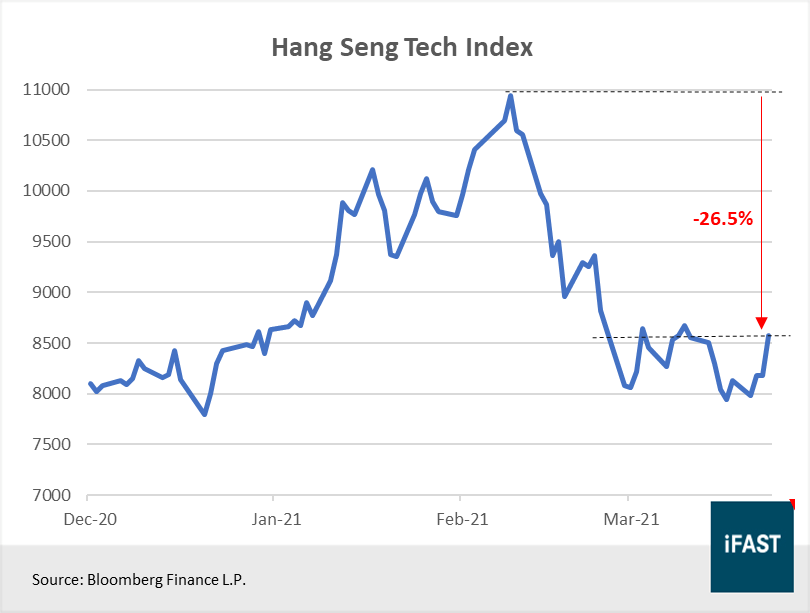

• Struck by a barrage of negative news, the share prices of Chinese tech companies have fallen, dragging the Hang Seng Tech index down by more than -25% since its peak in February.

• The purpose of increased regulation is meant to safeguard consumers and promote healthy competition within China’s tech sector, not to stop its growth.

• Sanctions on Chinese tech firms will compel China to double down on its efforts to become technologically self-sufficient, a goal which it will eventually achieve.

• We view the recent sell-off as an opportunity for investors to accumulate more shares, as the long-term growth story of this sector remains intact.

• Our target price for the iShares Hang Seng Tech ETF is HKD 25, which represents an upside potential of close to 50%.

Recently, Chinese tech companies have been hit by a string of bad news, beginning with the government pulling the plug on Ant Group’s USD 34.5 billion mega IPO, days before it was scheduled to take place in November last year.

Shortly after, officials from China’s State Administration for Market Regulation announced a new set of rules targeting the use of monopolistic practices among big tech companies. Alibaba, Ant Group’s largest shareholder, was among the first few companies that came under investigation for its alleged use of monopolistic practices.

While Alibaba is the most high profile target at the moment, nearly a dozen other firms, such as Tencent and Didi Chuxing, have had fines handed out to them for violating anti-monopoly rules. The increased scrutiny on tech companies has set the tone for 2021, with many expecting the country’s market watchdog to further tighten rules on the tech sector.

To make matters worse, the US continues to exert pressure on Chinese tech companies, especially those operating in the semiconductor industry. SMIC (HKEX:981) has become the latest victim after US regulators added the chipmaker to an export blacklist, cutting it off from US suppliers and technology.

In addition, the US Securities and Exchange Commission (SEC) recently adopted a law called the Holding Foreign Companies Accountable Act, which would allow it to delist Chinese tech companies listed on US exchanges in the event that they do not comply with their auditing standards.

The flurry of negative news have without a doubt shaken investors’ confidence in the sector and raised questions about whether the valuations of Chinese tech giants are sustainable. As a result, the share prices of Chinese tech companies fell, dragging the Hang Seng Tech Index down by more than -25% since its peak in February (Figure 1).

Figure 1: The Hang Seng Tech Index has corrected by more -25% since February

Fears of increased regulation largely overblown

Despite the barrage of bad news, we continue to hold a positive view on China’s tech sector and we view the recent sell-off as an opportunity for investors to accumulate more shares.

Firstly, we think that investors should not be overly worried about the increased regulation on China’s tech sector.

The government has made it clear that the main purpose of the increased regulation is to safeguard consumers, and to promote healthy competition and the sustainable growth of China’s technology sector in the long run. They are not meant to stifle the growth of tech companies, like what the US is trying to achieve.

It has also acknowledged that tech companies have played a crucial role in stabilising the economy during the pandemic, as their digital services have allowed businesses and individuals to carry out their daily activities with as little disruption as possible. Through this, it is evident that the government recognises the value these tech companies have as the country undergoes a massive digital transformation.

Related Article: Quick Take: What impact will the recent antitrust regulations have on Chinese tech companies?

Most importantly, investors should know that the majority of the successful Chinese tech companies are where they are today mainly because of network effects (e.g. WeChat’s ecosystem) and superior product offerings, rather than significant anti-competitive behaviour, which is what the government is trying to deter.

Secondly, the loose regulatory environment in the past has allowed these companies to grow into the behemoths that they are today. However, as many of them are now systemically important to China’s economy due to their involvement in financial services (e.g. Alipay, WeChat Pay), some form of regulation is necessary to ensure that they do not take on excessive risk.

