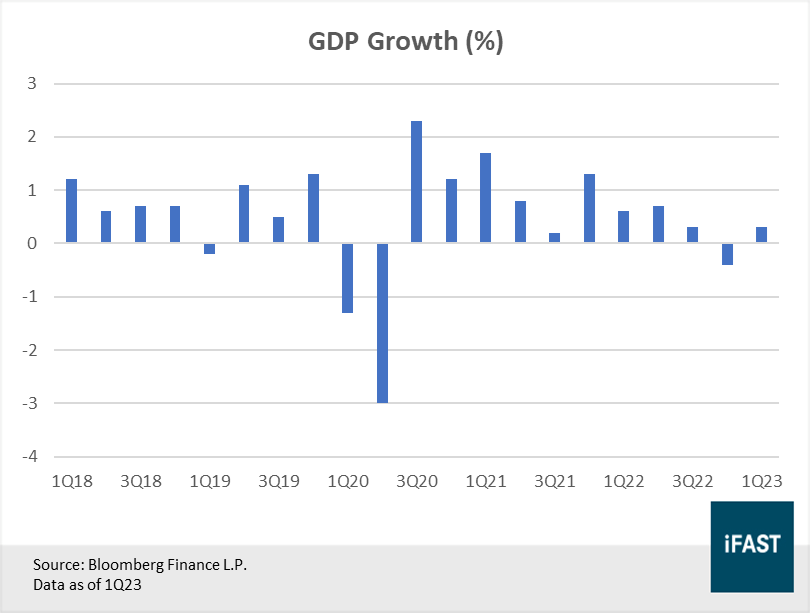

South Korea narrowly avoided a recession after delivering GDP growth of 0.3% in the first quarter of 2023, rebounding from a -0.4% contraction in the final quarter of the previous year (Figure 2). The latest results were also slightly stronger than the median consensus forecast for a 0.2% expansion, though it remains to be seen if positive growth can be sustained, especially in such a challenging global environment.

The biggest contributor to 1Q23 GDP was private consumption, which rose by 0.5% quarter-on-quarter, after a decline of -0.6% in 4Q22. South Korea continues to enjoy the benefits of the post pandemic recovery, as consumer expenditure on services such as travel and leisure increased – partly due to higher tourism revenues. Exports, on the other hand, rose 3.8% quarter-on-quarter helped by higher shipments of cars and machinery. However, on a year-on-year basis, they were still down by -3.0%, whereas imports were up by 4.4%.

Figure 2: South Korea delivered slim growth in 1Q23, narrowly avoiding a recession

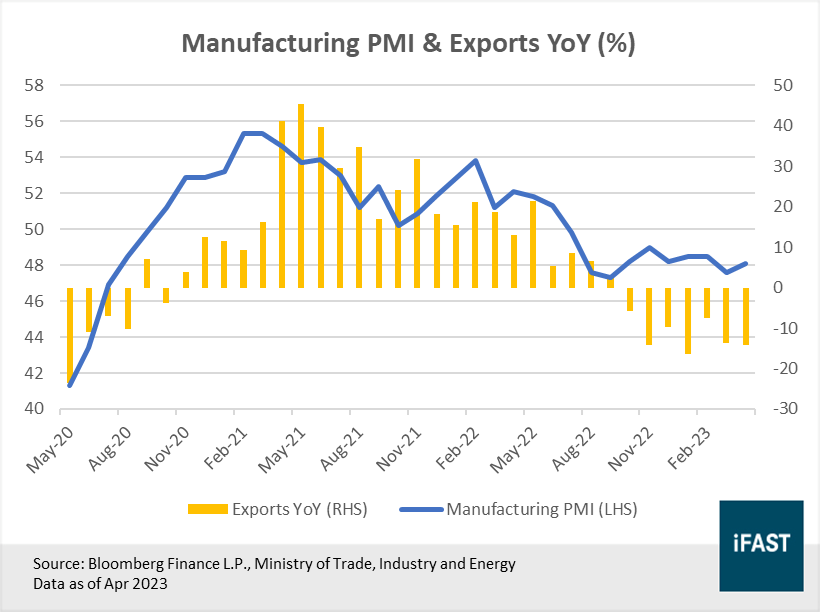

Looking at the monthly data, we observe that Korean exports fell -14.2% year-on-year in April, following a -13.6% decline in the previous month (Figure 3). This is one of the steepest declines in recent history, not to mention the seventh consecutive month exports have fallen. The cooling global trade outlook reflects the headwinds faced by Korean exporters, particularly the manufacturing sector.

