- While Singapore’s market has been underperforming over the past few years, it has been playing catch-up over the past month, driven by positive vaccine news and Phase 3 reopening.

- The COVID-19 situation in Singapore has stabilised, with social distancing measures driving down infections rates, paving the way for the economy to recover in 2021.

- We expect the manufacturing sector to remain the key growth driver in 2021, driven by a still-robust external demand and a continued upswing in the global electronics cycle.

- Looking ahead to 2021, we expect the banks’ earnings to improve by approximately 30% in 2021, largely driven by lower loan loss provisions. S-REITs are headed for a better year in 2021, but the recovery is likely to be uneven, with some segments recovering faster than the others.

- At its current level, Singapore equities offer investors an upside potential of 13.7% by end-2022, with an attractive dividend yield of about 4.0-4.5% over the next two years. We maintain our star rating of 3.5 Stars “Attractive” rating for the Singapore equity market.

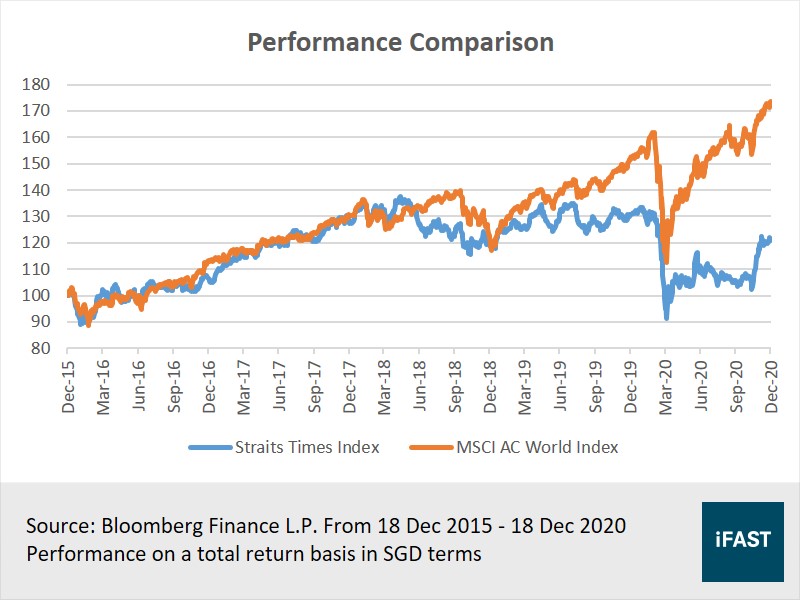

Singapore’s equity market has been lagging behind its global peers for the most part of this year.

While global equities have been on an unprecedented winning streak since end-March, delivering an impressive 37.0% return (in SGD terms as of 18 December 2020), the Straits Times Index could only serve up a 19.0% return over the same period.

What is more jarring is the fact that Singapore’s relative underperformance is not isolated to this year. The performance comparison between the MSCI AC World Index and the Straits Times Index says it all (Chart 1). Over the past five years, the MSCI AC World Index delivered a strong annualised return of 11.6%, while the Straits Times Index only delivered a lukewarm annualised return of 3.9% – that’s a huge gap of almost eight percentage points!

Chart 1: Singapore has underperformed global equities in recent years

However, with positive vaccine news and the Singapore economy entering its third phase of reopening, the Straits Times Index has been playing catch-up over the past month, racking up strong gains of 18.0% since end-October. If this recent rally is anything to go by, the winds of change may have finally descended upon Singapore’s equity market.

The question then beckons, is 2021 the year for Singapore equities to finally shine? We think it could.

COVID-19 stabilisation sets stage for economic recovery

Singapore has come a long way since it recorded its first COVID-19 case in January.

What started off as a viral infection that was largely confined to China became a public health emergency of international concern. Singapore was not spared either, with the city-state seeing four-digit new cases each day at the peak of the pandemic. The situation even sparked a frenzied rush for household items, with such items as toilet paper, face masks, rice, and pasta stripped from supermarket shelves.

The COVID-19 situation in Singapore has since stabilised, with the social distancing measures implemented by the government achieving a great degree of success in driving down infection rates. At this juncture, most of the new cases are imported, and there are very few local transmissions. With the pandemic largely brought under control, the Singapore economy is entering its third phase of reopening, paving the way for an eventual recovery in 2021.