As a matter of fact, China is not the only country that is trying to regulate big tech companies. Over the past few years, there has been increasing calls for greater regulation over big tech companies from policymakers in the US and Europe given the significant role these companies play in the economy and in our lives. From this perspective, we think that China has perfectly legitimate reasons to do so as well.

Lastly, we think that the anti-monopoly laws could be a way for China’s government to preserve the country’s innovative spirit by protecting young companies, giving them a chance to develop. This is very similar to what the government did in the past for today’s big tech companies, during which it shielded them from the threat of foreign competition, contributing to their rapid expansion.

As China seeks to achieve technology self-sufficiency – an urgent agenda in light of rising tensions with the US – cultivating the element of innovation in China’s economy has become ever more critical.

Chinese companies have the ability to overcome pressure from the US

Despite the mounting pressure from the US, China will not fold. We believe that the recent actions taken against Chinese tech companies, especially those that operate in the semiconductor industry, will have the opposite effect of compelling China to double down its efforts in building up its chip making capabilities, instead of slowing its growth.

With the motivation and the resources to become technologically self-sufficient, we think that China’s semiconductor industry is about to enter a phase of supercharged growth, one that will bring about many investment opportunities in time to come.

Furthermore, investors should note that SMIC (HKEX:981) is currently the only company within the iShares Hang Seng Tech ETF (HKEX:3067) that is on the entity list. The remaining 29 companies are not affected at the moment. However, there is a possibility that these companies may be sanctioned in the future in the event that the Biden administration decides to tighten rules even further.

Related Article: China’s semiconductor industry: A sleeping giant that has been awakened

Contrary to what most people think with regards to the new law that the SEC recently adopted, Chinese companies will not be delisted immediately in the event that they are deemed to be non-compliant with US auditing standards.

Instead, delistings will only occur if a company fails to comply with the standards for three consecutive years. Moreover, the three year clock will not begin until the SEC drafts rules on how the law will be implemented, which may take a while.

Nevertheless, delistings should not be a major concern for investors because Chinese companies can always choose to relist elsewhere like in Hong Kong for instance, where several firms such as JD.com (HKEX:9618) and Baidu (HKEX:9888) have completed their secondary listings in the recent years.

As Asia’s financial hub, Hong Kong is becoming an increasingly attractive location for Chinese companies to list their shares given its unique position as a gateway to both China and the rest of the world. Furthermore, the HKEX recently announced that it is planning to ease listing requirements even further in a bid to attract more firms to sell their shares there.

Long-term growth story remains intact, supported by rapidly unfolding megatrends

Looking forward, the outlook for China’s tech sector remains robust as companies benefit from rapidly unfolding megatrends, such as rising Internet penetration rates and the digitalisation of consumption, both of which have been boosted by the pandemic.

With most of the country placed under strict lockdown measures during the first half of 2020, most physical/in-person activities have started to shift online. This has driven the Internet penetration rate in China up from 61.2% in 2019 to a record high of 70.4% in 2020. The 9.2 percentage point jump in penetration rate between 2019 and 2020 is the largest ever in China’s Internet history (Figure 2).

Figure 2: Internet penetration rates in China jumped by nearly 10% between 2019 and 2020

The rising Internet penetration rate seems to have produced a cascading effect on other segments of China’s tech sector, such as cloud computing and live commerce, as businesses accelerate the adoption of digital solutions to keep up with the increasingly digitalised consumption habits of consumers.

Cloud computing, in particular, played a pivotal role during the COVID-19 pandemic, supporting the digital transformation process and allowing businesses to operate with as little disruption as possible. Growth in China’s cloud infrastructure services spend continues to be among the fastest in the world, rising by 66% year-over-year in 2020 (Figure 3).

Figure 3: Cloud spending in China continues to outpace the rest of the world

This should not come as a surprise as the government declared cloud computing as one of the key technologies that China will focus on in its 14th Five Year Plan, alongside 5G, semiconductors and more.

Related Article: Alibaba Cloud: The next profit engine of China’s largest tech company

Recent sell-off is an opportunity to accumulate more shares

Based on a fair PE multiple of 35X, our target price for the iShares Hang Seng Tech ETF (HKEX:3067) is HKD 25, which translates to an upside potential of close to 50%.

We are confident that the recent sell off is largely sentiment driven, and factors, such as the increased regulation and mounting pressure from the US, pose limited risk to the long-term growth story of China’s technology sector. As we have mentioned earlier, Chinese tech companies may even benefit as China works towards becoming technologically self-sufficient.

Market volatility is inevitable, but what we should do as investors is to ignore the short-term fluctuations and focus on the long-term growth story instead. Sell-offs are typically the best time to accumulate good stocks. Investors who have faith in China’s tech sector should make use of this opportunity to add to their positions.

Table 1: Earnings table for China’s tech sector

|

2021 |

2022 |

2023 |

|

|

EPS |

199.57 |

279.40 |

363.22 |

|

Earnings Growth |

- |

40% |

30% |

|

PE Ratio |

42.38 |

30.27 |

23.29 |

|

Upside Potential* |

- |

15.6% |

50.3% |

|

Source: Bloomberg Finance L.P., iFAST Estimates *Based on our fair PE multiple of 35X |

|||

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.