In the month of April, manufacturing PMI came in at 48.1 - slightly higher than a reading of 47.6 in March, pointing to a softer deterioration in the sector’s health. Nonetheless, the manufacturing sector has remained in contractionary territory for the tenth straight month. Taking a closer look at the various components, new orders (both foreign and domestic) and output fell as demand remains subdued – largely attributed to the weakening global economy. In March, Korea’s industrial production decreased by -7.6% year-on-year, while its manufacturing capacity utilisation rate has fallen to 72.2%, compared to 78.7% a year ago.

Figure 3: Korea’s manufacturing PMI remains in contractionary territory as demand for exports remains subdued

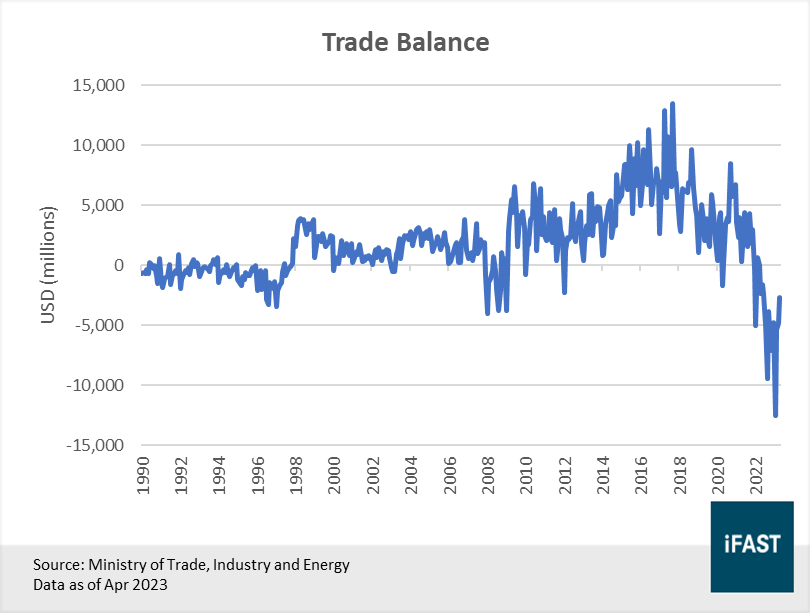

Overall, the rapidly cooling global trade outlook has resulted in Korea recording a trade deficit for 13 straight months – the longest streak since the late 1990s (Figure 4). For a country like Korea which relies heavily on exports for growth, carrying a negative trade balance for a prolonged period can be very damaging to its economy.

Figure 4: As of April 2023, Korea has carried a trade deficit for 13 straight months

Korea’s trade woes are compounded by its significant exposure to memory chips

Korea’s trade woes are compounded by its significant exposure to semiconductors, particularly the memory chip segment where prices tend to be more volatile. According to estimates by TrendForce, Korea controls the majority of the world’s DRAM and NAND production, with a market share of roughly 70% and 50% respectively as of the third quarter of 2022.

The majority are produced by two key companies - Samsung and SK Hynix. The duo also happens to be the largest and third largest constituent of the KOSPI index with a combined weight of close to 25%. Due to their significant weighting, it should not come as a surprise that the overall performance of the KOSPI is highly dependent on the performance of these two companies, and by extension the outlook of the semiconductor industry.