Chart 2: Social distancing measures have driven down infection rates

In fact, the recovery is already underway, with the second quarter marking the bottom of this current cycle. Following a deep contraction of -13.3% year-on-year in 2Q 2020, Singapore’s economy rebounded in the third quarter, with the contraction narrowing to -5.8% year-on-year on the back of a resumption in economic activities since the “circuit-breaker” period. While growth remained in negative territory, the headline GDP growth rate of -5.8% year-on-year was much better than initially expected, with the improvement driven by the manufacturing sector.

Manufacturing to power Singapore back to growth in 2021

Singapore’s coronavirus-hit economy has so far been given a shot in the arm by its manufacturing sector, which has been leading the recovery, with the manufacturing purchasing managers' index (PMI) in expansionary territory for the fifth straight month in November. The strength in Singapore’s manufacturing sector has been underpinned by strong demand for its biomedical and electronic products.

Moving forward, we expect the manufacturing sector to remain the key driver of Singapore's rebound from its coronavirus-induced recession. The PMIs of key markets, such as US, China, and the Eurozone, have all rebounded strongly from their sharp declines, and remain firmly in expansionary territory, indicating a still-robust external demand (Chart 3).

Chart 3: PMIs of key markets have rebounded strongly

The electronics sector, which forms the bulk of manufacturing, is likely to benefit from the continued upswing in the global electronics cycle (Chart 4), especially with companies embracing work-from-home (WFH) arrangements as the new norm. The speed and scale of the COVID-19 pandemic has also led companies to step up their investments in digital solutions as part of their business continuity plans to not only cope with the here and now, but also to mitigate any future crisis.

Chart 4: Manufacturing sector to benefit from upswing in global electronics cycle

These bode well for Singapore’s manufacturing sector heading into 2021. With Phase 3 of Singapore’s re-opening also likely to bring the much-needed respite to the embattled construction and services sectors, Singapore’s economy is expected to return to positive growth in 2021 (Chart 5), with a GDP growth of 5.5% in 2021, and 3.4% in 2022.

Chart 5: Singapore’s economy to return to growth in 2021

Time to bank on Singapore banks in 2021

With the three Singapore banks constituting almost 40% of the Straits Times Index, no analysis on Singapore’s equity market will ever be complete without a discussion on the earnings prospects of DBS (SGX:D05), OCBC (SGX:O39), and UOB (SGX:U11).

The three banks charted a sharp dive in earnings in the first half of 2020, with an average net profit of SGD 1.8 billion that represented a decline of about -32.5% year-on-year, as net interest margins (NIM) – a measure of lending profitability – dipped amidst a collapse in benchmark rates. The trio also had to set aside significantly more provisions for loan losses due to the economic fallout from the COVID-19 pandemic.

Looking ahead to 2021, we expect the banks’ earnings to improve by approximately 30% in 2021, largely driven by lower loan loss provisions, which are likely to peak in 2020 as the banks had front-loaded allowances in 1H 2020 (Chart 6). We expect loan loss provisions to slow down in 2021 before returning to their normal levels in 2022, signalling a turning point for the banks’ earnings.

Chart 6: Loan loss provisions of the three banks to peak in 2020

Given that the Fed has plans to keep the target range for the federal funds rate at near zero until at least 2023, or until the economy shows a sustained recovery, we expect interest rates to remain at its current low levels, and do not expect a significant recovery in NIMs. That said, we believe NIMs have bottomed, and a substantial compression in margins in 2021 seems unlikely, especially since the global economy and credit environment has improved since the COVID-19 shock.

Moreover, DBS, OCBC and UOB continued to report healthy capital ratios in 1H20 despite making hefty provisions. While credit migration may result in an increase in risk-weighted assets in the subsequent quarters, the improvement in earnings – thanks to the slowdown in provisions – should help support their overall capital positions. As Singapore recovers from the pandemic, we believe MAS will revisit its previous decision to cap dividends.

Based on their current capital positions, we believe the banks have adequate capital to resume their pre-COVID dividends. On average, they are offering investors an attractive dividend yield of 5.6%.

(Related article: Why it is time to bank on Singapore banks in 2021)

S-REITs headed for uneven recovery next year

As for the S-REITs, there has been a performance divergence within this sector year-to-date. The performance of hospitality and retail REITs have been hit the hardest, thanks to COVID-19, while the resilient industrial and data centre REITs have outperformed the broader sector (Chart 7).

