Image Credits: BusinessKorea

• China has long struggled to produce its own chips as it lacks the technology. For decades, the country has relied heavily on imports to fulfil its semiconductor demand.

• We believe that the recent bans will push China to double down its efforts in building up its semiconductor industry, bringing about many investment opportunities in time to come.

• To support the growth of its semiconductor industry, China established a national fund to invest in semiconductor companies and has also made significant adjustments to its tax policy.

• Investors seeking exposure to this fast-growing industry can consider the Global X China Semiconductor ETF (HKEX:3191). Our target price for this ETF is HKD 77.

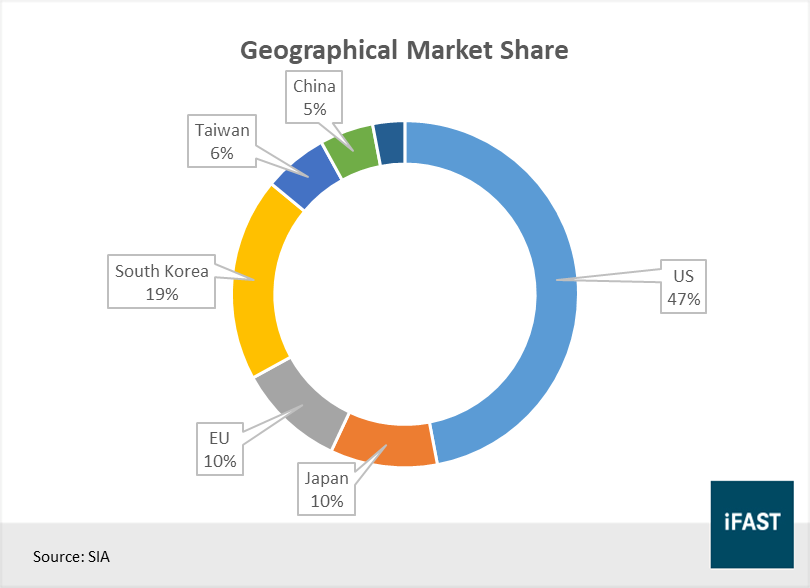

Since the very beginning, China has not had a significant presence in the global semiconductor industry. In 2019, the country as a whole accounted for only 5% of the global industry market share, far behind the US and South Korea, which controlled 47% and 19% of the market respectively (Figure 1).

Figure 1: China accounts for only 5% of the global semiconductor market

China’s semiconductor foundry technology is years behind its peers

The main reason why China has such a small market share in the global semiconductor industry is because of technology. In terms of chip design, China has made significant progress over the years, with leading fabless companies like HiSillicon able to design advanced chips used in applications such as 5G and artificial intelligence. For instance, HiSilicon’s newest smartphone processor, the Kirin 9000, is considered to be on par with those designed by Apple.

Where China is lacking the most is foundry technology. For decades, China has long struggled to produce its own chips, especially those that require a cutting-edge manufacturing process. Its most advanced foundry, SMIC (HKEX:981), only began producing chips using a 14nm process in 4Q19, a feat that TSMC managed to achieve five years ago. Within a short span of less than a year, this gap has widened, with TSMC introducing its 5nm process in the first half of 2020.

Besides TSMC, SMIC’s technology is also several generations behind other foundries, such as GlobalFoundries and Samsung Foundry (Table 1).

Table 1: SMIC’s 14nm process node is several generations behind its peers

|

Foundry |

Most Advanced Process Node |

|

SMIC |

14nm |

|

TSMC |

5nm |

|

GlobalFoundries |

12nm |

|

Samsung Foundry |

5nm |

|

Source: Company Data |

|

Despite being the largest electronics manufacturing hub in the world, domestic production only accounts for roughly 20-30% of China’s total semiconductor demand. Its limited technological capabilities mean that it has no choice but to fulfil the remaining demand by importing from other countries, mainly the US.

In 2020, China’s chip imports totalled approximately USD 380 billion, a number that has been increasing every year as global demand for electronics continues to rise (Figure 2). But with the US clamping down on China’s access to these critical components, it will most likely have to look inwards to fulfil its demand for semiconductors.

Figure 2: China relies heavily on imports to feed its semiconductor needs

China to focus on developing its domestic semiconductor industry

Since the US-China trade war began in 2018, the relationship between both countries has deteriorated substantially. Over the past two years, the conflict has extended to a number of issues beyond trade, such as intellectual property theft and national security.

Right now, national security issues seem to be the number one priority of the US government, as it has implemented a string of measures over the past two years in an attempt to hamstring the growth of China’s leading technology companies, starting with Huawei.

In May 2019, the US Commerce Department announced that it has placed Huawei and 68 of its affiliates on its Entity List, claiming that the telecoms equipment manufactured by the company can be used for spying, and therefore, posing a national security threat to the US.

This effectively restricts Huawei’s ability to purchase vital components like semiconductors from US firms to manufacture its products. From then till now, many other Chinese tech companies (e.g. Xiaomi) have fallen into the crosshairs of US regulators. If these companies are unable to find an alternative supply for chips, their business may be severely affected.