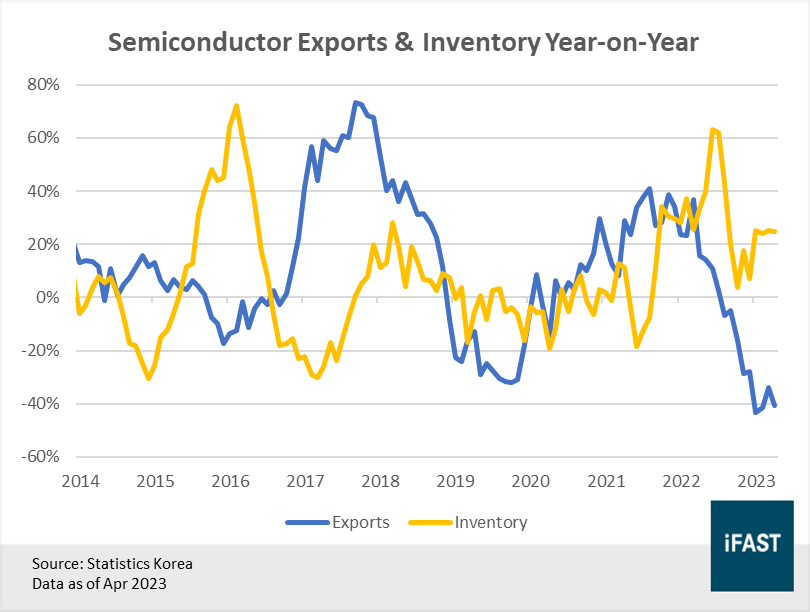

Unfortunately, the chip industry is currently in the midst of a cyclical downturn with sales growth tumbling by near double digits as of 1Q23. Based on the latest trade statistics, Korea’s semiconductor exports dived -41% while inventory levels rose by 23.4% year-on-year in April as demand for chips falters (Figure 5).

Figure 5: Korea’s chip exports dived while inventory levels rose as demand falters

According to the latest financial results, Samsung’s semiconductor division booked an operating loss of USD 3.4 billion in 1Q23, the company’s first loss in 14 years. Its rival SK Hynix did no better, as it posted an operating loss of USD 2.6 billion over the same period. Unlike Samsung who is a conglomerate with multiple business units, SK Hynix’s revenue comes entirely from the production of memory chips, and therefore is more vulnerable during downturns.

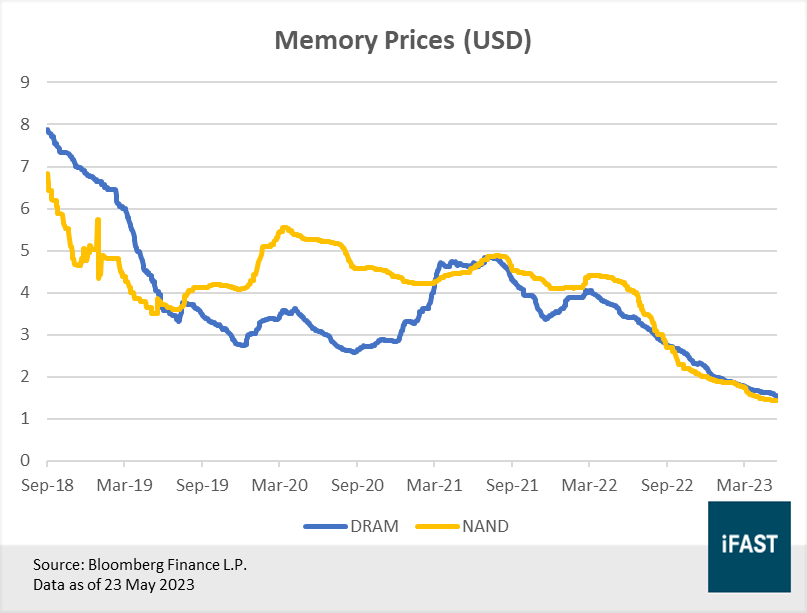

Both companies blamed the ongoing inventory adjustment as well as sluggish demand due to the global economic slowdown for their lacklustre earnings results last quarter. Memory chips have also experienced a significant correction in average selling prices (ASP), resulting in higher inventory valuation losses for both chipmakers. Between July 2021 and May 2022, memory prices have fallen by nearly -70% on average (Figure 6).