Chart 7: Total return of S-REIT sub-segments

With the potential roll-out of the COVID-19 vaccine and Singapore entering into its third phase of reopening, we reckoned that industrial and data centre REITs will continue to deliver resilient growth while expecting hospitality and retail REITs to recover gradually. On the other end of the spectrum, we believe office REITs’ long-term outlook will remain uncertain despite the recovery in Singapore’s economy.

Hospitality REITs: From an empty Changi airport to deserted hotels, Singapore’s domestic hospitality industry has been dealt an unprecedented blow by the COVID-19 pandemic. As such, the roll-out of vaccines around the world and an eventual resumption of international travel is expected to jumpstart the recovery of hospitality REITs in 2021. While a full recovery may extend beyond 2021, most hospitality REITs will be supported by the fixed rent from their master leases, providing downside protection while international air travel resumes gradually.

Retail REITs: Retail REITs could also see a recovery as Singapore enters into its Phase 3 re-opening. Suburban malls, in particular, are likely to continue their recovery to pre-COVID levels, as they tend to focus on essential goods and services, and have a close proximity to densely-populated residential areas. Hence, they are more resilient to the increasing adoption of e-commerce, which has been posing structural challenges to brick-and-mortar stores.

Office REITs: Meanwhile, the long-term outlook for office REITs remains uncertain, especially with companies embracing WFH arrangements as the new norm. This will reduce the need for companies to expand their office spaces. Some may even consider downsizing. With the reduced demand for offices, occupancy rates and rental rates are likely to remain under pressure. We also expect more tenants asking for shorter and more flexible lease terms as they figure out their future office needs.

Industrial and data centre REITs: Industrial and data centre REITs are well-positioned to deliver resilient growth going forward. The acceleration of e-commerce will continue to drive the demand for warehouse spaces, while the prevalence of WFH arrangements and future 5G adoption, will lead to an increase in spending on data centres.

(Related article: Not all S-REITs are made the same, here's what you should look out for in 2021)

Earnings recovery and dividend yield to lend support to Singapore equities

In view of the improved macroeconomic backdrop and fundamentals, we expect to see strong earnings recovery for Singapore equities in 2021, driven mainly by the three local banks. While earnings are likely to contract -43.7% for the full-year in 2020, we estimate earnings to rebound by 38.8% in 2021, and 14.6% in 2022 (Table 1).

Table 1: Earnings of Singapore equities to recover in 2021

|

Singapore Equities (Straits Times Index) |

FY2020 |

FY2021 |

FY2022 |

|

PE Ratio |

19.6 |

14.1 |

12.3 |

|

Earnings Growth (%) |

-43.7% |

38.8% |

14.6% |

|

Earnings Per Share |

145.4 |

201.8 |

231.4 |

|

Projected Fair Price (Based on 14.0X Fair PE Ratio) |

2,036 |

2,825 |

3,239 |

|

Potential Upside (%) |

- |

- |

+13.7% |

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 18 December 2020 |

|||

At its current level, the Straits Times Index is trading at a PE ratio of 12.3 based on our 2022 estimated earnings, offering investors an upside potential of 13.7%. We maintain our star rating of 3.5 Stars “Attractive” rating for the Singapore equity market.

The good news? The market is currently offering investors an attractive dividend yield of about 4.0-4.5% over the next two years. Its current dividend yield also represents a spread of about 250 basis points over the 10-year Singapore government bond yield, much higher than the long-term average spread (Chart 8). As such, investing in the Singapore equity market right now will put time on your side as you are being paid dividends while waiting for the market to return to its fair value.

Chart 8: Dividend yield spread remains above long-term average

Investors who can afford room in their portfolios for a Singapore equity fund may be interested in the Nikko AM Singapore Dividend Equity, our recommended fund that invests primarily in Singapore equities that offer attractive and sustainable dividend payments.

While the SPDR Straits Times Index ETF (SGX:ES3) is also a viable option for passive investors, it is worth noting that the Nikko AM Singapore Dividend Equity fund has a strong track record of outperforming the market. As such, navigating the Singapore equity market with an active strategy might be the way to go.

Table 2: Recommended products for exposure to Singapore equities

|

Equity Market |

Actively Managed Fund |

Passive Tracking ETF |

|

Singapore |

Nikko AM Singapore Dividend Equity SGD |

SPDR Straits Times Index ETF |

Chart 9: Earnings recovery to drive Singapore equities in 2021

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.