In response, Chinese officials began accelerating plans to strengthen the country’s semiconductor industry. As part of its “Made in China 2025” plan, China aims to produce 70% of all the semiconductors it requires by 2025, with a longer term goal of becoming completely self-sufficient. These efforts will no doubt be led by the nation’s top chipmakers, such as SMIC.

However, the US threw a wrench into China’s chip making ambitions by announcing that it will tighten export controls on the company, making it difficult for SMIC to acquire the latest equipment used to fabricate semiconductors.

Given how crucial semiconductors are to a nation’s development, we think that the bans will have the opposite effect of compelling China to double down its efforts in building up its semiconductor industry, instead of slowing the rise of China’s tech sector. The recent events have revealed China’s vulnerability in this key sector, and we think China will be very keen to fix these issues.

The road to self-sufficiency will definitely be paved with difficulties, but we believe that China will persevere through as the future of the nation depends on the success of this endeavour.

Supportive government policies to supercharge growth

To achieve its goal of becoming self-sufficient in chip production, the government has laid out several policies to support the industry. One of its greatest efforts was to establish a national fund, known as the China Integrated Circuit Industry Investment Fund (CICIIF), to help promote the growth of the local semiconductor industry.

The fund, which was first set up in 2014, has invested close to CNY 350 billion in various projects and companies within China’s semiconductor industry to-date. It is estimated that roughly 67% of the monies went to manufacturing firms, both integrated device manufacturers and foundries (Figure 3).

Figure 3: China’s national fund made huge investments in chip manufacturing

Secondly, the government also made significant adjustments to its tax policies last year, a decision that should greatly benefit local semiconductor companies.

Under the new policy, chipmakers that have been in operation for more than 15 years and produce chips using a 28nm and below process will be exempted from corporate income taxes for up to 10 years, while those producing 65nm to 28nm chips will get five years of tax exemption and a 50% discount on the corporate tax rate for the next five years beginning in 2020.

In addition, companies that are involved in chip design, packaging, testing, and equipment manufacturing will also be exempted from corporate income taxes for the first two years, and enjoy a 50% discount on the corporate tax rate for the next three years.

Table 2: Summary of the major tax policy changes for semiconductor companies

|

Company Type |

Tax Rate |

|

Standard Tax Rate |

25% |

|

28nm and below |

Tax exempt for up to 10 years |

|

28nm to 65nm |

Tax exempt for the first 5 years, 50% discount on corporate tax rate for the next 5 years |

|

66nm to 130nm |

Tax exempt for the first 2 years, 50% discount on corporate tax rate for the next 3 years |

|

Chip design, packaging, testing, materials and equipment |

|

|

Source: State Taxation Administration of the PRC, iFAST Compilations Data as of Dec 2020 |

|

The idea is that, by reducing the tax burden, Chinese semiconductor firms will have more resources to allocate to capital expenditure as well as research and development (R&D), which will hopefully improve their technological capabilities, allowing them to compete with their global peers.

Through the way these policies are structured, we can tell that the government’s focus is clearly on strengthening the country’s chip making capabilities, an area where it is currently lacking the most.

With the motivation and the resources to narrow the gap between themselves and the US, we believe that China’s semiconductor industry is about to enter a phase of supercharged growth, one that will bring about many investment opportunities in time to come.

Potential headwinds faced by China

It is worth noting that semiconductors are some of the most complex products to design and fabricate in the world, and the success of US-based firms in this field is not something that can be replicated overnight. It is the fruit of thousands of hours and billions of dollars spent on R&D over many decades.

To be on par with the US, China will most likely need to do the exact same thing while navigating through a maze of sanctions. Since our valuations are calculated with the assumption that China will be able to meet its ambition of producing 70% of all the semiconductors it requires by 2025, the key risk here is that share prices could see a severe correction if China falls short of meeting this target.

Significant upside potential as the industry expands

Investors who are seeking exposure to China’s fast-growing semiconductor industry may consider the Global X China Semiconductor ETF (HKEX:3191). This ETF seeks to replicate the performance of the FactSet China Semiconductor Index, which consists of a basket of 24 Chinese semiconductor companies. The top 10 holdings of this ETF include SMIC and Will Semiconductor.

Besides having a low expense ratio of just 0.68%, another advantage of this ETF is that it provides investors with exposure to semiconductor firms listed in Mainland China, which may not be easily accessible to certain investors.

Taking into account the country’s renewed focus on developing the industry and the string of supportive policies from the government, we believe that the industry will enter a high growth phase in the near to mid-term, which could send the shares of Chinese semiconductor companies upwards.

Based on a fair PE ratio of 35X, our target price for the Global X China Semiconductor ETF (HKEX:3191) is HKD 77. This translate to an upside potential of 53% for the industry as a whole.

Table 3: Earnings table for China’s semiconductor industry

|

2020 |

2021E |

2022E |

2023E |

|

|

PE Ratio |

71.94 |

48.06 |

34.33 |

22.88 |

|

Earnings Growth |

- |

35% |

40% |

50% |

|

EPS (CNY) |

2.79 |

3.77 |

5.27 |

7.91 |

|

Upside Potential |

- |

- |

2.0% |

52.9% |

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 24 March 2021 |

||||

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in the abovementioned securities.

The Research Team is part of iFAST Financial Pte Ltd.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.