Figure 6: Memory prices have tumbled by close to 70% since July 2021

Even so, we remain positive on the long-term growth prospects for the chip industry and Korea. Looking forward, semiconductor demand will eventually recover to higher levels than before driven by structural factors such as (i) an increase in the number of semiconductor applications, and (ii) the increase in silicon content in them.

Samsung & SK Hynix pointed out that future demand for memory chips will be driven by the launch of new smartphones as well as the shift towards high density & performance memory such as DDR5. The rapid rise of generative AI systems such as ChatGPT and its counterparts will also boost demand for high core CPUs, where the silicon content per box is much higher than before. NVIDIA’s latest financial results and forecast for AI chip demand certainly adds to the optimism. Based on the guidance provided by both companies, semiconductor sales is expected to see a gradual recovery as early as the latter half of 2023, once the existing inventories have been properly digested.

Related Article: Stop trying to catch the bottom. The time to start buying semiconductor stocks is now

Improving domestic conditions bodes well for Korea

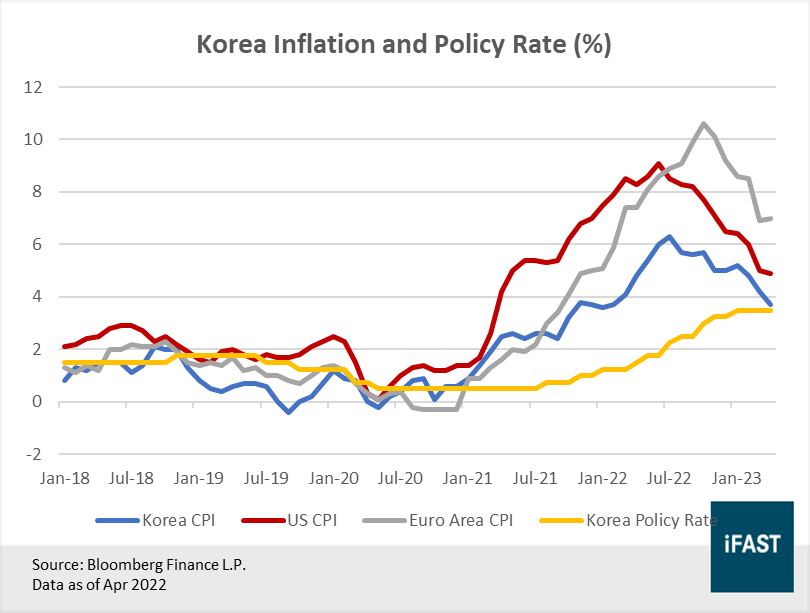

Balancing the challenging external environment is the improving domestic conditions in Korea. Inflation in Korea has been falling steadily, from a peak 6.3% in July 2022 to just 3.7% in April 2023. This is in contrast to other countries such as the US and those in the Eurozone where inflation remains well above their respective target rates (the ECB, US Fed and the Bank of Korea all have an inflation target of 2%).

Even though the Bank of Korea has dismissed the idea of a rate cut, calling it too premature, falling inflation should at the very least allow the central bank to put a pause to rate hikes, which would help to support consumption and economic growth. As of April 2023, the Bank of Korea has left its policy rate unchanged for the past three meetings at 3.5% (Figure 7).

Figure 7: Falling inflation should allow the Bank of Korea to pause rate hikes

Another sign that things are starting to turn around for Korea is the improvement in the Leading Economic Index (LEI). As of March, the LEI has increased by three consecutive months, which suggests that the growth prospects of Korea are starting improve, with four out of six components contributing positively to the LEI.

Key investment risks

Geopolitical risks: Just recently, China imposed a ban on the use of Micron’s memory chips in certain key domestic sectors, citing security risks. China’s latest move is seen as a form of retaliation after the US imposed a series of export controls, preventing its companies and allies from shipping advanced semiconductors to China. While this can potentially be an opportunity for Korean chipmakers to increase their market share, the US has urged Korea to not fill any market gaps left by Micron. If Korea sides with the US, it may trigger some form of retaliation from China which would likely be detrimental to Korea’s economy given that China is still its largest trading partner.

Deep recession: As it stands, the global economy is likely to experience a shallow recession. However, the possibility of a deep recession is not out of the question. If this were to occur, South Korea’s export-oriented economy would face even greater headwinds and take longer than expected to recover.

Maintain rating of 3.5 Stars “Attractive” – Long-term outlook remains promising

Even though Korean equities have done quite well so far this year, deteriorating trade conditions will likely lead to greater headwinds for exporters, especially for the manufacturing sector. On top of that, Korea’s significant exposure to semiconductors - memory chips in particular - will also weigh heavily on its outlook as the entire industry undergoes a down-cycle.

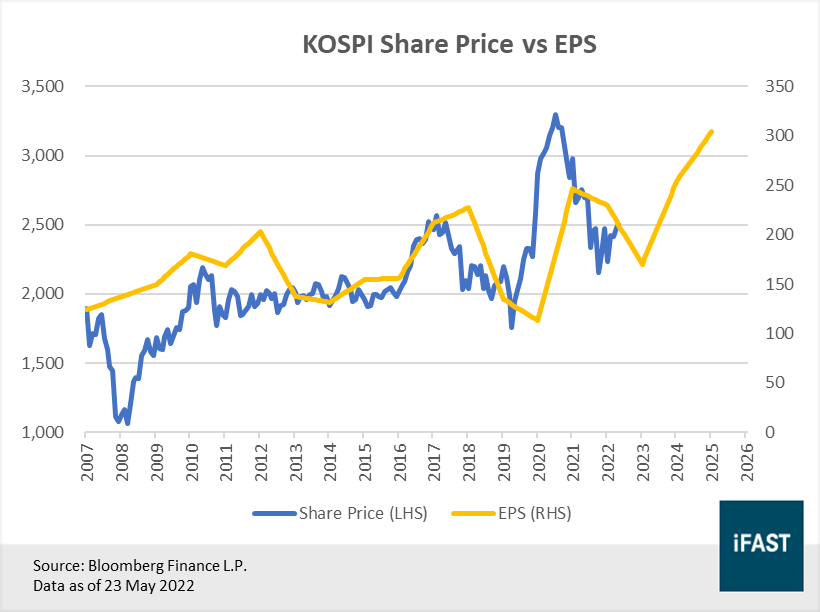

Given the challenges the country faces in the near-term, earnings growth is unlikely to be as robust as before. As a matter of fact, we expect to see negative earnings growth for Korean equities this year (which would make them look less attractive in the near-term) before a subsequent recovery in 2024 and 2025 as global trade normalises.

Despite the challenging near-term outlook, the relatively lower valuations of Korean equities means that investors can potentially realise larger profits if they are willing to stretch their investment horizon out further. Applying our designated fair PE multiple of 12X on 2025E EPS, we arrived at a target price of 3428 for the KOSPI Index. This implies an upside potential of approximately 34%. As such, we will be retaining our rating of 3.5 Stars “Attractive” for the market.

Investors who wish to invest in Korea may consider the iShares MSCI South Korea ETF (NYSE:EWY). Alternatively, those who are seeking exposure only to the semiconductor industry can go for the VanEck Semiconductor ETF (NASDAQ:SMH), which tracks a basket of 25 of the largest and most liquid semiconductor companies that are listed in the US.

Table 1: Earnings growth likely to be weaker in the near-term as trade headwinds mount

|

KOSPI |

2022 |

2023E |

2024E |

2025E |

|

EPS |

229.64 |

172.23 |

246.29 |

285.70 |

|

EPS Growth |

-6.7% |

-25.0% |

43.0% |

16.0% |

|

PE Ratio (X) |

9.74 |

14.87 |

10.40 |

8.97 |

|

Upside Potential |

- |

- |

- |

33.83% |

|

Source: Bloomberg Finance L.P. Data as of 23 May 2023 |

||||

Figure 8: Share price vs. earnings for the KOSPI index

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in the VanEck Vectors Semiconductor ETF.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.